Asset-Liability Mismatch

Research Edition

Part of any domain is doing extensive research in order to increase your ability to operate effectively. Today I want to go over asset-liability mismatch since it is clearly an important thing for people to understand.

There have been a lot of discussions and headlines surrounding the current banking issues. Let’s dig into a couple of definitions and ideas:

Every financial crisis occurs due to an asset-liability mismatch.

Asset-liability mismatch refers to a situation in which the financial obligations (liabilities) of an entity, such as a bank, corporation, or individual, are not well-aligned with their assets in terms of their maturity, currency, or cash flow. This mismatch can create liquidity or solvency problems for the entity and may lead to financial instability or even bankruptcy in extreme cases.

There are several dimensions to asset-liability mismatch:

Maturity mismatch: This occurs when the maturities of assets and liabilities are not well matched. For instance, a bank may have long-term loans (assets) and short-term deposits (liabilities). In such a case, if depositors demand their money back before the loans are repaid, the bank may face a liquidity crisis.

Currency mismatch: This happens when assets and liabilities are denominated in different currencies. For example, a company may have assets in one currency and liabilities in another. Fluctuations in exchange rates can lead to significant changes in the value of the assets or liabilities, causing financial strain.

Interest rate mismatch: This type of mismatch arises when the interest rates on assets and liabilities are not in sync. For example, if a bank has issued variable-rate loans (assets) and fixed-rate deposits (liabilities), an increase in interest rates could lead to higher interest income from loans but no change in interest expense, leading to improved profitability. However, if interest rates decrease, the bank's interest income will decrease while the interest expense remains the same, which can lead to financial distress.

Cash flow mismatch: This occurs when the timing or amount of cash inflows from assets and cash outflows for liabilities are not aligned. For example, a company may have uneven cash flows from its operations, causing difficulties in meeting its periodic debt obligations.

Asset-liability management (ALM) is the process of managing the risks arising from these mismatches. ALM involves developing strategies to monitor, measure, and control risks associated with mismatches between assets and liabilities, ensuring that the entity remains financially stable and solvent.

This is a very simplified summary of asset-liability mismatch. In reality, there are books with thousands of pages breaking down these dynamics. However, once you begin to understand it, you can begin to understand HOW to think about the assets and liabilities of a person, company, state, or even country.

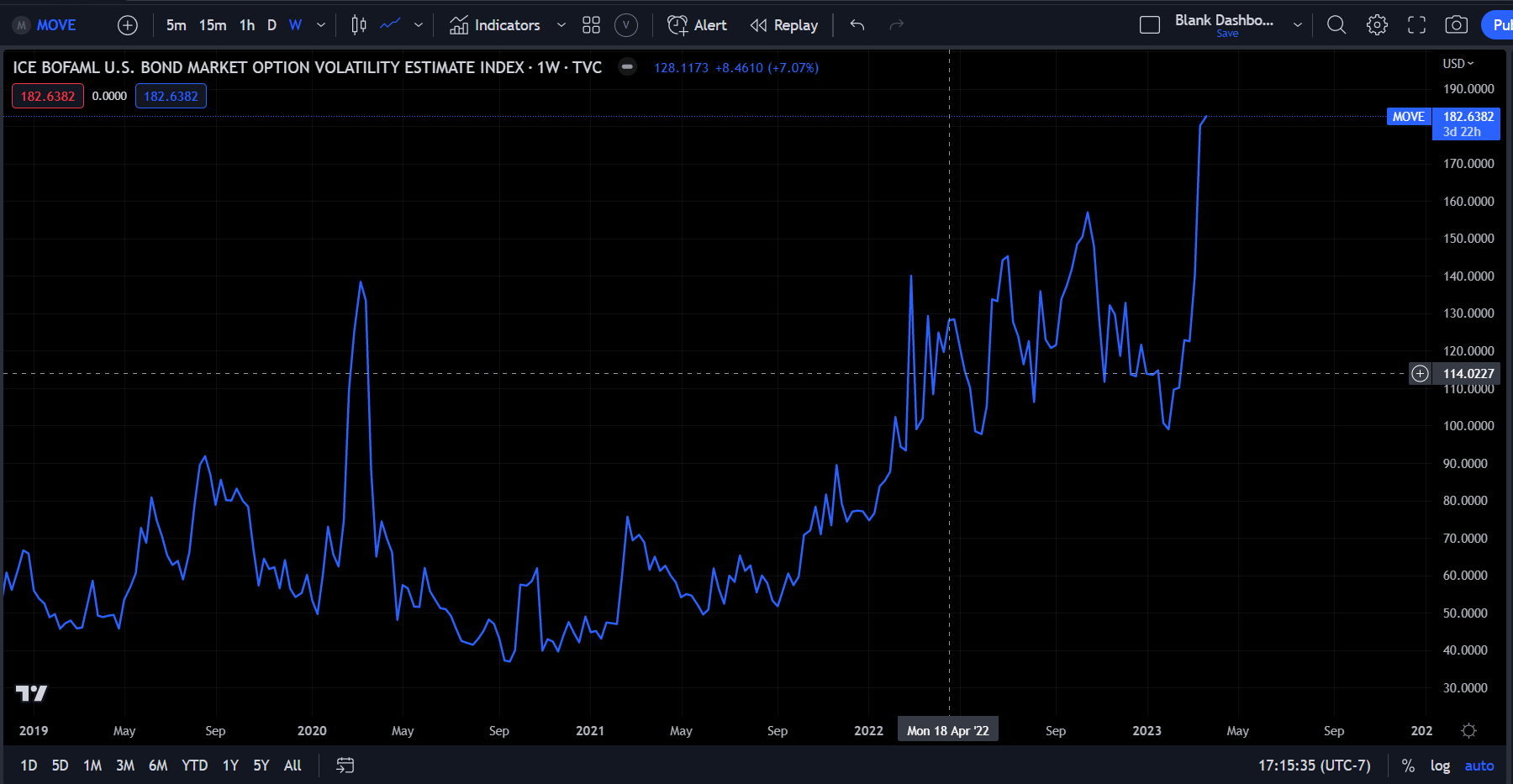

The way a company or bank manages risk is by ensuring that they are not overexposed to an asset-liability mismatch. In the SVB situation, we had a bank that didn’t hedge their duration risk which is banking 101. All the other major banks were hedging their duration risk which is one of the reasons we saw implied vol go up so much.

This is the MOVE Index which is like the VIX for bonds:

Anytime I think about taking a view on a specific asset for trades, I look at how a specific change will be transmitted through the assets and liabilities of a balance sheet. There are so many different shocks that can happen and so many different ways those shocks can be transmitted.

For example, if a company or country has a large portion of its debt or operations denominated in a specific currency, it can easily go bankrupt when an outsized FX move occurs if it doesn’t hedge its risk. Many times, you simply need to identify situations where there is a liability mismatch and wait for a shock to occur because you know it will have an outsized impact.

This is the process you need to work through over and over when identifying opportunities or running any company/portfolio. The key is having quality information flow and a proper interpretation of that information.

In the next article, I will use these principles to explain how I am thinking about scenario analysis for 2023 and the different opportunities that could occur.

Thanks for reading!