Banking "Crisis"

These things take time

It has been a very interesting week tracking financial markets and all the developments. Preparation and quality information flow is the name of the game during periods like this.

This piece might be a little technical but it should be informative.

First, I noted that the short equities trade was positive and working. Go see the previous two articles where I provided the signal in real-time and its updates. I am now covering the short equity position and looking to benefit on the long side from a short squeeze.

Even though there is a lot of news about “the world ending,” positioning has gotten way too bearish way too fast in my opinion. It truly is amazing how fast information spreads. Multiple people came up to me over the weekend asking me what I think will happen with SVB. When that happens, I know I don’t have an information advantage or any edge.

THE TENSION:

There is now an incredibly interesting tension in financial markets. The tension between credit risk and inflation risk. Credit risk is about companies not having the ability to meet obligations via their cash flows. Inflation risk or duration risk is how we discount those cash flows given the time value of money. Basically, overnight, the forward curve went from pricing rate hikes into the summer to pricing rate cuts. This was a very dramatic shift.

Basically, the market is saying that the credit risk will be greater than the inflation risk and that Powell will cut even though inflation is still incredibly high. Actually, this can potentially lead to a reflexive feedback loop where the looser conditions lead to a looser money supply and higher inflation. We will see though.

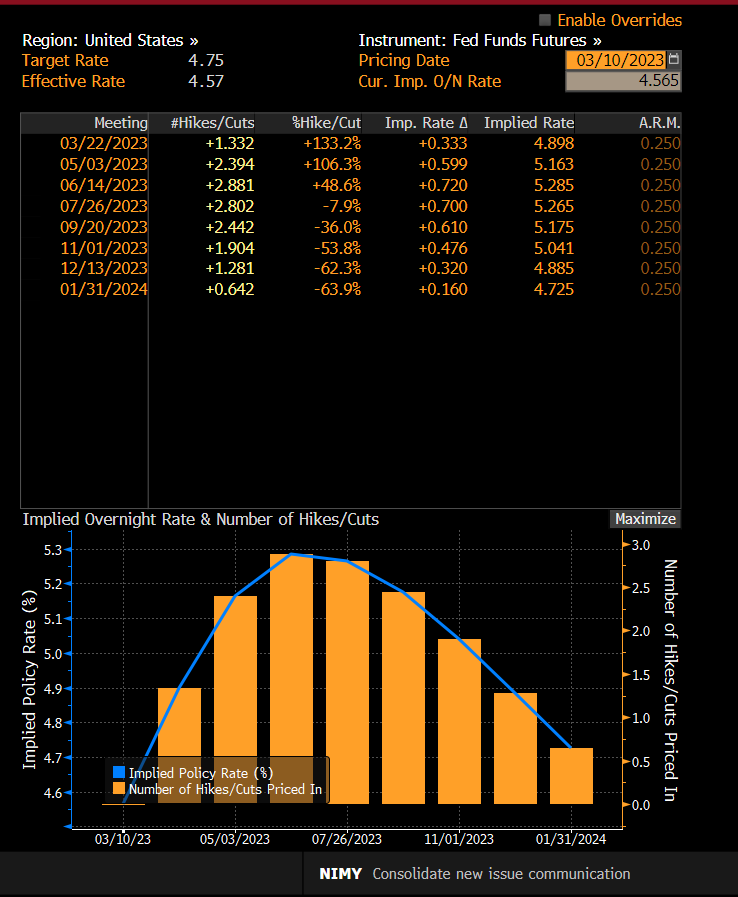

Here was the forward curve pricing rate hikes/cuts on Friday at market close:

Here it is now:

If you watch these instruments intraday, they are basically moving inversely to bank stocks which means there is a tension between credit risk and inflation risk. In simple terms, the market is saying, which one is going to screw me over more, inflation or a credit crunch? And then it’s bouncing back and forth between the two as new data and news come out.

Now as Americans, most of us are very US-centric and don’t think about the rest of the world. However, as a participant in financial markets, you need to think about global capital flows and information flows. What does this mean? It means that the SVB situation is connected to banks across the world. The tension I described above is taking place in Japan, Europe, the UK, and other major countries.

This is why ever since Sunday when Japanese markets opened, I have been watching bank stocks across every single country as they have their market open and close. Generally speaking, most people don’t think of doing this and it only gets talked about retrospectively after the fact.

The important thing to know is that it’s not just US investors who hold US assets. Investors from across the world buy and sell US assets every single day. This is why we see a correlation between currencies and assets. If you are a foreigner and want to buy US assets, you first need to exchange your local currency for US dollars and then you can buy the S&P500 (or whatever asset it is). When enough people do this, you actually begin to move exchange rates with the supply and demand of assets.

So when we have periods of time like this where every piece of information is important, I want to see what every market is doing. For example, if some piece of news comes out overnight during the Asia trading session, no one is up in New York to price the information. It is up to Japanese traders to make the move. But, then I know when New York traders wake up in the morning, they might be forced to buy or sell depending on what informational developments occurred overnight.

The information flows and capital flows are everything!

What is next?

Even if we don’t know what is going to take place, we can still benefit from the uncertainty because we are more prepared than other people in the market. This is why having a strategy and a plan is the best course of action. Most people don’t have a plan or in-depth knowledge of how their domain works. This is just setting up for a disaster to happen.

However, if we carefully plan, and have a proper interpretation of the signals that take place, then we are able to react faster than others. And this isn’t even about financial markets or high-frequency trading. This type of dynamic takes place across all timeframes whether it’s days, months, years or even decades. The bigger the player, the slower they move.

Think about it like this, an individual can easily move their money in and out of financial markets at the click of a button. Can they move houses that fast? Not really. So when more migration flows began in 2020, the “speed” of buying a house wasn’t about microseconds, it was about weeks and months.

What about an institution? Well, that might take a little longer. What about an entire country? That could take a really long time!

Knowing that it could take a country years or decades to be in a position of preparation for a crisis is important because you have an idea of the time horizon and constraints that a country is under.

All really helpful principles to think about when considering your own situation.

Charts: Let’s go through a couple more charts

We have not entered the period of time where earnings are getting revised down. We will see when this happens and how this additional credit risk either brings it closer or pushes it out farther in time.

Oil prices breaking to new lows today. This helps a little with the inflation picture but its only one piece.

Without getting too technical, this is the FRA-OIS spread which is a rough reflection of credit conditions. You can see 2020, the spikes during the 2022 hiking cycle and then the current spike.

A lot of people see charts like this and get super bearish. When I look at it, I think, yeah that just went up but what happens if it comes back down, where do you think the market will be? I am always thinking in scenarios that can occur as opposed to only extrapolating the current move.

Final chart! Here is an interesting backtest of SPX during past recessions. A lot of different things can happen. Not everything is a repeat of 2008 simply because most of America and the financial industry have a recency bias for it.

Thanks for taking the time and reading!