Direction of the Substack and Macro Outlook

A lot of new updates

Hello everyone,

I wanted to take a quick moment and thank everyone for reading. This Substack has been up and running since the beginning of the year with great success. I wanted to lay out a couple of things for where we are heading this year.

First, I have provided a lot of good introductory articles on trading, macro, and wealth management. These will function as a great foundation for the publications through the rest of this year. I would encourage you to go back and read them because they frame how to think about markets correctly.

Second, I will be adding a Twitter account for Capital Flows. It can be found @Globalflows. I will provide some tweets and more content on there as well.

What is the plan moving forward?

Big picture, when we approach markets, we need to account for every moving part and variable. After you account for every variable you need to build a system that generates signals so that we can act correctly during specific market regimes. I laid a lot of this out in the first article.

For the rest of this year, I have decided to spend time providing these mental frameworks and models on countries across the world. I will be providing it in an educational format, connecting it to real-time insights, and linking it with specific trades or actions that can be implemented.

This will include breakdowns of economic data, asset markets, positioning, geopolitics, and much more. The focus will be on providing these frameworks in an educational format while also connecting them to tangible real-time examples or trades. I will also be providing regular analysis on G7 asset markets and specifically US markets since those are the most relevant.

Why do this? I have always found this quote by legendary trader Paul Tudor Jones very helpful:

This is part of the reason for the name “Capital Flows.”

With all of that being said, let’s have a couple of thoughts on markets!

Macro and Markets:

In the last article, I said I would expand a little into this idea of asset-liability mismatch and how it connects to scenario analysis for 2023.

We saw a marginal increase in credit spreads due to the SVB banking crisis.

We are now watching for the persistence of the spread. If it continues trending up or remains at an elevated level then we need to be watching for additional deterioration and risk-off moves in equities. When credit risk drives the VIX, it’s not really bad.

Here is the FRA-OIS spread with the 6th Eurodollar contract. Think about it like this, when credit risk increases, the market prices more rate cuts. When more rate cuts get priced into the forward curve, government bonds begin to rally.

We will need to be watching the inflation data closely for the next month or so because any surprise to the upside could constrain the FED to do additional rate hikes while credit risk is elevated.

All of this can easily be monitored on the free CME tool here: https://www.cmegroup.com/tools-information/quikstrike/treasury-watch.html

FOMC Today:

Today Powell raised the FED funds rate by 25bps. The key was his speech though. He didn’t specifically correct how the forward curve was pricing rate cuts. Powell had the opportunity to “correct” the forward curve ever since it did a massive flip on the SVB news.

If Powell holds rates at an elevated level, the oscillations in bonds will likely occur as we approach where these rate cuts are getting priced and they get squeezed out.

The final thing I am watching is inflation swaps. If these begin to rally on higher-than-expected inflation prints, it is likely that the forward curve will begin repricing the rate cuts.

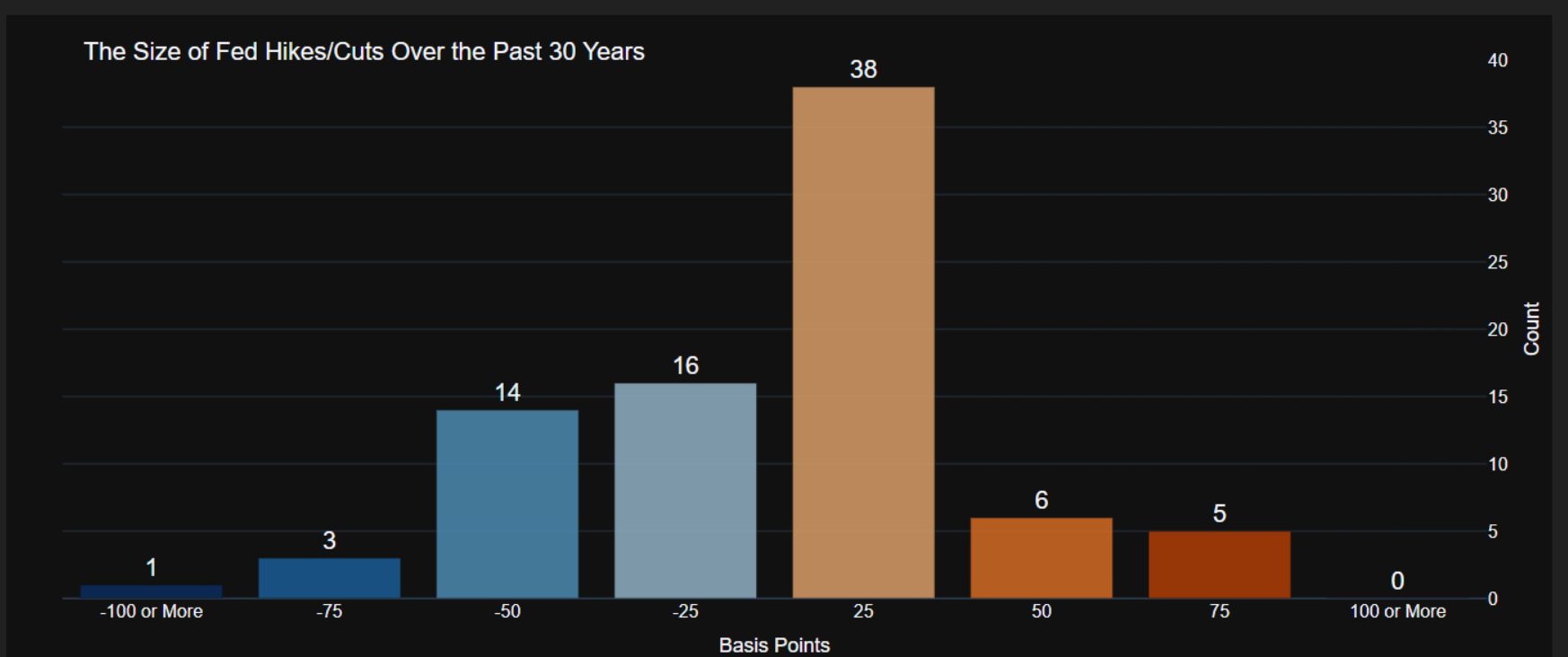

Powell began doing the aggressive 75bps hikes in 2022 when inflation swaps were really rallying. And just to give some perspective, 75bps hikes are NOT normal.

Conclusion:

Watch for additional issues such as SVB that could cause credit spreads to widen.

Watch forward expectations in connection with credit risk.

Watch inflation prints and inflation swaps (or breakevens) to see if a scenario is being set up for the forward curve to get repriced.

Thanks for reading!

Hello- could you please explain this statement. "If these (inflation swaps)begin to rally on higher-than-expected inflation prints, it is likely that the forward curve will begin repricing the rate cuts." Why will the rally in inflation swaps reflect in rate cuts in the forward curve?