Liquidity Is Expanding and Panic Buying Has Begun

Why credit issuance is at 3x last year's pace, how the IGV positioning unwind sets up the next leg, and why real rates 28bps from negative is the chart everyone should be watching into FOMC

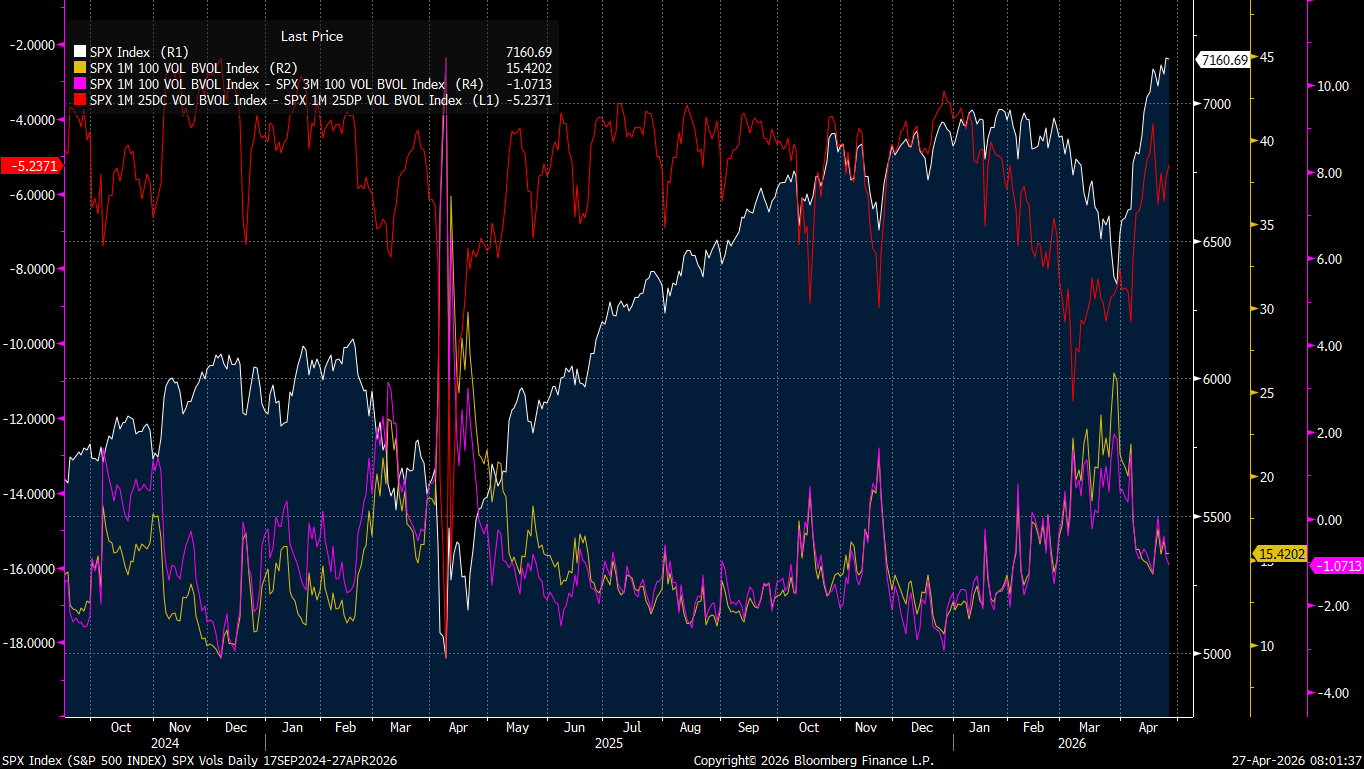

Today I had PharmD_KS on the stream to walk through the macro setup heading into FOMC week and how it lines up with the execution levels in ES, NQ, SMH, and the Russell. The panic buying has officially started. April US junk bond issuance is nearly thirty billion dollars, more than triple last year’s total. Intel just kicked off a fourteen billion dollar bond sale. Oracle wrapped sixteen billion in financing for the Michigan data center. Real rates are 28bps from turning negative. The Russell is outperforming, IGV vol is at the same level it was at the prior lows without making a new low, and the entire sector rotation setup is primed for another aggressive leg higher.

LIVESTREAM RECORDING FROM TODAY:

Today’s Livestream: Main Talking Points

1. Credit issuance is at 3x last year’s pace and that single fact refutes every “liquidity is contracting” thesis in the market. April US junk bond issuance is nearly thirty billion dollars, more than triple last year’s total. Eleven billion in high yield notes sold in the past week alone. Intel kicked off a fourteen billion dollar bond sale to fund its Aryan Lead acquisition. Oracle wrapped sixteen billion in financing for its Michigan data center. This is not investment grade. This is high yield. When credit markets are absorbing this much issuance at this kind of pace, it is mechanically impossible for liquidity to be contracting. The bears are getting falsified by the credit markets in real time.

2. Real rates are 28 basis points from turning negative. That is the same setup that fueled the 2020-2021 melt-up. One-year real rates are at new lows. Two-year real rates are 1bp from negative. If we cross into negative territory, you get the same dynamic that produced one of the largest melt-ups in human history four years ago. The setup does not require Fed cuts to get there. It requires the Fed to keep doing what it is doing now: nothing. The Fed’s inaction is the liquidity impulse, and it is mechanical.

3. Geopolitical risk premium has been faded by the market and the over-extrapolation is unwinding. Geopolitical risk attribution to the S&P dropped from roughly forty percent at the lows to under ten percent now. The Marko Papic framework is doing exactly what it does every cycle: actual geopolitical risk events get priced into the market, the market over-extrapolates them, and three to six months later the premium gets faded. We are now in the fade phase.

4. The IGV positioning unwind is the cleanest setup for the next leg of the melt-up. IGV implied vol is at the same level it was at the prior lows, but IGV has not made a new low. That is a massive divergence. Call skew is rising in SMH. If IGV starts squeezing to the upside, equity long-short positioning has to unwind both sides of the trade, which mechanically forces buying in IGV and potentially selling in SMH. Microsoft is holding key levels and is the third largest weight in the index. If Microsoft and the broader IGV complex squeezes, the entire NASDAQ melts up further. Software is half of tech, tech is thirty five percent of the index, and the unwind has not happened yet.

5. The Russell is the cleanest range compression in the market right now and has the cleanest setup to break out. The Russell has tighter range compression than the S&P or NASDAQ. It is the structural recipient of the AI capex transfer because the Mag 7 are paying Russell-weighted companies to build the data centers. Capital is moving out the risk curve, and the Russell is where that flow has the most leverage. If we get a small pullback into FOMC, the Russell is the cleanest long expression on the bounce. If we just continue higher, the Russell breaks out of the range first and drags everything else with it.

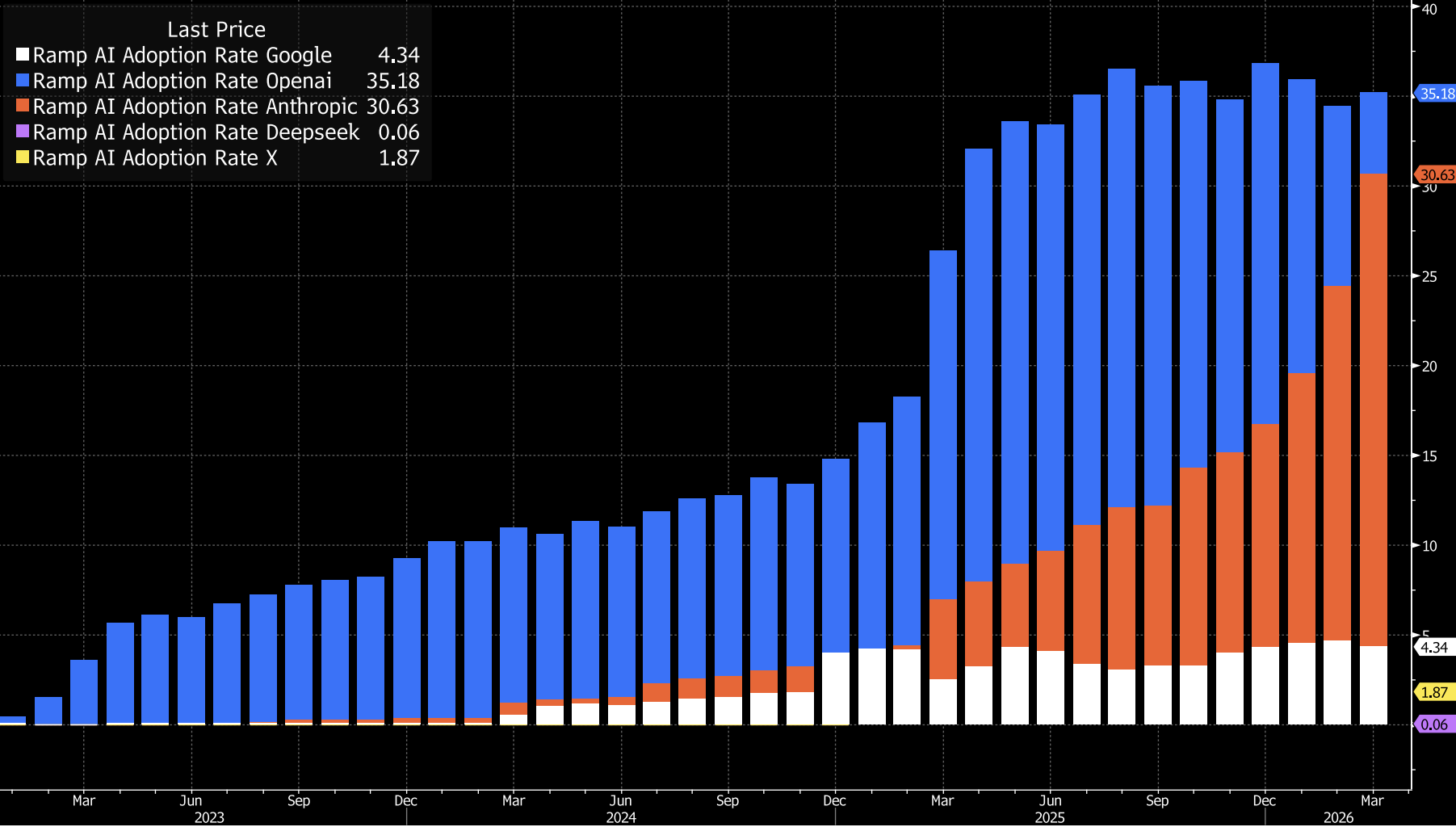

6. The Anthropic vs OpenAI market share chart is the most underpriced data set in the market. Anthropic is now at roughly thirty percent market share, just under OpenAI. The last two software-sector selloffs in IGV were caused by Anthropic and OpenAI model releases. With Anthropic gaining share and a higher IPO probability than OpenAI, the next inflection in the IPO window directly transmits into IGV positioning. This is why I am long Oracle. Larry Ellison hits the bid, sector flows turn, and the move compounds.

7. FOMC week setup: the PCE data is the single most important release. Energy spiked in the recent CPI print. The question is whether that pass-through hits core CPI or stays contained at headline. If core stays contained, the Fed pauses cleanly and real rates keep falling. If core reaccelerates, long-end rates blow out and we get a temporary pullback before the structural bid resumes. GDP this week also matters because it confirms growth is positive and not contracting through the inflation impulse, which keeps the Fed’s pause framework intact.

8. The three ways the credit cycle ends, and why none of them are happening right now. First way: recession from AI capex disappointment, layoffs, and delinquencies. Second way: long-end rates blow out from inflation pass-through, the Fed has to hike, and we move into a real bear market. Third way: cross-border flows reverse and you get the 2025 tariff-style dollar-and-equity selloff. None of these conditions are present right now. Capex is rising, delinquencies are non-existent, the Fed is pausing into supply-side inflation rather than hiking, and cross-border flows are still pushing capital out the risk curve. Until one of these three triggers, the structural bid stays intact.

Slide Deck and Playbooks:

Slide deck from livestream:

Additional charts I referenced:

Tomorrow’s Livestream: FOMC Setup: How Powell’s Last Meeting Reshapes the Real Rate Path

Tomorrow I map the full FOMC setup heading into Wednesday’s meeting. This is functionally Powell’s last meeting that matters before the Warsh handoff, and the way the curve is positioned for it is going to determine the next leg of the credit cycle melt-up.

See the breakdown I did of Warsh here:

TOMORROW’S LIVESTREAM: LINK

The information on this website/Substack is for information purposes only. It is believed to be reliable, but Capital Flows does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of Capital Flows websites and systems including but not limited to data scraping, unauthorized entry into Capital Flows systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by Capital Flows and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to Capital Flows or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of Capital Flows.

Great piece. Thanks for sharing your insights on this!