Macro Regime Tracker: Tariff Unwind

Macro regime and risk assets qualified clearly

The Macro Regime Tracker offers a daily lens on how shifts in growth, inflation, and liquidity affect short-term risk and reward. Leveraging machine learning, AI, and cross-asset data, it identifies macro changes and their impact on market positioning.

Macro Regime Tracker Index:

Macro Regime Context

Macro Tear Sheets: Equities, Fixed Income, FX, Crypto, and Commodities

Macro Regime Dashboard: Excel spreadsheet for economic data and interest rates

Growth, Inflation, Fixed Income, Credit, and Equities Regime Tracker

AI and Machine Learning Strategies - Macro Regime and Positioning Premiums Strategies: S&P 500, 2-Year Interest Rates, Gold, and Bitcoin

Macro Regime Context:

One of the main ideas I continue to put forward is that macro volatility is increasing. After cash equity close today, news came across the tape pushing back on Trump for all the tariffs. This immediately caused equities to rally and bonds to sell.

All of the tensions and views for interest rates and equities were laid out here:

Now, here is the thing: equities are rallying more than bonds are selling off. Why is this? Part of the reason is that we are getting a lot closer to the 25bps level in Z5, which means the market is pricing only 25bps of cuts by the Fed for this year. In other words, we still have a decent amount of time before the next FOMC meeting and we need to move through the GDP, PCE, NFP and CPI print BEFORE FOMC. All of the flows around SOFR and bonds move incrementally around these datapoints.

As we have ZT (2 year futures) grinding down, we are likely to see gold begin to rally again and push to new highs along with silver:

I believe we are going to push higher in CL as well:

My view on the long end of the curve has not changed. I believe we are going to see 30 year interest rates rise to new highs and begin to cause much bigger issues in macro land:

I will just say, every equity investor/trader doesn’t care about interest rates until it begins to blow up their portfolio. For now, equities remain skewed to the upside and I believe we could actually see a gamma squeeze to the upside in equities. But the move index just moved even lower reflecting greater and greater complacency surrounding interest rate risk.

All of this is while 1-year inflation swaps are above 3%. This is not a situation for a dovish Fed.

Through this entire period of time, the cuts of 2025 have just been rolled to 2026 instead of being completely taken out of the forward curve. In other words, the market just kicked the can down the road for cuts. If Powell begins to actually flip marginally hawkish, this would likely cause a real capitulation in Z6 to reprice to 75bps or even less.

Watching Z6 will be critical through the GDP print tomorrow and PCE print on Friday.

Main Developments In Macro

*US SUSPENDS SOME SALES OF JET ENGINE TECH TO CHINA: NYT

*US WILL BEGIN REVOKING SOME CHINESE STUDENT VISAS, RUBIO SAYS

*RBNZ'S HAWKESBY: WE'VE GOT INTEREST RATES NEAR NEUTRAL

*RBNZ'S HAWKESBY: WE'RE IN A GOOD SPACE IN TERMS OF INFLATION

*RBNZ'S HAWKESBY: COMMODITY PRICES COULD STAY HIGH FOR A WHILE

*RBNZ'S HAWKESBY: HIGH COMMODITY PRICES INSULATING NZ ECONOMY

*TRUMP ADMIN. CANCELS $3 BILLION LOAN GUARANTEE TO SUNNOVA

*RBNZ'S CONWAY: RECENT RISE IN INFLATION EXPECTATIONS NOT IDEAL

*RBNZ'S CONWAY: CONFIDENT INFLATION WILL SLOW AGAIN AFTER UPTICK

*HAWKESBY: REVISION REFLECTS WEAKER INFLATION OUTLOOK VS FEB

*RBNZ'S HAWKESBY: REVISION TO OCR FORECAST TRACK WAS MODEST

*RBNZ'S HAWKESBY: WE DO SEE GROWTH HEADWINDS IN NEAR TERM

*RBNZ GOVERNOR HAWKESBY SPEAKS TO PARLIAMENTARY COMMITTEE

*US TELLS SIEMENS EDA, SYNOPSYS, CADENCE TO STOP CHINA SUPPLY:FT

*TRUMP ORDERS US CHIP SOFTWARE DESIGNERS TO STOP CHINA SALES: FT

*WILLIAMS CONSTITUTION PIPELINE PROJECT ABOUT TO BE REVIVED: WSJ

*NY FED PUBLISHES STATEMENT REGARDING THE STANDING REPO FACILITY

*MANY FED OFFICIALS CITED FIRMS PAUSING, DELAYING CAPEX PLANS

*FED MINUTES: TARIFFS MUCH LARGER, BROADER THAN EXPECTED

*FED STAFF SAW RECESSION `ALMOST AS LIKELY' AS MAIN FORECAST

*FED WELL POSITIONED TO WAIT FOR CLARITY ON OUTLOOK, MINUTES SAY

*FED OFFICIALS SAW POTENTIAL FOR `DIFFICULT TRADEOFFS' AHEAD

*FED MINUTES: `CAUTIOUS APPROACH' APPROPRIATE AMID UNCERTAINTY

*ECB'S VILLEROY: MORE RATE CUTS POSSIBLE IN COMING WEEKS

*ECB'S VILLEROY: DON'T SEE INFLATION PICKING UP IN EUROPE

*TRUMP: IRAN DEAL COULD HAPPEN 'OVER NEXT COUPLE OF WEEKS'

*TRUMP ON TIKTOK DEAL: 'CHINA IS NEVER EASY'

*TRUMP REPEATS WILL HAVE TO GET CHINA APPROVAL FOR TIKTOK DEAL

*TRUMP: WOULD LIKE TO SAVE TIKTOK

*TRUMP: WOULDN'T SANCTION RUSSIA IF I THINK IT COULD HURT DEAL

*TRUMP: NOT HAPPY ABOUT CERTAIN ASPECTS OF TAX BILL

*TRUMP: NEED TO GET A LOT OF SUPPORT ON TAX BILL

*TRUMP: THINK WE'RE GOING TO SEE SOMETHING SENSIBLE WITH IRAN

*TRUMP: DOING VERY WELL WITH IRAN

*TRUMP: HAVING VERY GOOD TALKS WITH IRAN

*TRUMP: WILL FIND OUT IN TWO WEEKS IF PUTIN WANTS TO END WAR

*OPEC+ TO DISCUSS JULY OUTPUT HIKE IN SEPARATE MEETING ON MAY 31

Macro Tear Sheets: Equities, Fixed Income, FX, Crypto, and Commodities

Macro Regime Dashboard: Excel spreadsheet for economic data and interest rates

Growth, Inflation, Fixed Income, Credit, and Equities Regime Tracker

The Macro Regime Model offers a real-time view of growth, inflation, and yield curve dynamics, integrating these with credit market shifts, equity risk premiums, and positioning data. It connects upcoming catalysts to statistical drivers of asset prices, creating a unified framework that quantifies skew and clarifies risk-reward across asset classes.

Key Points To Set The Context:

S&P 500 Wrap — Index Declines -0.70%, Dragged Lower by Energy and Utilities; Real Estate Holds Ground

Sector-by-Sector Contribution Snapshot (Weighted Impact)

Information Technology (-0.22 pp) – Largest negative contributor, despite Nvidia’s strong earnings; broader tariff uncertainties weighed heavily on sentiment in the tech sector.

Financials (-0.10 pp) – Negative impact from continued pressure in bond markets, particularly at the long end of the curve.

Consumer Discretionary (-0.10 pp) – Pulled lower due to caution amid tariff uncertainties and potential impacts on consumer spending.

Materials (-0.02 pp) – Modestly negative amid ongoing commodity price volatility and uncertain global demand.

Communication Services (-0.04 pp) – Slight negative impact, reflecting broader market caution.

Industrials (-0.06 pp) – Down due to persistent concerns around global trade dynamics and weakening manufacturing outlook.

Health Care (-0.04 pp) – Mild negative influence reflecting broader market conditions and limited sector-specific catalysts.

Consumer Staples (-0.03 pp) – Slight negative contribution as investors reduced exposure amid defensive rotations.

Utilities (-0.03 pp) – Minor negative contribution, despite traditionally defensive positioning, highlighting overall weak market sentiment.

Energy (-0.05 pp) – Impacted by renewed uncertainty around global growth and energy demand forecasts.

Real Estate (~0.00 pp) – Essentially neutral, outperforming relative to broader market losses due to easing Treasury yields.

Sector-by-Sector Performance Snapshot (Unweighted Returns)

Energy (-1.76%) – Worst-performing sector, driven by concerns about weakening global economic outlook and energy demand.

Utilities (-1.31%) – Underperforming despite defensive nature, reflecting market-wide risk-off sentiment.

Materials (-1.11%) – Hit by ongoing volatility in commodity prices and uncertainty around global demand.

Consumer Discretionary (-0.93%) – Pressured by broader market sentiment despite positive Nvidia earnings.

Financials (-0.71%) – Negative performance, impacted by steepening yield curve pressures.

Information Technology (-0.68%) – Declined despite Nvidia’s earnings, with broader concerns around U.S.-China tech relations weighing on investor sentiment.

Industrials (-0.67%) – Soft performance reflecting uncertainty surrounding trade policy impacts and manufacturing outlook.

Consumer Staples (-0.46%) – Relatively moderate losses, reflective of typical defensive characteristics.

Health Care (-0.43%) – Mild losses in line with the broader market direction.

Communication Services (-0.38%) – Relatively stable compared to broader market weakness.

Real Estate (-0.02%) – Best-performing sector on a relative basis, buoyed by stable yields.

Macro Overlay

Market sentiment reversed negatively today despite a favorable overnight decision from the U.S. trade court blocking President Trump's global tariffs. Nvidia's positive earnings initially buoyed tech sentiment; however, broader market concerns around escalating regulatory pressures on semiconductor exports to China overshadowed individual stock positivity. Energy and Utilities significantly underperformed due to concerns regarding global growth prospects. Persistent upward pressure on long-term bond yields, exacerbated by fiscal uncertainties, further dampened sentiment. Federal Reserve caution, highlighting increased risks of both inflation persistence and economic slowdown, compounded these worries.

Bottom Line

The S&P 500 declined -0.70%, led downward by significant losses in Energy, Utilities, and Materials sectors. Despite isolated positive earnings results, including Nvidia’s upbeat guidance, escalating regulatory and macroeconomic uncertainties are likely to maintain heightened volatility and cautious market sentiment in the near term.

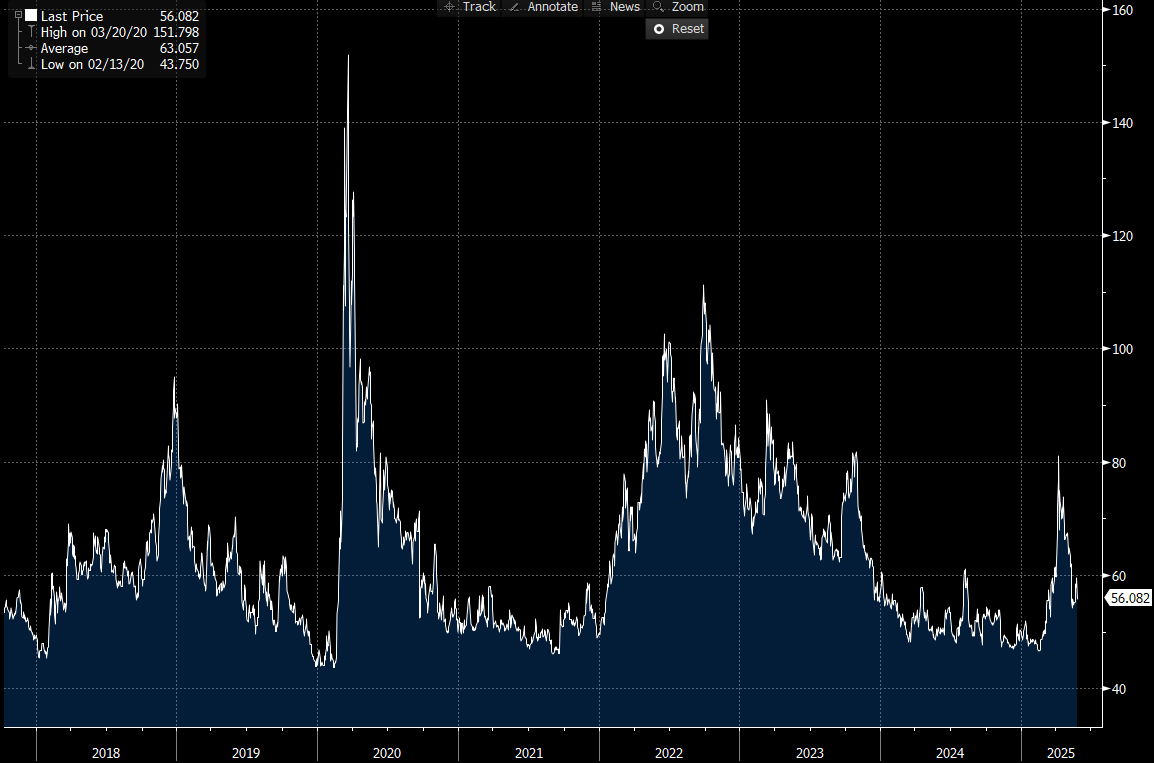

US IG Credit Wrap — Spreads Ease to 56.1 bp Amid Persistent Macro Concerns and Regulatory Uncertainty

Current Spread: 56.1 bp (▲ ~0.4 bp d/d), indicating slight widening amid cautious market sentiment. Spreads remain below the 5-year historical average (~63 bp), but ongoing macroeconomic and regulatory uncertainties persistently pressure sentiment.

Credit Context

< 60 bp: Pre-tariff escalation range: supportive of duration-heavy buyers (LDI, insurers).

60–70 bp: Tariff and fiscal uncertainty zone: neutral-to-cautious stance warranted.

> 90 bp: Severe stress breakout: still low probability.

Macro Overlay

Today's slight widening in IG credit spreads reflects increased investor caution amid regulatory uncertainties, particularly the Trump administration's potential tightening of semiconductor software exports to China. Despite an initially positive market reaction following the U.S. trade court ruling blocking global tariffs, broader market concerns resurfaced, driven by persistent pressures on long-dated Treasury yields and increased Fed vigilance regarding inflation persistence and economic slowdown risks. The cautiously constructive credit environment persists but is tempered by elevated macroeconomic uncertainty.

Bottom Line

IG credit spreads marginally widened to 56.1 bp, reflecting cautious investor sentiment amid renewed regulatory and macroeconomic concerns. The immediate risk environment remains stable yet fragile, with spreads likely to remain sensitive to evolving geopolitical developments and fiscal policy news. Directional bias is neutral-to-cautious, pending further clarity on regulatory and economic dynamics.

Mag7 Model:

Keep reading with a 7-day free trial

Subscribe to Capital Flows to keep reading this post and get 7 days of free access to the full post archives.