Macro Report/Insights: FOMC Day

Key charts!

Hey everyone,

There are some really important things to note after FOMC today.

Several Macro Topics:

FOMC "hawkish skip”

DOT plot upward revision

Market Reaction

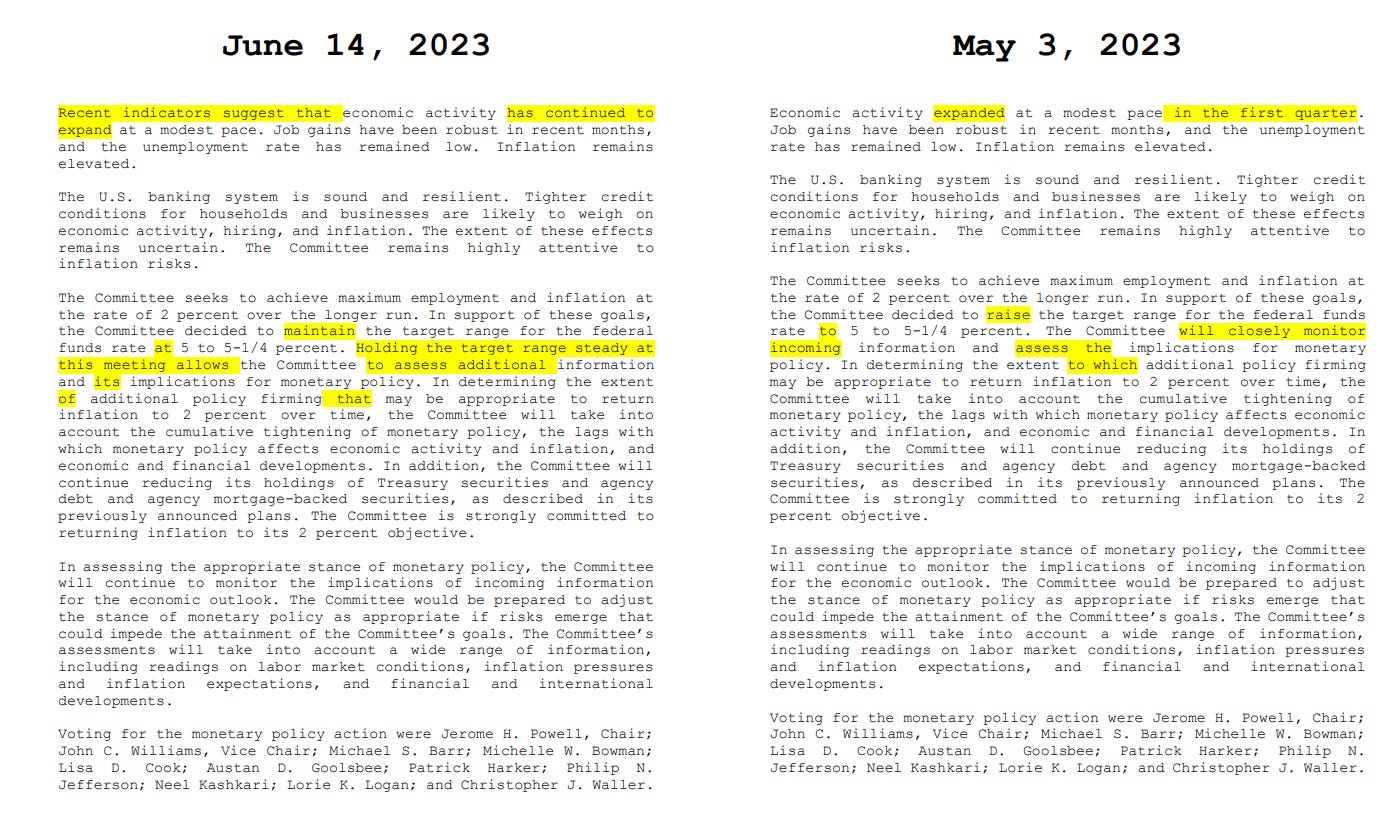

The FED left their target rate unchanged at FOMC today. The side-by-side comparison doesn’t show any significant changes in the language. Most doves are using this “pause” as a signal that the FED is done hiking. They assert that historically when the FED pauses, they are done hiking.

There are two points of discontinuity with the dovish view that the FED is done hiking. First, there was a unanimous vote for policy action today. Second, the dot plot was revised UP in the SEP today.

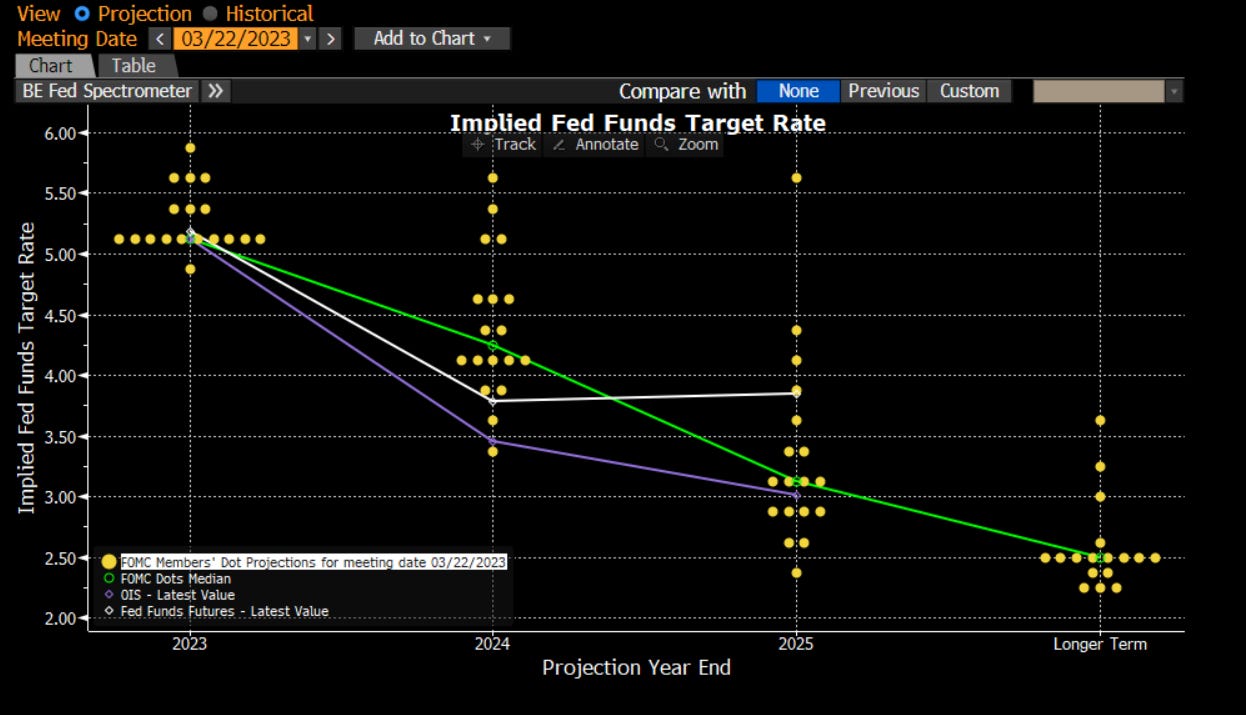

Here is the SEP from the March FOMC:

Here is the dot plot from today. We can see the majority of members are now above 5.50% with several participants closer to 6.00%.

This upward revision in the dot plot will be key for framing the FED speeches until FOMC in July. Here is the schedule for FED speeches between now and the July FOMC.

While Powell said they have not made a decision about the July rate hike, the dot plot seems to bias the decision to the upside.

While we didn’t have a rate hike today, it was the SEP’s impact on the forward curve that caused the sell-off in bonds. We now have the July meeting pricing with a 62% probability of a hike in July. Given the dot plot revision, two more 25bps rate hikes are well within the distribution of probabilities.

As we move into the next month, the FED speeches are likely to provide further confirmation of the pricing of the forward curve. This in turn is likely to cause the yield curve to flatten more.

10-year yields have reasonably strong resistance at the 3.90%-4.00% level:

However, if we price 2 more rate hikes into the forward curve, the 2-year yield could move above the level where the SVB banking crisis occurred.

When we look at credit spreads and the 2 year, we still have a very large gap (see the report where I explained this relationship here: Link). Until credit spreads move up to close this gap, equities are unlikely to have considerable downside driven by macro factors:

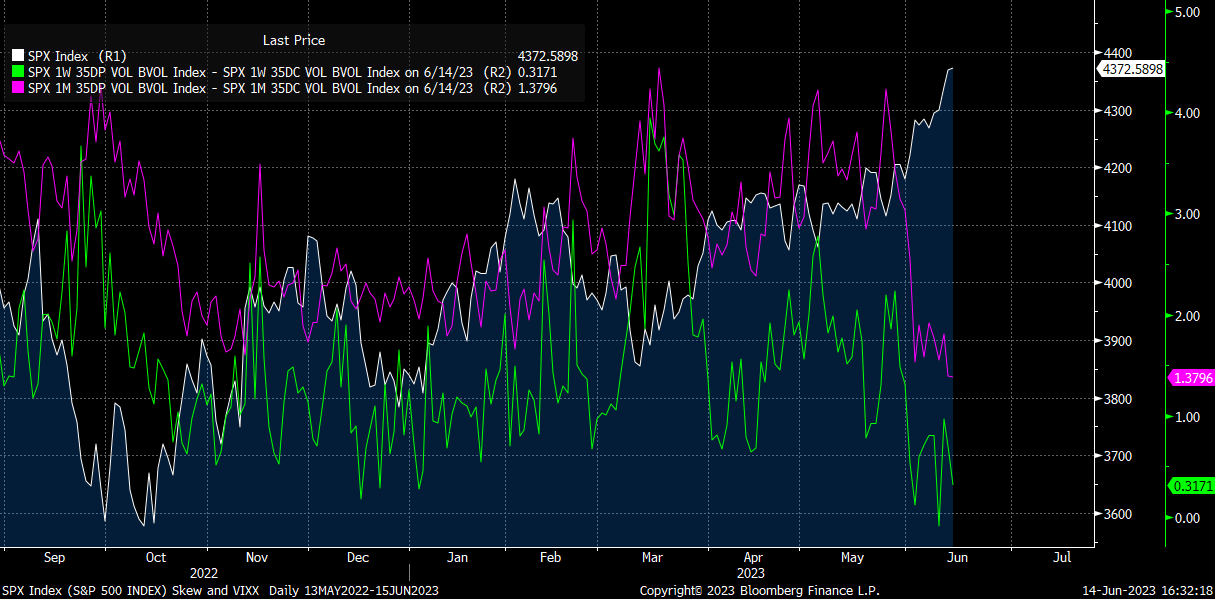

We continue to see volatility expressed in the VIX and SPX skew remain incredibly low.

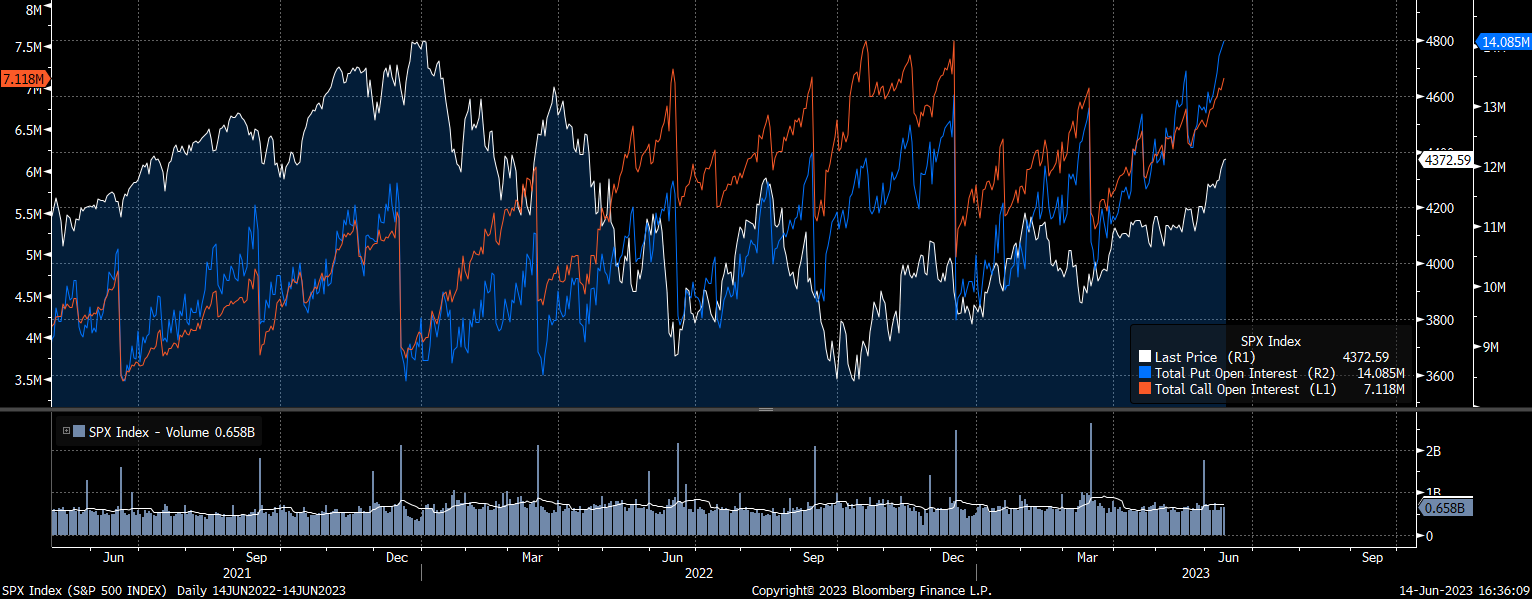

Total call and put open interest are moving up to incredibly high levels:

Friday is opex and we are likely to see some considerable moves in positioning:

Bottom line:

We are likely to see continued upside in the 2-year yield with the 10-year yield remaining below its resistance as the yield curve flattens.

The FED speeches will provide additional confirmation for the forward curve in pricing the next two meetings.

Option open interest is incredibly high as we move into Opex on Friday. However, we need to see a pronounced move in credit spreads to cause a durable bearish move in equities.

Conclusion:

I will be providing more analysis and trades surrounding these topics for Paid Subscribers. Right now, I think there some are exception risk/reward opportunities setting up in gold, the dollar, and potentially equities.

Thanks for reading!

In the information age, you simply need to be at the right place, at the right time, with the right information to succeed

When will you give an update on your trades for gold and the USD?

Hello sir, I just came across your substack lately and I really love it. I´m not a total newb to markets, but I lack options market knowledge. Where can I learn the things you use in your option analyses? When it comes to books, most are about the basics or basic option strategies, but not about the internals like in today´s post where you mentioned calls and puts open interest moving up. Best Regards Veroni