NVDA Earnings Is THE Catalyst For This Week

Can global geopolitics hinge on NVDA earnings?

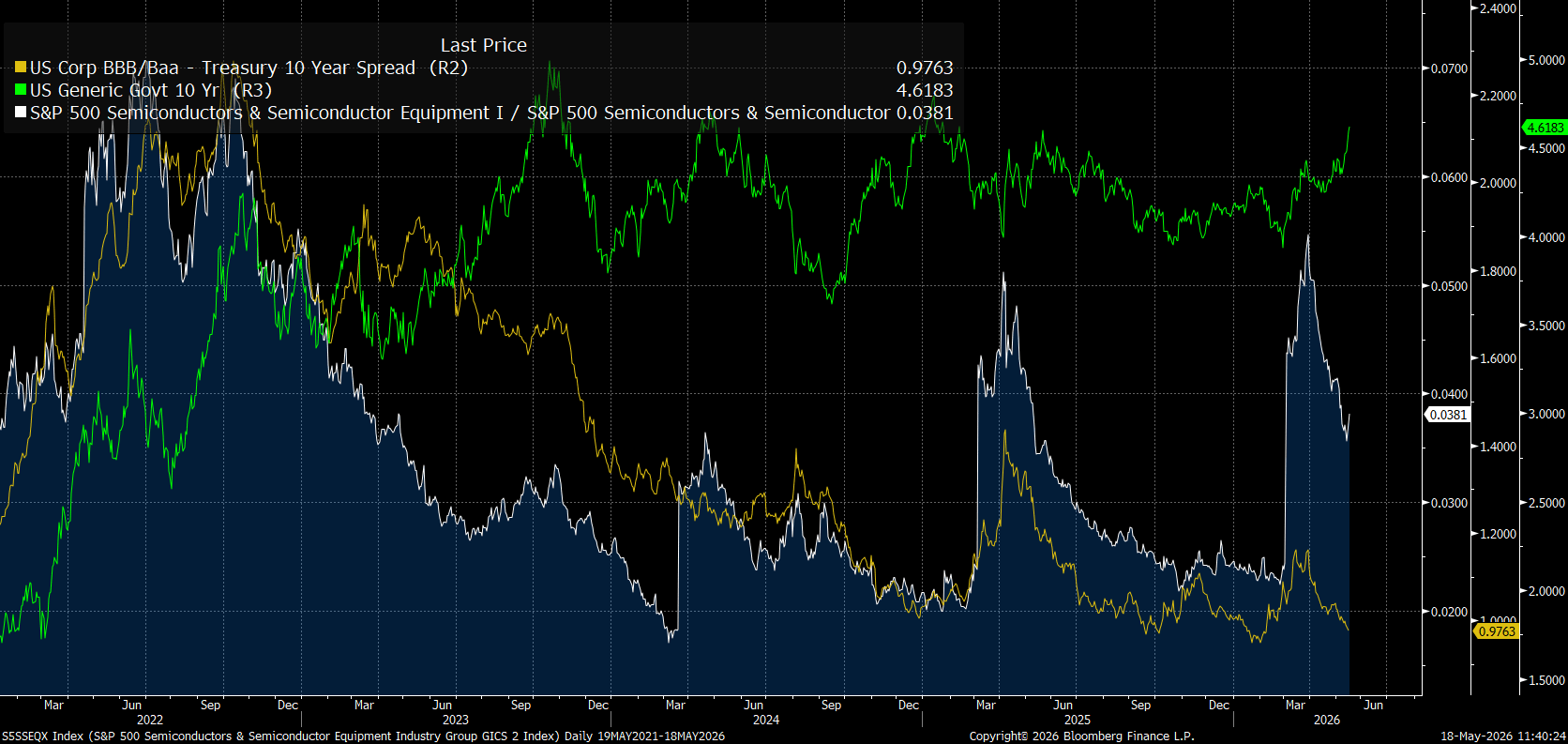

Today, Jaymes and I broke down the dispersion between semiconductors and software, the cybersecurity unwind in Palo Alto and CrowdStrike confirming the February report, and the full earnings setup for Nvidia, Intuit, Workday, Home Depot, and Lowe's this week. The SMH ETF is melting up with implied vol rising at the same time as price rises, which is the commodity-like price action that only happens when capital is forced to participate. Inflation risk is still greater than recession risk, stocks over bonds remains the framework, and the entire question of the week is whether Nvidia delivers the AI capex affirmation the market needs.

LIVESTREAM RECORDING FROM TODAY:

Today’s Livestream: Main Talking Points

1. The SMH ETF is functioning like a commodity with implied vol rising alongside price. In a normal equity setup, vol rises when price falls. In SMH right now, vol is rising as price rises, which is the same dynamic crude shows when traders are forced to buy calls to cover exposure. Companies and capital cannot afford to not be long the AI build out, which mechanically forces them into the same names. That is a commodity flow pattern overlaid on equities.

2. The IGV dispersion thesis is playing out exactly as I laid out in the February report on cybersecurity. Palo Alto and CrowdStrike were sold indiscriminately with the broader software complex on the AI disruption thesis. Both are now ripping to new highs as the dispersion separates winners from losers. The names with proprietary data moats are emerging as the winners. The ones without are staying suppressed.

3. IGV implied vol is at the same level as January, which means the market is pricing a very wide outcome range for software. When vol stays elevated this long without resolving in either direction, you have a positioning setup where any earnings catalyst that injects clarity into the moat question forces a massive vol crush. The Intuit print this week is the catalyst to watch.

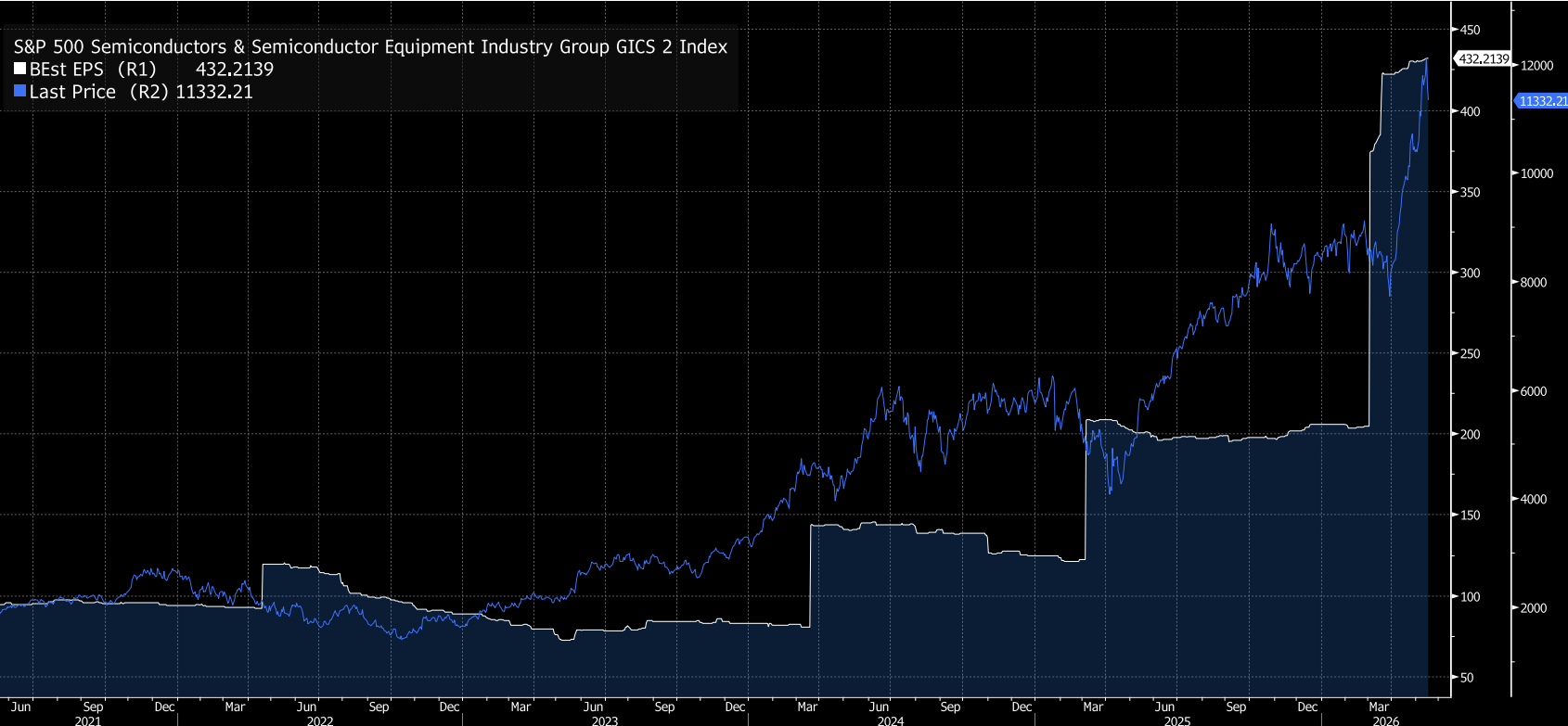

4. Nvidia earnings this week determine the next leg of the AI capex flow. Watch for any signal from Jensen on China developments. If geopolitical risk in the AI space drops further after the Trump-Xi meeting, that is an immediate bid across the entire complex. Positioning is heavily long Nvidia, which means the bar is high for the report to extend the move. But the broader capex flow is what matters more than the single name.

5. PURR continues to be the cleanest expression of the Hyperliquid thesis with no VC overhang and no aligned promoters. No VCs got an early allocation because there was no allocation. Anyone with public commentary on Hyperliquid is not paid to pump it. The absence of coordinated promotion is the cleanest signal that the value proposition is structurally underpriced. Goldman Sachs initiating a position and a single buyer taking a million shares last week are the early institutional confirmations.

6. SPY versus RSP concentration is widening into Nvidia earnings, which is characteristic of a melt-up. The top names are absorbing the marginal flow because the AI capex theme is concentrated there. The equal-weighted index will lag as long as that concentration continues. Late-stage melt-ups feature this exact pattern and the unwind happens when rates spike or positioning catches offside.

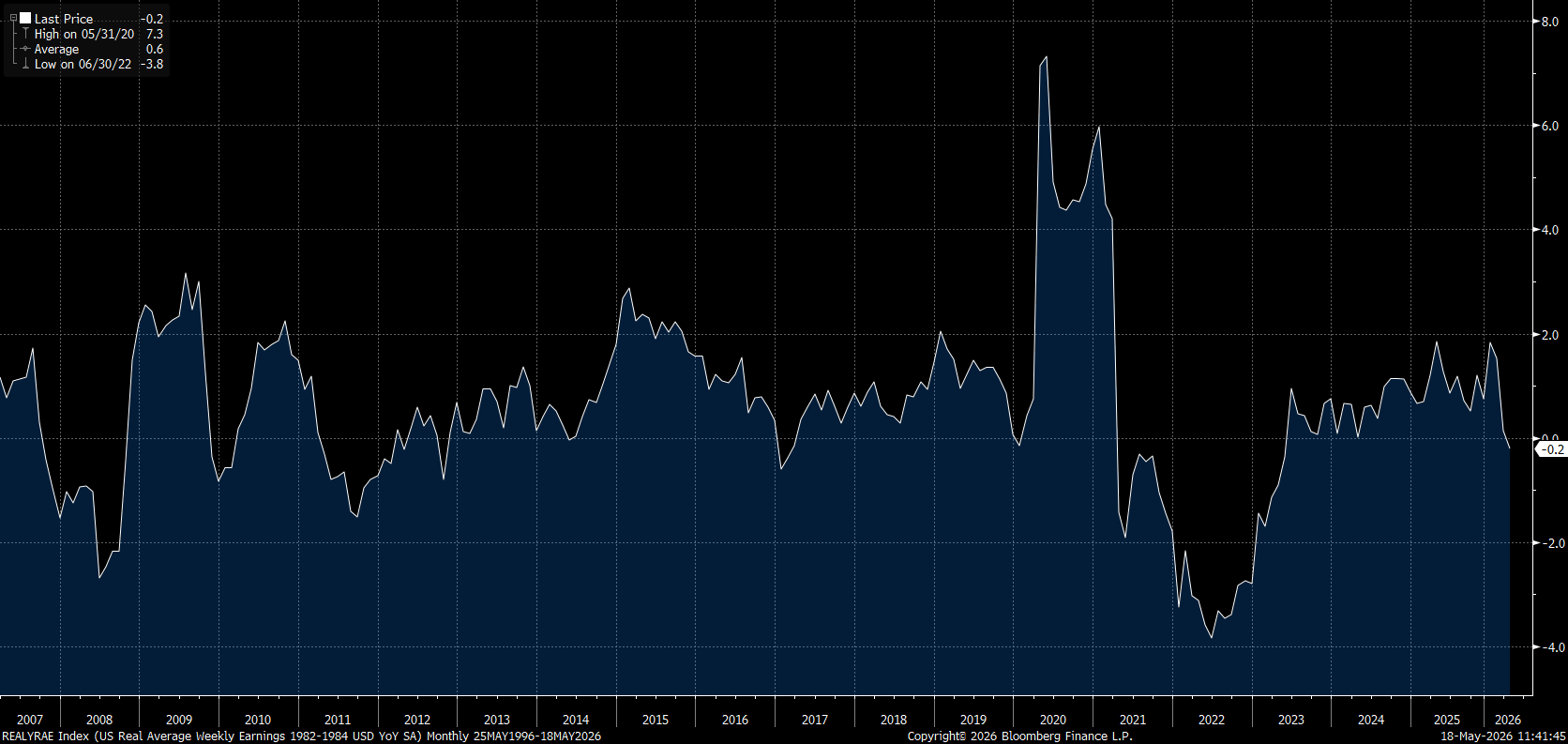

7. Inflation risk is still greater than recession risk, which means stocks over bonds remains the framework. Headline CPI is ticking up, core is not transmitting yet. Inflation swaps are sitting at the highs while real rates compress. As long as the Fed stays inactive into rising inflation expectations, real rates fall and capital keeps moving out the risk curve. The melt up extends until the transmission breaks.

8. The two main sectors to watch for the consumer transmission are housing and staples through Home Depot, Lowe’s, and Walmart earnings. Mortgage rates ticking up is putting marginal pressure on home builders. Home Depot and Lowe’s move in lockstep with the home builder complex. Walmart prints give the cleanest read on food inflation through groceries. These earnings confirm or refute the consumer resilience thesis underlying the broader credit cycle framework.

Slide Deck and Playbooks:

Here are all the decks and charts from today’s livestream: Positioning breakdown, earnings analysis, and TSMC asymmetry for chip buildout.

Tomorrow's Livestream: Is China Trying to Become the Next World Power and How Are They Attacking the Global Stage Through Economic Warfare

Tomorrow, I break down how China is actively trying to become the next world power and the specific economic warfare tactics they are deploying to attack the US and the global stage. Yuan suppression, rare earth controls, dollar substitution narratives, and the AI supply chain dynamics are all part of the same coordinated playbook. I map what is actually happening and what it means for cross-border positioning.

TOMORROW’S LIVESTREAM: LINK

The information on this website/Substack is for information purposes only. It is believed to be reliable, but Capital Flows does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of Capital Flows websites and systems including but not limited to data scraping, unauthorized entry into Capital Flows systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by Capital Flows and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to Capital Flows or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of Capital Flows.

Agree on NVDA as this week’s pivot but the SOX correlation to SPX sits at 0.72 over the past 60 days. A hot print probably moves the broad tape more than just QQQ.

NVDA single name catalyst risk feels priced in by now. The bigger tell is hyperscaler capex guides and AVGO commentary. Insider activity at the picks and shovels names is where the asymmetry sits.