SOFR, Interest Rate Volatility, and Macro Endgame

LIVESTREAM/PROPIETARY REPORT

The livestream today broke down HOW the SOFR curve, meeting date volatility, and front end rate pricing set the interest rate risk that governs equities, the yen, and macro liquidity right now.

Main takeaways from the livestream:

For the first time in years the market genuinely cannot decide if the Fed’s next move is a hike, with the July 29 meeting priced near a coin flip at 66% hold and 34% hike and roughly 51 basis points of hikes priced to terminal. The forward curve, not sentiment or consensus, is WHAT tells you the Fed path.

The December 2026 SOFR contract is now the largest contract by open interest in SOFR history, with open interest up 28% in just over two months. The Z6/Z7 and Z6/Z8 calendar spreads price only 6 and 14 basis points of cuts, so if the Fed overtightens into disinflation those spreads have to reprice sharply lower, which makes them the daily one stop read on the front end.

Rate volatility does not flow evenly through time, it pools at FOMC meetings and data catalysts and goes quiet between them. Interest rate vol sitting this low is WHY higher rates are not contracting liquidity, and with CPI next week expected to show disinflation, equities are skewed to drift higher between catalysts.

The recession narrative fails the data test: nominal GDP is running at 5.8% against 2% real, ISM manufacturing has accelerated for five to six prints, and industrials and financials sit at all time highs. ITB up 2% year to date versus the S&P up 11% is normal credit cycle rotation, nothing like the 70% homebuilder collapse that warned in 2008.

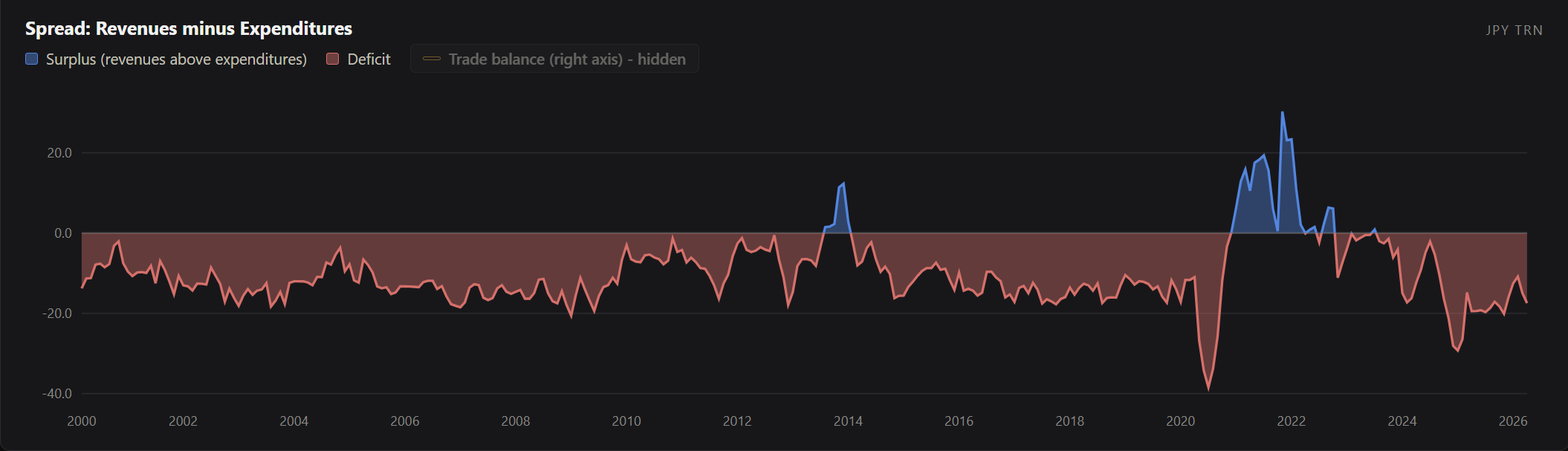

Japan is funding heavy government spending with bills at the short end WHERE real rates are negative, around negative 38 basis points on the two year. Every Japanese saver in short term debt loses money in real terms while the Ministry of Finance wins, and that transfer is the mechanical reason the yen keeps devaluing. Japan’s government deficit:

CME single stock futures launch this month on names like NVIDIA, Microsoft, Oracle, and Palantir, bringing 24/5 trading and futures margin efficiency to single names. That changes hedging flows and overnight risk expression, and it feeds the same cross collateralized IPO flows that let Cerebras set both a top and a bottom in NVIDIA.

You can find the free recording on the SOFR and Interest Rate Volatility Playbook here in the YouTube video:

The member section connects this framework to the live regime and positioning, with the recording linked at the bottom of this report.

Macro Decks From today’s stream:

Monday’s Livestream: The American Exceptionalism Trade

The livestream for Monday (no stream tomorrow) will take on the American Exceptionalism trade, the question of whether USD reserve status, the rise of global trade, and the US innovation hub remain the critical bet as global rebalancing takes place. It will map HOW those three pillars channel capital flows and WHERE the pressure points sit as the rest of the world competes for that capital.

Paid subscribers can join the livestream with this link (the first half will be free and streamed to Twitter and YouTube, where the second half will only be available on Substack for paid subscribers):

Proprietary Report On SOFR, Interest Rate Volatility, and Macro Endgame

Keep reading with a 7-day free trial

Subscribe to Capital Flows to keep reading this post and get 7 days of free access to the full post archives.