The Crowded Exit

How macro catalysts are setting up for a short term inflection

FOMC and the Positioning Risk In Inflation

Markets are pricing geopolitical risk as a short-term inflation accelerant, which is pushing rate cut expectations lower and raising the specter of stagflation. Dollar strength reflects this dynamic precisely: short-end inflation expectations (1y and 2y swaps) are rising while real rates climb on the long end (10y and 30y), a combination that has been mechanical support for the currency.

We are approaching a critical inflection. FOMC this week creates a binary setup. If geopolitical risk fades and crude sells off, or if the Fed signals less concern about inflation on the grounds that the current move is supply-driven rather than demand-driven, the market’s hawkish repricing could unwind quickly. Either catalyst would likely produce equity buying and dollar selling. That reversal would carry extra force right now, given how elevated implied volatility is, which tells you hedging premiums are stretched and any shift in sentiment gets amplified as those positions unwind.

I explained the mechanics of the dashboard above, along with an extensive breakdown of the macro regime in the livestream earlier today. You can find the full recording here:

Positioning is one-sided:

The chart crystallizes the positioning argument. Crude call skew (white) has surged to levels not seen in years, reflecting aggressive demand for upside protection in oil as markets price a geopolitical supply shock into the inflation narrative. Crude implied volatility premium(yellow) has followed, confirming that the entire options surface in energy has repriced higher, not just the directional skew. Simultaneously, SPX put skew (green) has reached comparable extremes, as equity investors have rushed to protect against a growth shock. EURUSD put skew (magenta) completes the picture, with the market heavily positioned for continued dollar strength against the euro.

What makes this moment genuinely unusual is that all four measures have spiked in unison, suggesting the positioning is cross-collateralized across asset classes rather than idiosyncratic to any single market. Traders are hedging the same macro thesis simultaneously in crude, equities, and FX, which means the trade is crowded from multiple directions at once. This is the setup heading into FOMC. The pause itself is not in question, with the forward curve pricing it as a certainty, but the December 2026 contract has been repriced down to roughly 17 basis points, essentially less than a single cut. The real question Powell faces is whether to push back on that repricing and restore some easing optionality for 2026, and if he does, the unwind of this correlated hedge stack could be sharp precisely because so many positions are leaning the same way at the same time.

The Z6 SOFR contract (showing the markets expectations for how many cuts this year) is sitting at 17bps as the terminal rate is pricing a total of 35bps of cuts for this cycle.

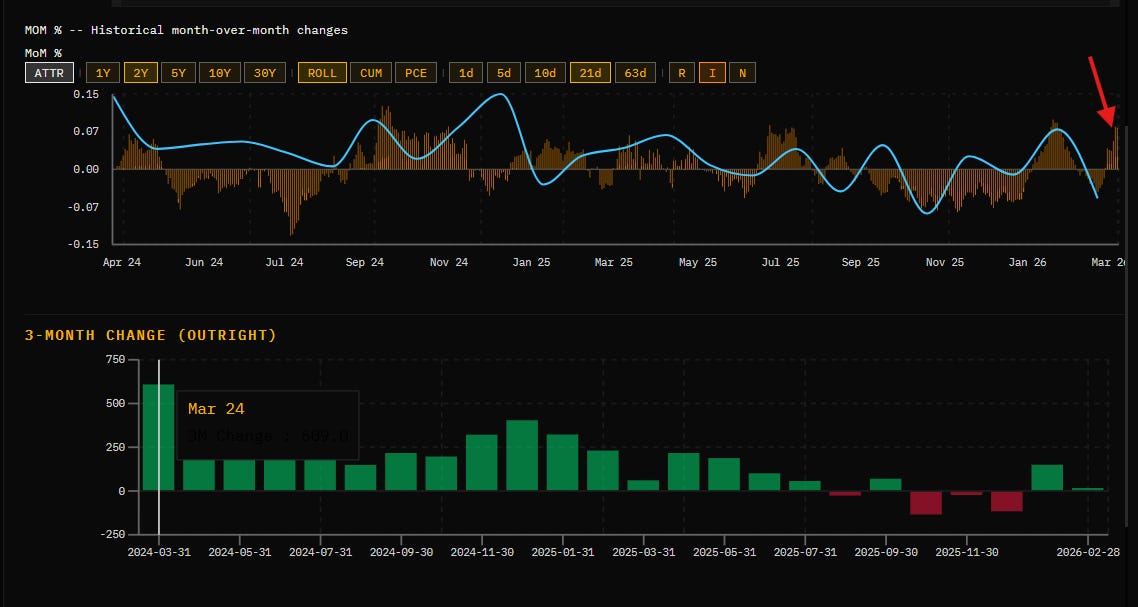

The problem with this pricing is that, as I laid out in the livestream (link), the growth side of the equation is at more risk since the labor market is near the zero bounds of growth. 3-month change in NFP (bottom panel) is functionally a coin flip, and the most recent MoM NFP print (blue) was negative just as the inflation impulse in markets accelerated (visualized by the orange bars in the background).

The FOMC meeting this week carries a genuine double tension. Inflation is accelerating at the same time growth is under threat, but the inflation impulse is supply-driven rather than a reflection of excess nominal demand, which complicates how aggressively the Fed can respond. Layered on top of that is a deeper uncertainty: markets do not know how to weight Powell’s forward guidance when he is likely months away from being replaced, which leaves positioning one-sided with no clear anchor. The smallest shift from Trump on trade or geopolitics could be enough to trigger an aggressive unwind of the cross-asset hedge stack that has been built up across crude, equities, and FX simultaneously.

Tomorrow’s Livestream

What I have laid out here is the map, but the map is not the territory. The cross-asset positioning picture is clear enough. What is not clear is the sequencing, because the order in which these catalysts arrive changes everything about how the unwind plays out and which instruments express it most cleanly.

There is a specific problem with trading around a crowded hedge stack: everyone sees the same positioning data, which means the consensus trade on the unwind is also getting crowded before the catalyst even arrives. Tomorrow I want to work through how to think about that second-order problem, where the real opportunity is not in predicting Powell but in understanding what the market is already pricing as its escape route and whether that consensus unwind trade is itself mispriced.

We will go deep on the rates structure, what the Z6 contract is actually telling us about the market’s implicit Fed reaction function, and how I am thinking about expressing this across the curve rather than in a single instrument. If you have been following the inflation swap divergence between the short and long end that I walked through above, tomorrow is where that framework gets applied to actual positioning decisions.

Noon EST at this link:

Thanks

The information on this website/Substack is for information purposes only. It is believed to be reliable, but Capital Flows does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of Capital Flows websites and systems including but not limited to data scraping, unauthorized entry into Capital Flows systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by Capital Flows and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to Capital Flows or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of Capital Flows.

I don't think folks are getting it... Trump has fully lost control of this war. It is not up to him to end it. In fact, he's now in a position to have to give CONCESSIONS to reverse it. The greatest fk up in US history.