Top Down/Bottom Up, FED, BMR

BMR (Bear Market Rally)

There have been a couple of things I have been giving considerable thought to this week. Several have to do with the current market environment and several have to do with thinking correctly about markets (or any domain of life).

Let’s start with markets:

So we had FOMC this week where Powell made a decision about setting the FED Funds rate. Interestingly enough, people have become a bit too focused on the FED as of late. When the guy at the gym who doesn’t work in markets asks you what you think about Powell doing 25bps vs 50bps, you know there is way too much focus on them.

The significance of the rate hikes is changing the time value of money. If you are thinking about buying a stock you need to take into account the fundamentals of the company as well as the time value of the currency those fundamentals are denominated in. For example, if a company’s cash flow is increasing, its stock price could still go down if the value of those cash flows is decreasing/increasing in real terms. A good example of this was last year when earnings remained relatively flat across the board but Powell increased the value of dollars by hiking interest rates which caused risk assets to go down. Cash flows=flat but the value of those cash flows=up in real terms which = asset prices down.

The implication of this is that you need to take into account both the fundamentals of whatever you are buying/selling as well as the time value of money. Both impact asset prices.

Why BMR?

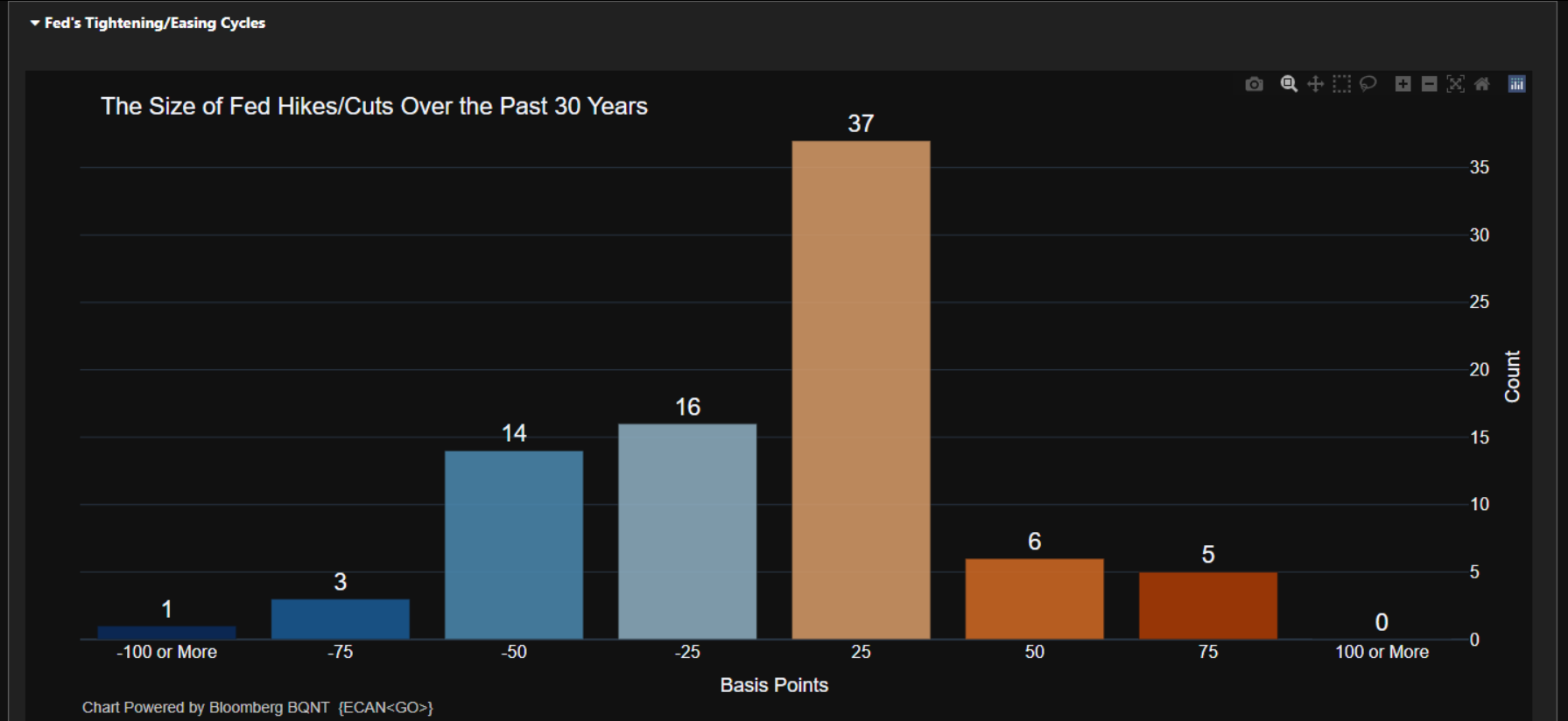

As we moved into Q1 we had one of the most violent bear market rallies (BMR) since this bear market began. Why? Let me break this down because it is the combination of a couple of factors. First, the FED embarked on one of the fastest hiking cycles ever in history. In markets, the speed and rate of change at which things occur are incredibly important for expectations and asset prices.

We can see that the “regular size” of rate hikes over the past 30 years has been 25bps. Does it make sense now why the market puked when Powell was doing 75bps last year? Yeah, not normal.

So when we go from really fast hiking to “holding rates flat” liquidity increases on a marginal basis.

The other dynamic is that growth is slowing but not as fast as everyone expected. A lot of people thought a recession and a bottom in equities would occur in Q1 of 2023. So there was a lot of cash on the sidelines.

Now there is a lot of positioning long the market with the expectation that we are back to normal because the FED is done hiking. If you want a fuller breakdown of this, the macro report I wrote breaks this down fairly well.

What is happening from here?

I am waiting for an opportunity to short equities again. When that time comes I’ll provide a breakdown so you can see how to think through this. It’s not as easy as everyone makes it look though.

Holding the 2-year is still an amazing deal here because you get paid over 4% to hold “risk-free” treasuries. I provided a link to the write-up I did on that in the macro report.

We remain in a period of time where there is considerable volatility which means holding a high allocation of cash or actively taking tactical trades are the best options. Again, not investment advice!

Thinking about markets and life:

I find that people usually appreciate learning how to think more than a hot take on the market. So let’s do a little bit of that:

You will usually see people in markets say they either take a “top-down” or “bottom-up” approach to the economy or markets.

For example, you hear the top-down guys say that it’s hard to predict all the small moving parts but if you can get the big moves right, you can do really well. And usually, the top-down guys are focused on major moves in growth, inflation and liquidity to nail big moves in stocks, bonds, or currencies.

Then you have the bottom-up guys who say that no one can predict the economy cause it’s to complex so they stick to finding really good situations or companies with strong fundamentals.

Both guys have their time to shine. If you actually look at the performance of these different types of funds, they go in and out of favor. For example, global macro funds usually have really good returns when we have a lot of volatility in growth, inflation and liquidity. Inversely, the fundamental guys usually do well when the market is in a stable bull market because they get to outperform based on their fundamental stock picks.

It’s not wise to be critical of managers’ returns simply because of their seasonality. Its more important to identify which managers/funds are likely to perform best in the given environment.

The way that I think about this:

I view these approaches as similar to inductive vs deductive reasoning. While these two forms of reasoning are different, the way I like doing things is by having inductive and deductive thinking in a constant feedback loop in my analysis to either confirm or falsify my thesis about the world.

So I run macroeconomic models on the entire economy and I also run bottom-up fundamental models on each asset. In my mind, if both the macro models and bottom-up fundamental models are saying the same thing, that is when I want to take a larger bet on something occurring.

This is the same thing as in any domain of life. Let me provide an example: there is a pretty large headwind to produce microchips since supply chains and deglobalization are putting pressure on chips. So you have a top-down thesis that supply chains and deglobalization are likely to presist and that will provide headwinds for the sector depending on how it has exposure to supply chains. If you want to look into this more, Peter Zeihan has some great books and Youtube videos on it.

So within this macro view, if you can find an additional bottom-up view in a specific location with a specific edge then it only increases your ability to make money. Granted, this means you need to have really high-quality information flowing to you from top-down and bottom-up sources. This is why many corporations pay a lot of money for macro research that informs them about cycle risk. At the end of the day, you want to align yourself with as many factors as possible.

Bringing it together………

So when thinking about markets or any situation, knowing all the various things that could impact it during different periods of time is critical. I am very thankful I have developed a skillset in macroeconomics and markets because I could very easily find an amazing headwind or bet and just switch jobs to get long a specific company or country by working/living there.

A small final note about markets: ever since options became a much larger part of markets, their expiration has become important for turning points in risk assets. Notice there are a ton of various expirations in two weeks. I wouldn’t be surprised to get a short signal from my strategies sometime around then.

Thanks for reading