Asset Class Report: Credit

Are there underlying risks in the credit market?

Every asset class is inherently connected but there are always varying degrees of transmission and sensitivities between them. Mapping these sensitivities through ALL macro regimes is the key to interpreting price action correctly.

Check out the bond report because it contextualizes the tensions for credit risk!

Bond View Update!

An important point I continue to reiterate is that we are in a higher nominal growth environment and there is very unique tension in bonds. The days when you could just buy bonds and be long are over. Active management is critical for managing bond exposure in 2024. While many economists and media figures talk in extremes, alpha is generated by monitoring the tensions and adapting dynamically.

Credit Report:

The previous macro reports (link) have consistently shown how economists and many market participants are incorrectly quantifying the underlying tensions in the economy. Many commentators continue to assert that an imminent recession is likely or that “under the surface” things are falling apart. Taking the other side of this trade in financial markets has proved incredibly profitable as equities make all-time highs, treasuries don’t have a 2020 type bid, and credit spreads tighten.

While it is incredibly easy to see consistent patterns in past economic cycles, there is always uncertainty and difficulty quantifying one’s current place in the economic cycle and HOW LONG a specific macro regime will persist. Further complexity is added with the structural shifts we see in deglobalization, onshoring, new trade partners, labor market tightness, and decreased sensitivity the economy has shown to monetary tightening (see previous macro reports for more on this). Additionally, the degree of path dependency continues to be undervalued by market participants for a potential reacceleration in inflation.

This report is intended to focus on credit risk throughout the economic cycle and the current conditions that exist in the credit market. The report will also show the current risk-reward for credit as we approach Q2 2024.

Big Picture Cycle:

Credit risk is directly connected to the growth cycle because it reflects the underlying risk in cash flows produced by growth. Credit risk also functions in a reflective feedback loop with growth as decelerating cash flows are amplified by higher credit spreads and decreased credit issuance. This reflective feedback loop directly connects with the path dependency we are likely to see in 2024.

Historically, credit spreads exhibit a persistent rise BEFORE an actual recession takes place. Credit spreads are currently decelerating well below their historical median which has two implications. First, this encourages participants to take out additional credit. Second, it reflects the resilient economic growth of the economy.

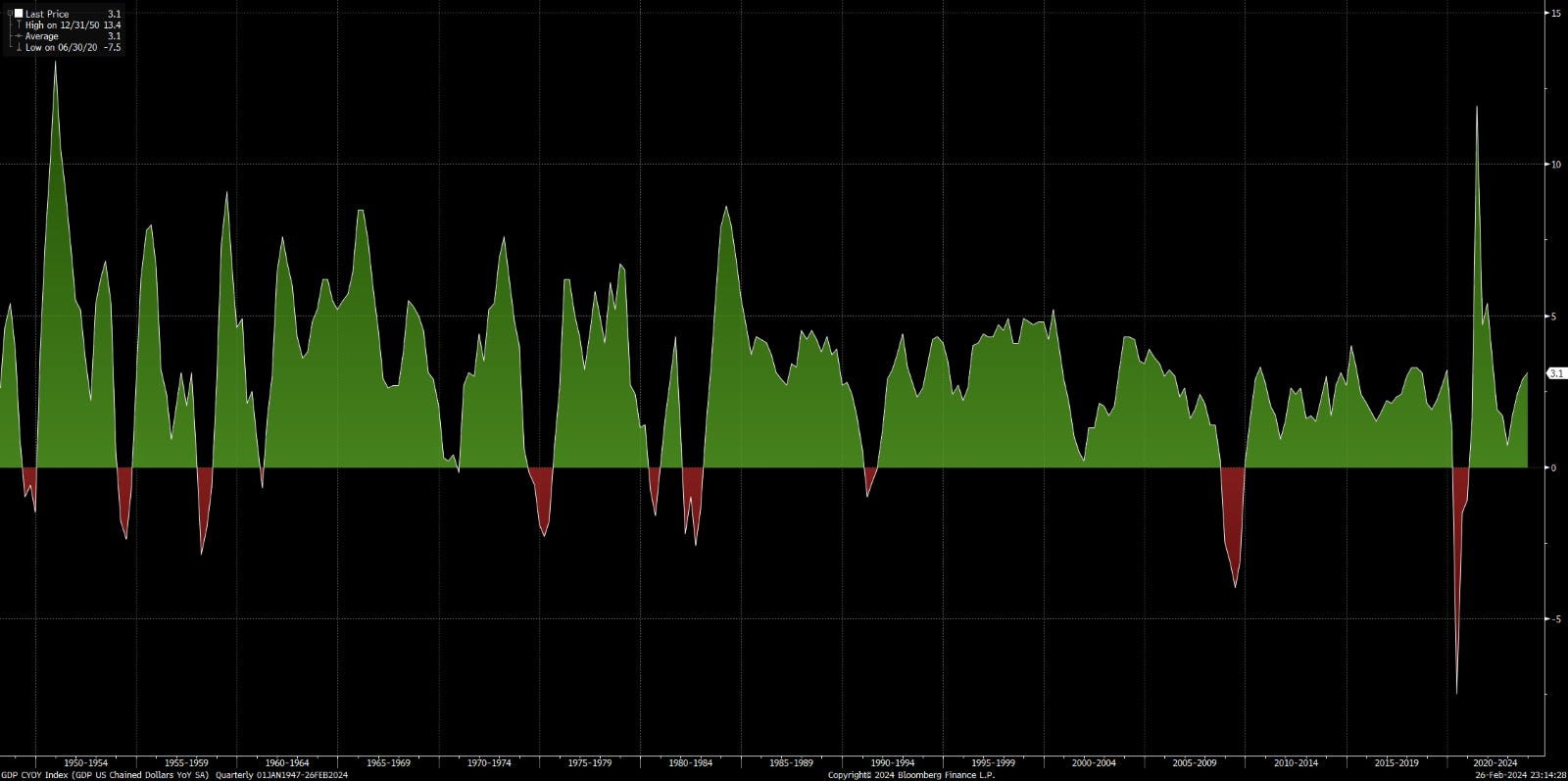

A persistent rise in credit risk will be reflected in three specific things: 1) The outright level of economic data decelerating. 2) A pervasive deceleration of economic data across all sectors of the economy. 3) the rate of change in economic growth being squarely negative.

The level of economic data is clearly positive with real GDP running at 3.1%:

While diffusion indices such as the Manufacturing and services ISMs have decelerated, they are now in the process of marginally reaccelerating:

The services PMI has remained above 50 for the majority of 2023 while the manufacturing sector is now reaccelerating from its lows:

Context post-COVID:

Bankruptcies always have a lagged effect with credit spreads which is illustrated in the current cycle. 2020 functioned as a significant clearing event for companies as bankruptcies accelerated to elevated levels. As the extreme measures of monetary and fiscal policy were implemented, bankruptcies decelerated considerably with credit spreads. As we moved into the 2022 hiking cycle, many of the companies that were produced by the low-interest rates and loose monetary policy began to be cleared from the system. You can see in the chart below, there was a significant rise in credit spreads in 2022 which was followed by bankruptcies in 2023. Now both bankruptcies and credit spreads are making a pronounced and persistent move down.

Keep reading with a 7-day free trial

Subscribe to Capital Flows to keep reading this post and get 7 days of free access to the full post archives.