This report is not an explicit prediction. It is an attempt to explain what it would look like if the current energy shock were to metastasize into a global recession, one that reverberates through the financial system in a manner that has no clean precedent. There is a difference between those two things, and that difference is the whole point.

To be clear, I do not think this is going to happen. And I will confess I am not among the clever ones who spent the last month long oil and short equities, nursing that position like a grievance until it paid. My largest exposure has been in the Hyperliquid ecosystem (link and link), which has quietly benefited from the geopolitical volatility and sits as one of the few assets up year to date, while Mag7 and Bitcoin are both in the red. I raise it only because the most dangerous thing in markets is a framework built backwards from a position.

The Architecture Assumes It

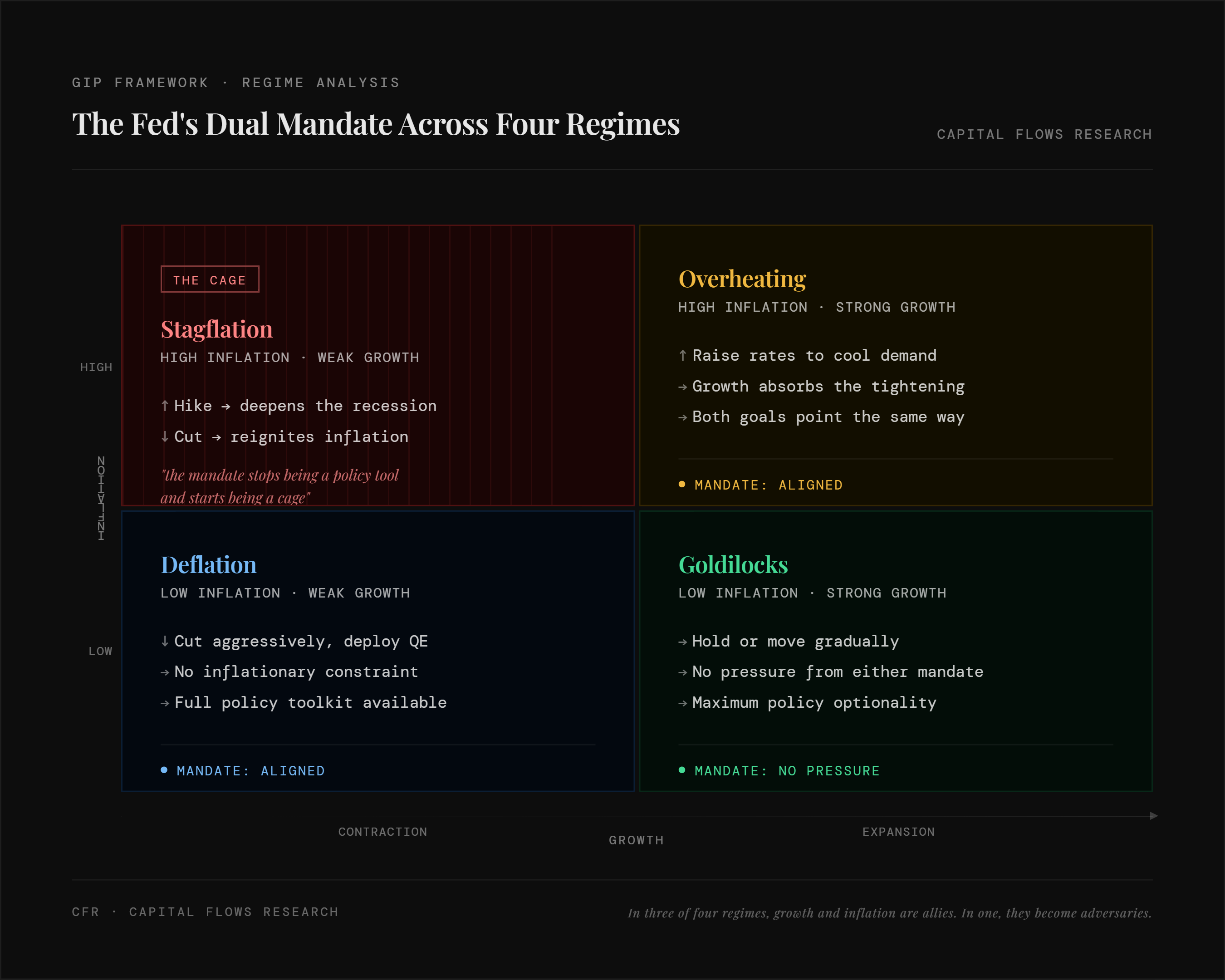

A supply shock is one of the few economic events that breaks the normal rules. In most environments, growth and inflation move together: the economy runs hot, and prices rise, or it cools, and they fall. Policy is designed around that relationship. The entire architecture of modern central banking assumes it.

What do we hear from the Fed? “Our dual mandate is maximum employment and stable prices.”

The dual mandate assumes growth and inflation are allies. In three of four regimes, they are. In one, they become adversaries, and the mandate stops being a policy tool and starts being a cage.

That cage is not theoretical. Since the late 1990s, stagflationary pricing has appeared in markets less than 10% of the time. It is the rarest regime in the table below, and it carries the worst return profile for the assets most people are holding.

This is exactly the moment we are in right now. The reason volatility is so elevated, and the reason people are so afraid, is not that a recession is certain. It is that we are in the one regime where the Fed cannot do anything about it without making something else worse.

The Transmission Chain

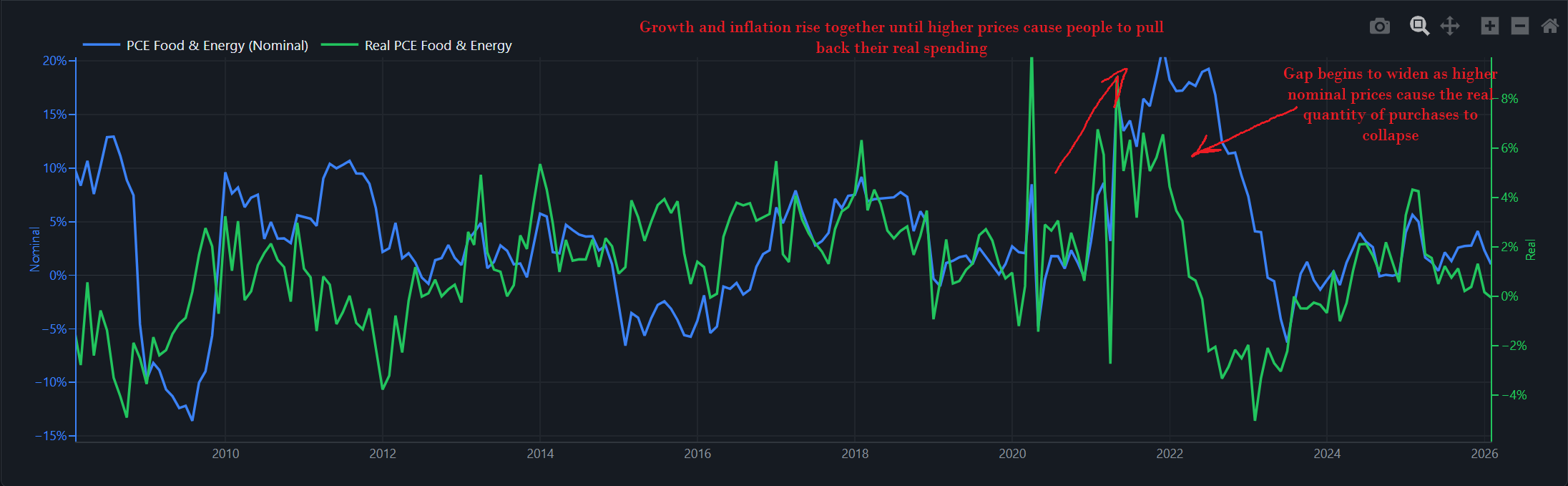

The chart below shows nominal and real spending on food and energy components of the economy. In dollar terms and quantity terms, it shows how much the American consumer is actually spending versus how much they are being charged. When growth and inflation rise together, higher prices do not immediately destroy demand. People absorb them. They grumble, they ask for raises, and they keep spending. That is what happened in 2022, and it is why the Fed was able to hike into that environment without triggering an immediate collapse. Real spending was running at nearly 8% year over year. The economy could take the punch.

We are now sitting at roughly 2% year over year real spending (vs. 8% when the last energy shock happened in 2022).

In 2022, the Fed hiked into an economy with enough momentum to absorb tighter financial conditions. Today, the cushion is gone. If another inflation impulse arrives now, through the food CPI lag that historically follows an energy shock by three to six months, the Fed faces a policy environment with no clean exit. Hike into 2% real spending and you risk cracking the consumer entirely. Hold and watch inflation re-accelerate, and you confirm the cage.

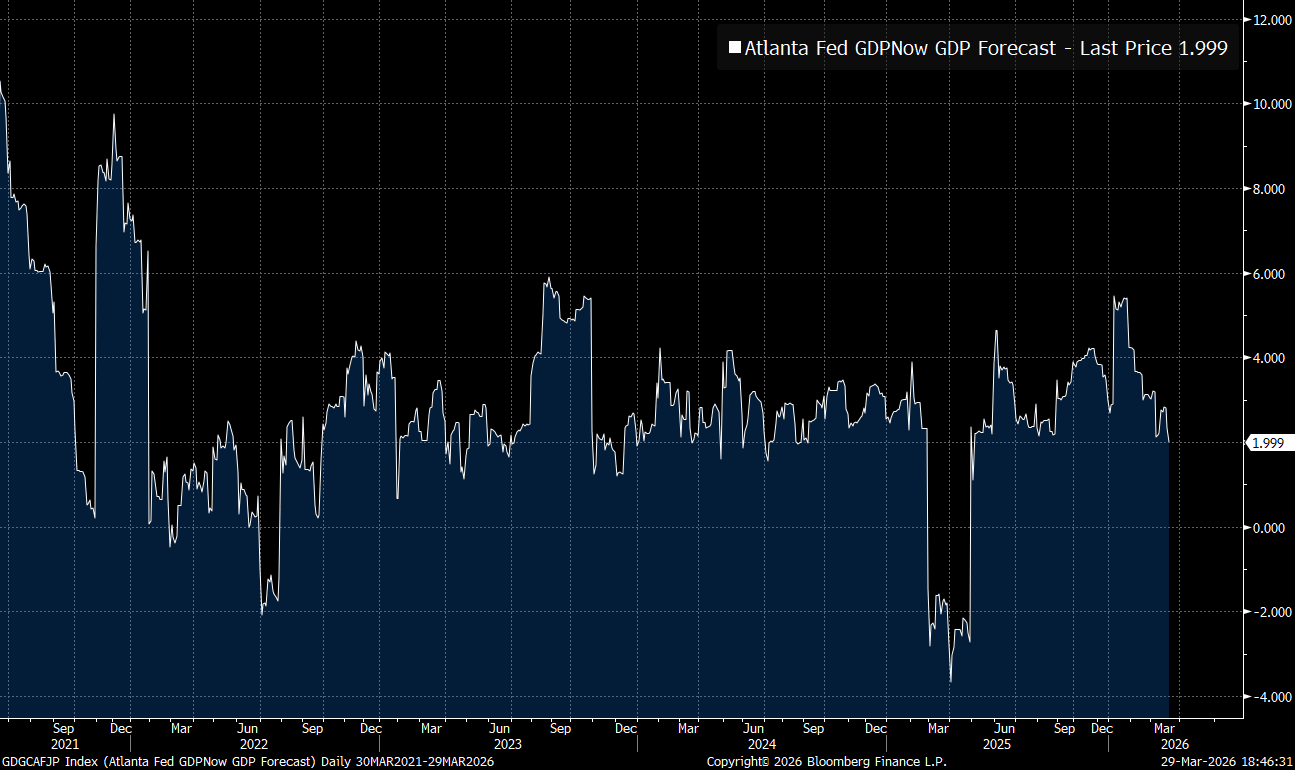

The Atlanta Fed GDPNowcast just crossed below 2%.

The Geopolitical Layer

There is a version of this analysis that stops at the commodity price. Oil is up, input costs rise, central banks are constrained, growth slows. That is a complete enough framework for a lot of portfolios. But it is worth at least acknowledging that the energy shock does not exist in a vacuum.

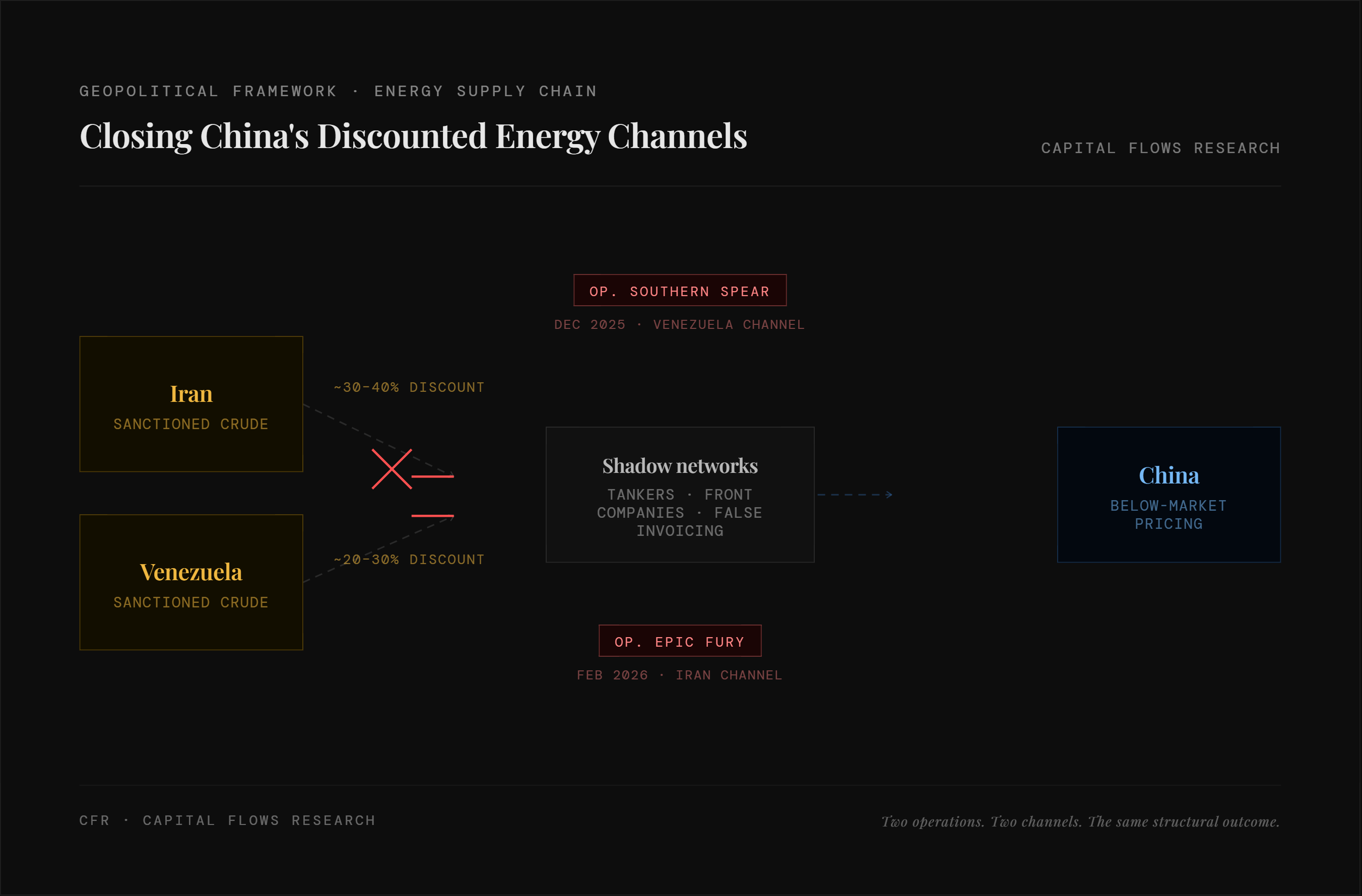

The United States has spent the better part of two years systematically closing off the channels through which China was accessing discounted energy — Iranian crude, Venezuelan crude, both flowing through shadow networks at well below market rates. Whether Operation Epic Fury was designed with that strategic dimension in mind or whether it simply accelerated an outcome already in motion is a question above my pay grade. What I can observe is the structure of what is happening around it.

The headlines about Jared Kushner operating simultaneously as Trump’s chief negotiator in the Middle East and as a fundraiser seeking $5 billion from Gulf sovereign wealth funds — the same funds belonging to governments he is negotiating with — have been framed almost entirely as an ethics story. I am less interested in the ethics question than in what the behavior reveals about the underlying logic. Kushner is not an idiot, and the people around him are not improvising. When the dealmaking layer is this active this fast, it tells you something about how this administration understands the relationship between military action, economic leverage, and capital flows. Trump is not swinging from the hip. There is a sequence being worked.

For our purposes, the relevant point is narrower: the oil shock is not a random weather event. It has authors and beneficiaries. That matters for how you think about its duration and the policy response to it.

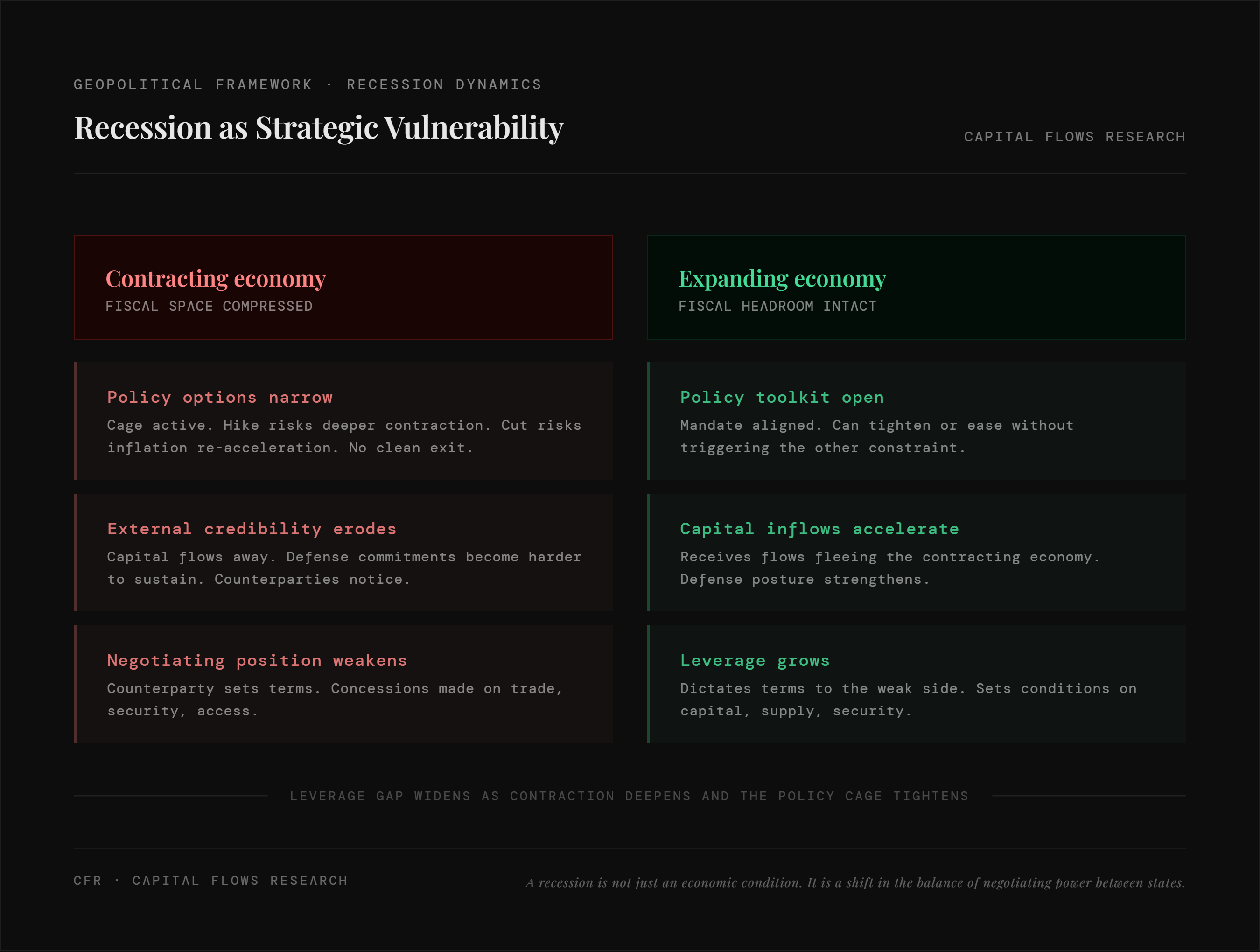

Recession as Strategic Vulnerability

The standard recession framework is economic. Output contracts, unemployment rises, and central banks respond. The framework I want to use here is different. It takes the geopolitical incentive structure seriously alongside the economic one.

A recession is not just an economic condition. It is a shift in the balance of negotiating power between states.

The mechanism is straightforward. A country in recession faces a simultaneous compression of fiscal space, political capital, and external credibility. Its government cannot commit resources it does not have. Its central bank cannot normalize policy without worsening the contraction. Its negotiating counterparties — in trade, in security, in capital markets — know all of this, and they price it into the terms they offer.

The country that avoids the recession, or even just avoids it longer, sits on the other side of that equation. It gets to set terms. It attracts the capital flows that fled the contracting economy. It accumulates the strategic leverage that the other side had to spend down just to stay solvent.

This is not a novel insight. It is the oldest logic in statecraft. What makes the current moment unusual is that the mechanism is running in an environment where the central banks of the major importing economies are already constrained by the cage we described earlier.

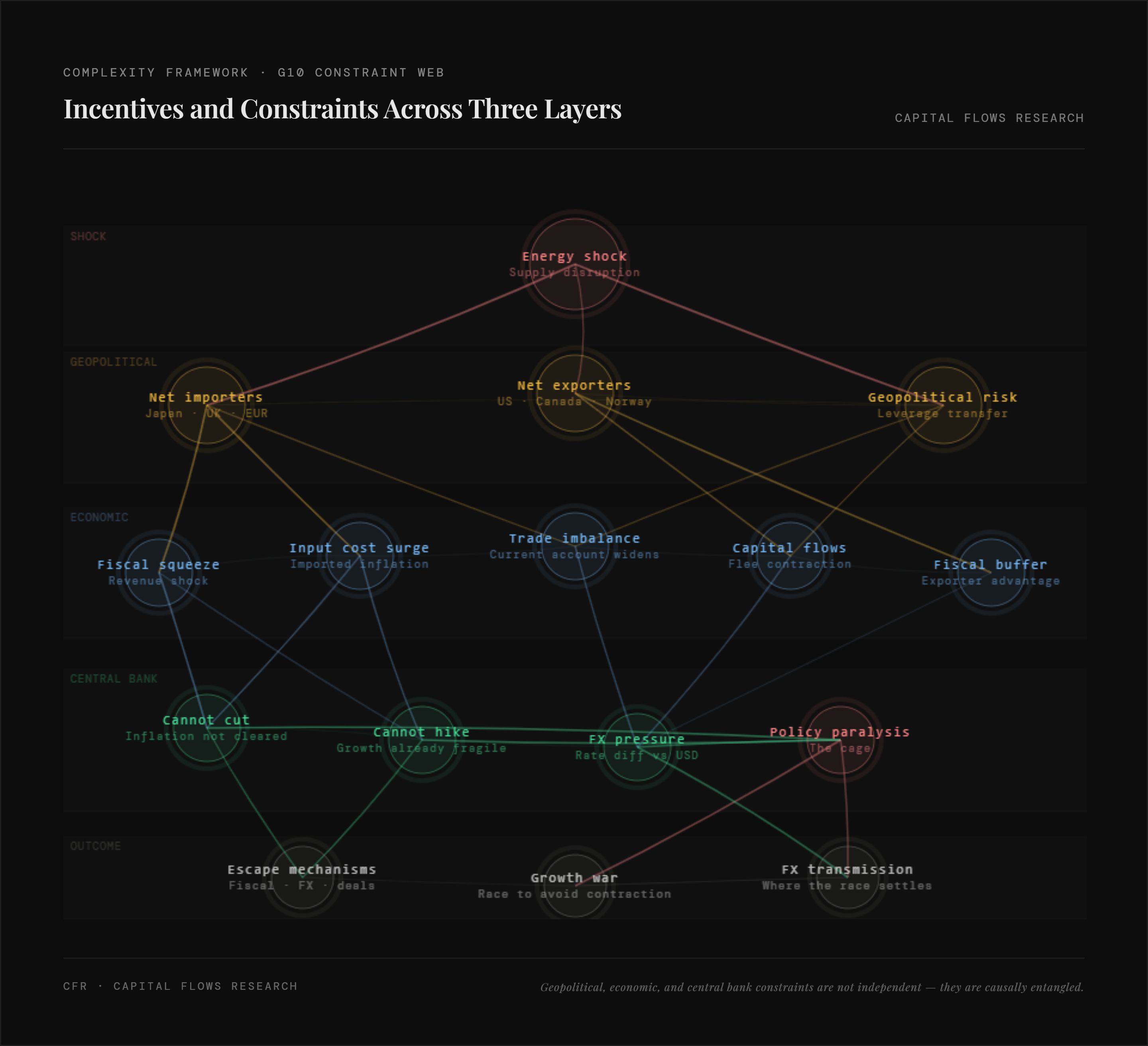

The G10 is not a uniform block in this environment. It is structurally divided by energy position. The United States, Canada, and Norway produce more oil than they consume. When the crude price rises, their energy sectors expand, and their central banks face a domestically different inflation profile than the countries on the other side of the ledger. Japan, the United Kingdom, Germany, France, Italy, and most of the eurozone are net importers. Every dollar move in the crude price transmits directly into their input costs, their trade balances, and their headline CPI. They are short oil in a world where oil is being used as a geopolitical instrument.

The cage lands differently on each side. A net exporter facing stagflationary pressure globally still has a revenue cushion and energy sector employment to absorb the shock. A net importer facing the same pressure gets the inflation without the offsetting income. Their central banks cannot stimulate freely because inflation has not cleared. They cannot tighten further because growth is already fragile. The constraint, structurally speaking, bears differently on the net importers than it does on Washington.

Geopolitical, economic, and central bank constraints — and the incentives running through each

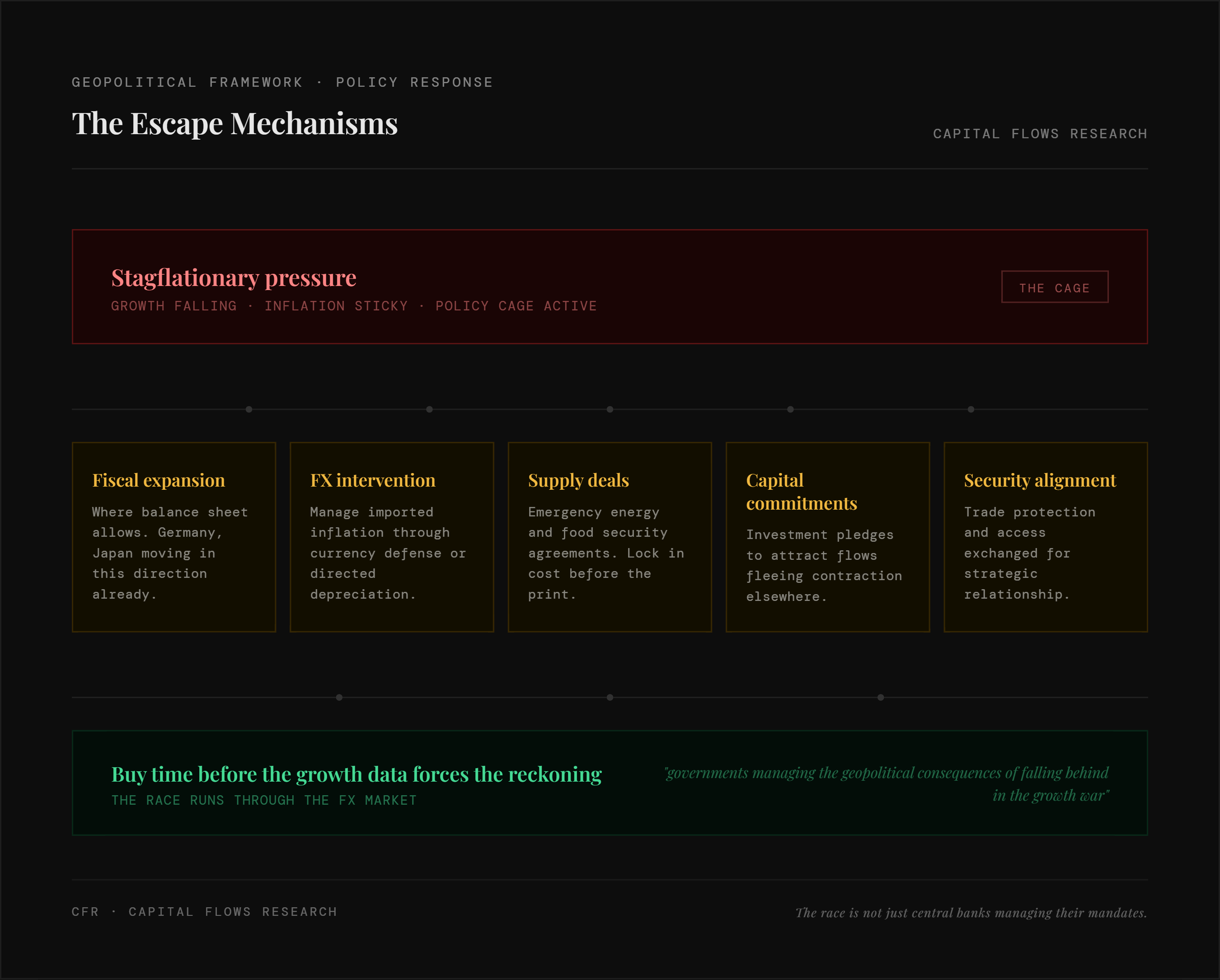

At the geopolitical level, the relevant frame is not competition between the importing economies. It is the relationship between the importing economies and the powers that benefit when they weaken. A country in recession becomes a more accommodating trading partner, a less credible security guarantor, and a more attractive target for the kind of patient, long-duration influence that China in particular has demonstrated it is willing to deploy. China does not need to attack a weakening economy. It needs only to wait, offer financing, lock in supply relationships, and extract the kind of structural dependencies that are only available to a counterparty negotiating from strength into weakness. Recession is the condition that makes that possible. Avoiding it is therefore not just an economic objective — it is a strategic one. Every government in the net-importer bloc understands this, even if they do not say it in those terms.

At the economic level, the incentive is to buy time before the growth deterioration forces a more disorderly response. Supply agreements lock in input costs before the next inflation print arrives. Investment pledges attract capital flows that would otherwise price the contraction risk and leave. Trade arrangements substitute for price mechanisms that have been disrupted. None of these are clean solutions. All of them are preferable to the alternative, which is arriving at the negotiating table in a recession.

At the central bank level, the constraint is the most visible and the least tractable. Cutting into inflation that has not cleared risks embedding it further. Holding while growth deteriorates risks a demand collapse that makes the next easing cycle far more costly. The added complication for the net importers is that their inflation profile is partly a function of what the Fed does regardless of their own stance — their currencies move against the dollar as rate differentials shift, which means the cage tightens or loosens partly based on decisions made in Washington, not in Frankfurt or Tokyo or London.

What the framework above describes, taken together, is an environment where the standard central bank reaction function is broken, where governments are substituting fiscal and diplomatic action for monetary policy, and where the capital flows that result are not being driven by yield differentials alone. They are being driven by which economies are successfully escaping the constraint and which are not. That distinction — who is in the cage and who has found a way out — shows up in FX first. It is the market that prices the gap between where policy needs to go and where it is actually permitted to go. And in an environment where that gap is widening across the major importing economies simultaneously, cross-border positioning is not a secondary question. It is the primary one.

Pulling All The Pieces Together:

The question worth sitting with is not whether a recession is coming. It is whether the governments and central banks of the major importing economies will permit one. The last time a demand shock of this magnitude created an opening, China used it. The 2020 recession was the moment China cemented its position as the dominant exporter of goods. That foothold was not taken by force. It was taken because everyone else was managing a crisis, and China was managing a strategy.

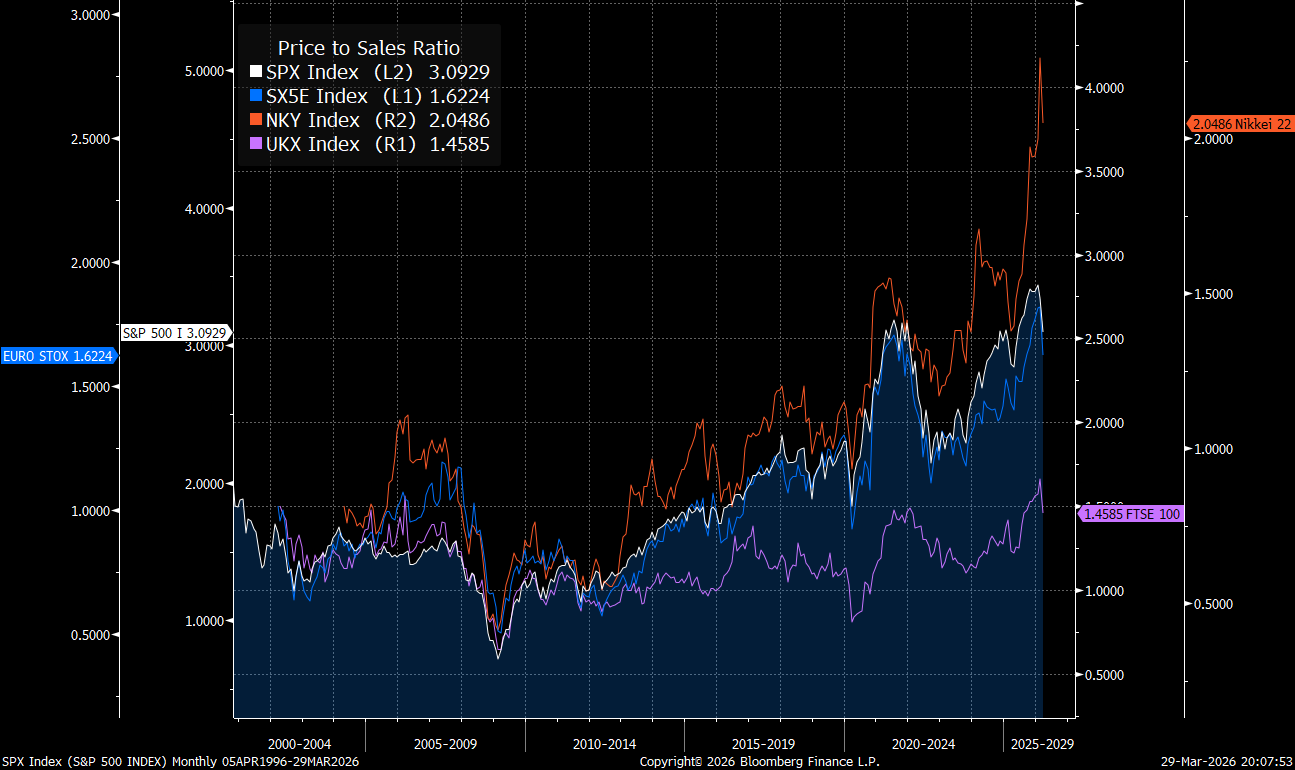

The central banks facing the cage today know this history. Which means the more interesting question is not whether they will hike into a supply shock and risk a recession. It is whether they will quietly allow liquidity conditions to loosen — tolerating financial asset inflation, letting valuations run — rather than accept the political and strategic cost of contraction. The equity valuation chart above is one way of reading that choice. Markets may already be pricing the answer.

I believe that once consensus and all of the economic talking heads on the news realise they’re missing the forest for the trees, there will be a violent change in markets that shakes FX and rates first and then reverberates into an aggressive chase into gold and silver as the inaction by central bankers speaks louder than any rhetoric games they can play at press conferences.

I believe we are entering the final innings of the endgame for both the macro picture and geopolitical stage.

Tomorrow, Part 2. FX and rates are the instruments that price the constraints and incentives we laid out here. The premiums and discounts embedded in those markets are the clearest read we have on which economies the world believes are escaping the cage and which are not. That is where we are going next.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but Capital Flows does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of Capital Flows websites and systems including but not limited to data scraping, unauthorized entry into Capital Flows systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by Capital Flows and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to Capital Flows or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of Capital Flows.

Great piece, really keen on seeing how this all plays out in the endgame

Txs for the good content