Macro Regime Tracker: Macro views

Macro regime and risk assets qualified clearly

The Macro Regime Tracker offers a daily lens on how shifts in growth, inflation, and liquidity affect short-term risk and reward. Leveraging machine learning, AI, and cross-asset data, it identifies macro changes and their impact on market positioning.

Macro Regime Tracker Index:

Macro Regime Context

Macro Tear Sheets: Equities, Fixed Income, FX, Crypto, and Commodities

Macro Regime Dashboard: Excel spreadsheet for economic data and interest rates

Growth, Inflation, Fixed Income, Credit, and Equities Regime Tracker

AI and Machine Learning Strategies - Macro Regime and Positioning Premiums Strategies: S&P 500, 2-Year Interest Rates, Gold, and Bitcoin

Macro Regime Context:

All of the macro views have been laid out here:

Markets Are Forcing the Fed’s Hand—and the Curve Shows It

Markets Are Forcing the Fed’s Hand—and the Curve Shows It

I will be sharing more tomorrow. See updated systematic models below.

Main Developments In Macro

US Macro & Fed Policy

TRUMP: OUR FED RATE IS AT LEAST 3 POINTS TOO HIGH

TRUMP: WE SHOULD HAVE THE LOWEST INTEREST RATES

TRUMP: FED CHAIR SHOULD BE LOWERING RATES

TRUMP: CUT INTEREST RATES JEROME

TRUMP: NOW IS THE TIME TO CUT INTEREST RATES

HASSETT: TRUMP WILL DECIDE ON FED CHAIR

HASSETT MET WITH TRUMP AT LEAST TWICE IN JUNE ABOUT FED JOB: WSJ

NY FED: ONE-YEAR INFLATION EXPECTATIONS FALL TO 3.02% VS 3.2%

NY FED: 3Y INFLATION EXPECTATIONS UNCHANGED IN JUNE AT 3%

US MBA'S MORTGAGE APPLICATIONS INDEX ROSE 9.4% LAST WEEK

US FINAL MAY WHOLESALE INVENTORIES FALL 0.3%; EST. -0.3%

US MAY WHOLESALE SALES FALL 0.3% M/M; EST. +0.2%

Trade Policy & Tariffs

TRUMP TO IMPOSE 50% TARIFF ON GOODS FROM BRAZIL

TRUMP: TRADE RELATIONSHIP WITH BRAZIL FAR FROM RECIPROCAL

TRUMP: RELEASING BRAZIL TARIFF NUMBER TODAY OR TOMORROW MORNING

TRUMP: NO EXTENSIONS WILL BE GRANTED TO AUGUST 1 DEADLINE

TRUMP SAYS MONEY IS 'COMING IN' AUGUST 1 FROM TARIFFS

TRUMP: SUGGESTS UPDATE ON TRADE WITH 7 COUNTRIES WEDNESDAY

LUTNICK: TRUMP INTENDS TO GO TO 50% TARIFF ON COPPER

LUTNICK: COPPER TARIFF TO BE PUT IN PLACE LATER JULY OR AUG 1

LUTNICK: TRUMP LEFT FLEXIBILITY ON TARIFF RATES IN LETTERS

LUTNICK: TRUMP HAS EU OFFERS ON HIS DESK, DECIDING HOW TO PLAY

LUTNICK ON EU: THEY'VE MADE REAL OFFERS

LUTNICK: EXPECTING TO TALK TO CHINA IN AUGUST WITH BESSENT

LUTNICK: EXPECT 15-20 TRADE LETTERS TO GO OUT OVER NEXT 2 DAYS

CORRECT: BESSENT: EXPECTING $300B TARIFF INCOME BY END OF YEAR

NAVARRO: MARKETS UNDERSTAND TRADE LETTERS ARE NEGOTIATIONS

NAVARRO: LETTERS, DEALS COVER ALMOST 90% OF OUR TRADE DEFICIT

GOLDMAN SAYS US COPPER IMPORTS MAY RISE AHEAD OF IMPORT TARIFF

BESSENT IS SAID PLANNING TO VISIT JAPAN NEXT WEEK FOR EXPO

US, JAPAN AGREED TO CONTINUE VIGOROUS TALKS ON TARIFFS

JAPAN CONTINUES TO SEEK MUTUALLY BENEFICIAL AGREEMENT WITH US

AKAZAWA, BESSENT SPOKE FOR 30 MINUTES, JAPAN'S MOFA SAYS

US Geopolitical / Defense / Fiscal

TRUMP ADMIN HAS RESUMED SENDING SOME WEAPONS TO UKRAINE: AP

TRUMP: LOOKING AT UKRAINE, ADDITIONAL MUNITIONS

WHITE HOUSE WEIGHS GIVING UKRAINE ANOTHER PATRIOT SYSTEM: WSJ

TRUMP AND NETANYAHU EXPECTED TO MEET TODAY: AXIOS

TRUMP: VERY GOOD CHANCE OF GAZA AGREEMENT AS SOON AS THIS WEEK

SUPREME COURT LETS TRUMP PROCEED WITH SWEEPING WORKFORCE CUTS

DEPUTY TREASURY SECRETARY FAULKENDER SPEAKS ON BLOOMBERG TV

Macro Tear Sheets: Equities, Stock/Bond Correlation, Fixed Income, FX, Crypto, and Commodities

Macro Regime Dashboard: Excel spreadsheet for economic data, interest rates, and real estate.

Momentum and Mean Reversion Models: Equities, Commodities, Fixed Income, and Currencies

You can find the educational primer and video explanation of these models here: LINK

Here is a summary of all models and their directional strengths:

Growth, Inflation, Fixed Income, Credit, and Equities Regime Tracker

The Macro Regime Model offers a real-time view of growth, inflation, and yield curve dynamics, integrating these with credit market shifts, equity risk premiums, and positioning data. It connects upcoming catalysts to statistical drivers of asset prices, creating a unified framework that quantifies skew and clarifies risk-reward across asset classes.

Key Points To Set The Context:

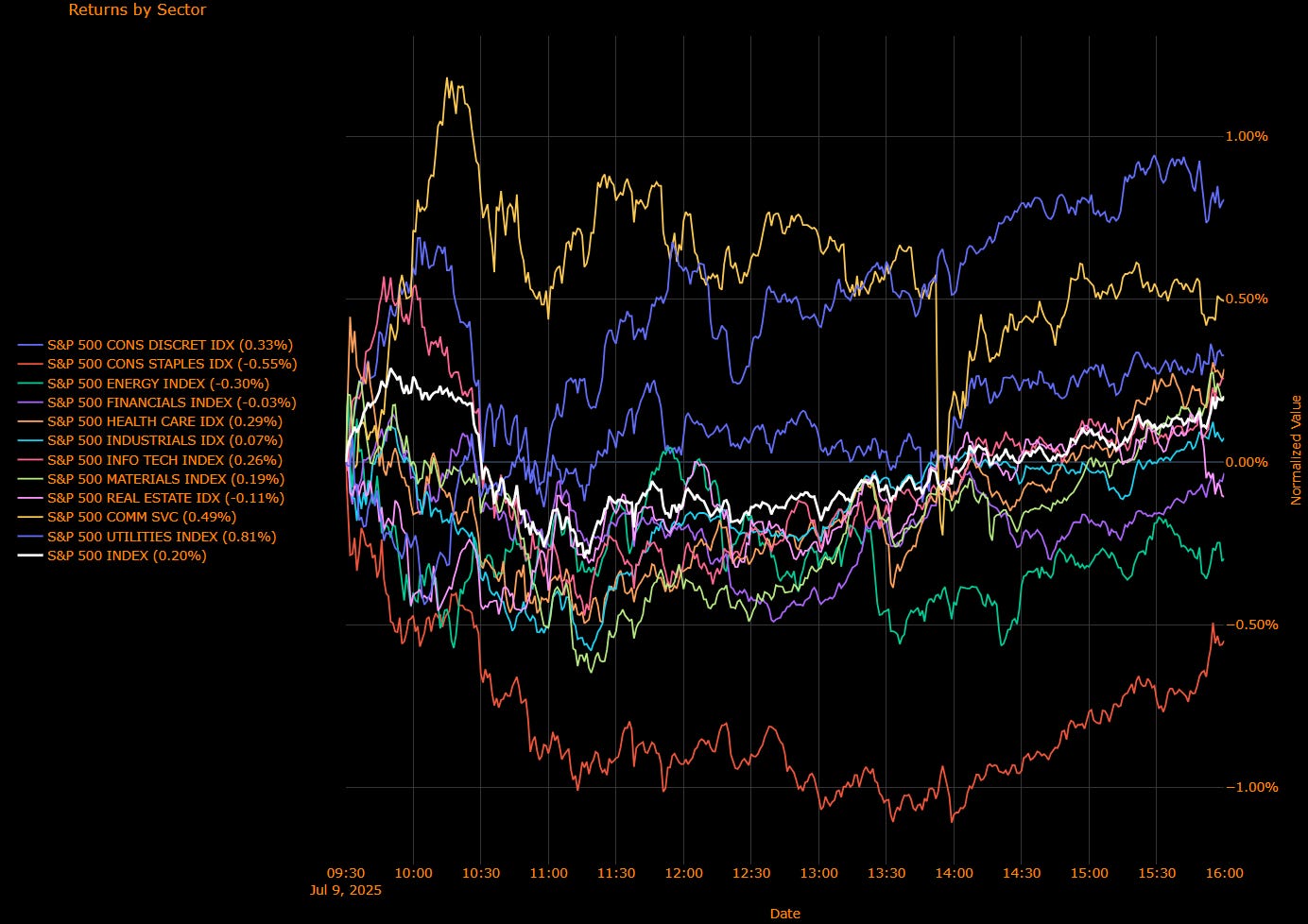

S&P 500 Rises 0.20% as Markets Refocus on Earnings Amid Tariff Fog

The S&P 500 climbed 0.20% Wednesday, regaining footing after Tuesday’s tariff-induced wobble, as risk appetite firmed into the upcoming earnings season. Sector leadership shifted decisively toward defensives, utilities, and communication services, while prior winners like energy and staples underperformed. With Nvidia briefly topping a $4 trillion market cap and bond yields easing modestly, equities pushed higher despite lingering policy uncertainty and President Trump’s renewed focus on tariff enforcement.

Sector Contribution Breakdown (Weighted Return to Index)

Information Technology (+0.09 pp) – Leading contributor again as big tech momentum persisted ahead of earnings. Nvidia’s surge and Apple resilience helped.

Communication Services (+0.05 pp) – Broad-based strength with platform and media stocks firming amid easing headline risk.

Health Care / Discretionary (+0.03 pp each) – Outperformance from pharma and select retail names lifted both sectors.

Utilities (+0.02 pp) – Yield compression supported interest-sensitive names; steady inflows into defensives.

Industrials (+0.01 pp), Materials (+0.00 pp) – Flat-to-mild gains on improving demand sentiment.

Staples / Real Estate / Financials (–0.00 to –0.03 pp) – Minor drags; consumer staples in particular weighed by margins and rate worries.

Energy (–0.01 pp) – Gave back some recent tariff-linked gains as copper cooled.

Sector Performance Breakdown (Unweighted Index Returns)

Utilities (+0.81%) – Best performing sector as lower yields supported high-dividend names.

Communication Services (+0.49%) – Continued bounce in platforms and streaming.

Consumer Discretionary (+0.33%), Health Care (+0.29%), Tech (+0.26%) – Rotation into beta-light and earnings-resilient pockets.

Materials (+0.19%), Industrials (+0.07%) – Underlying strength but no breakout.

Real Estate (–0.11%), Energy (–0.30%), Financials (–0.03%), Staples (–0.55%) – Dragged by yield stabilization and tariff discounting.

Macro Overlay: Calm Before Earnings, But Policy Noise Lingers

1. Tariff Risk Still Real, but Markets Decoupling (for Now)

Despite Trump reaffirming the August 1 tariff deadline and unveiling a 50% rate on Brazil, equity markets appear increasingly immune to trade headlines—at least temporarily. Tariff letters now cover 90% of the trade deficit, but expectations of negotiation progress remain, muting volatility.

2. Fed Minutes Highlight Inflation Divide

The FOMC minutes revealed a split over tariff-driven inflation risk, with most members concerned about longer-term price effects. Nonetheless, the market still sees two cuts this year, starting in September. Lower Treasury yields today supported equity multiples.

3. Earnings Season Now the Focus

With macro risks plateauing, attention turns to earnings. Mega-cap names continue to dominate flows. Nvidia's $4 trillion milestone highlights concentration, while breadth beneath the surface remains thin. Defensive positioning persists, but the “extreme greed” signal from the CNN Fear & Greed Index suggests optimism may be overextended.

Final Word: Tariff Headwinds Muted for Now, Earnings Take the Wheel

The S&P 500 is again leaning into tech, defensives, and utilities as the market shrugs off policy turbulence for now. Momentum is narrowing, but not breaking. With Nvidia and big tech powering the tape and Treasuries providing breathing room, equity bulls retain control ahead of earnings. That said, tariff risks and July CPI remain wildcards. Expect rotation, not retreat, until further catalysts emerge.

US IG Credit Wrap — Spreads Hold at 50.05 bp as Calm Masks Underlying Fragility

Current Spread: 50.05 bp | 5-Year Average: 62.80 bp

Investment-grade credit spreads tightened slightly to 50.05 basis points Wednesday, inching closer to post-pandemic tights despite a steady drumbeat of macro crosscurrents. While equities climbed on Nvidia’s $4 trillion milestone and receding long-end yields, credit markets were more restrained. The prevailing calm belies a landscape where tariff escalation, Fed uncertainty, and geopolitical frictions are quietly recalibrating risk premia beneath the surface.

Credit Context

< 60 bp: Duration-friendly, carry-positive zone for insurers, pensions, and liability-driven buyers.

60–70 bp: Macro noise threshold, where volatility or inflation threats prompt positioning cuts.

> 90 bp: Systemic stress unlikely unless global macro or geopolitical shocks return.

Macro Overlay: Calm Optics, Cautious Foundations

1. Spreads Compress as Risk Markets Reassert Bullish Bias

Spreads tightened ~1 bp despite ongoing policy and geopolitical overhangs. IG credit continues to behave like a carry trade — stable, liquid, and resilient — but cracks are beginning to emerge in peripheral positioning and liquidity depth. Bid-ask spreads in lower-rated segments have widened slightly, suggesting hesitation beneath the surface calm.

2. Trump’s Tariff Blitz Rolls On, Credit Watches the Edges

With over 90% of the US trade deficit now under active tariff negotiation, including this week’s 50% rate threat on Brazil and a 10% warning for India over BRICS participation, the market is shifting from binary reactions to slow-drip repricing. So far, credit is not treating this as systemic — but longer-term corporate margin risks are being repriced, especially in auto, retail, and semiconductors.

3. Fed Split Widens as Tariff Inflation Enters the Room

FOMC minutes revealed a growing divide over how tariffs might impact inflation trajectories. While some policymakers see one-off effects, most fear stickier pass-throughs. The implication: the September cut remains base case, but anything resembling a CPI surprise next week could delay or dilute the easing cycle. Credit is treading carefully — flat curves and dovish expectations are built into pricing.

4. Treasury Rally Offers Temporary Relief to Credit Duration

Wednesday’s bond auction brought a reprieve, with 10-year yields falling to 4.34%. While positive for IG carry math, this was more a tactical pause than a structural reversal. The 30-year remains elevated, and curve steepening pressures haven’t gone away — especially if energy prices or tariffs push inflation expectations higher again.

Final Word: Steady, Not Secure

At 50.05 bp, US IG spreads are hovering just above their lowest levels since 2018. But the risk-reward has subtly changed: tariff timelines are real, the Fed is increasingly split, and high-grade supply is expected to return post-earnings blackout. With macro volatility now a background hum rather than a shock event, credit is holding.

Mag7 Model:

See the intro published for how to use the Mag7 models here: Link

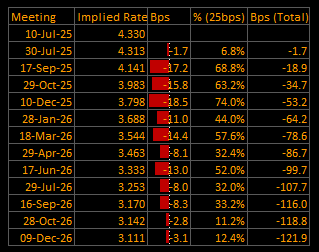

Short-End Rates Wrap: Easing Path Firms at –121.9 bp as Market Brushes Off Trade Rhetoric, Awaits CPI Signal

Cumulative Implied Easing: –121.9 bp | Terminal Still Anchored Near 3.11%

The OIS curve leaned more dovish Thursday, with markets now pricing in –121.9 basis points of rate cuts through December 2026 — a modest shift from –116.4 bp a day earlier. The move reflects stronger conviction in the post-September glidepath, despite persistent trade headlines and Powell’s steady tone. The Fed’s inflation hesitance remains, but markets are not waiting for formal guidance: the curve is increasingly confident that the easing cycle will proceed — if gradually.

OIS-Implied Rate Path

Front-End Meetings:

10-Jul-25: 4.330% → Cut fully priced out

30-Jul-25: 4.313% (–1.7 bp) → ~7% probability → July remains sidelined

17-Sep-25: 4.141% (–7.2 bp) → ~69% probability → September firming as first cut

29-Oct-25: 3.983% (–5.8 bp) → ~63% probability → Additional follow-through priced

2025 Year-End Outlook:

10-Dec-25: 3.798% → –53.2 bp total easing → Two cuts priced in with moderate conviction

Cycle Terminal:

09-Dec-26: 3.111% → –121.9 bp total easing → Terminal below 3.15%, dovish trend restored

Macro Overlay: Trade Noise, Policy Patience, CPI in Focus

1. Market Digests Tariff Rhetoric Without Repricing Core Path

Despite a barrage of tariff letters — including a newly announced 50% levy on Brazil — markets remain anchored to macro stability. Participants view Trump’s trade blitz as largely strategic posturing with inflation implications too murky to reprice the Fed path materially.

→ The tariff regime may matter later, but markets want to see CPI before reacting.

2. Powell Holds the Line as Fed Split on Inflation Risk Emerges

FOMC minutes revealed a growing divide on the inflation impact of tariffs. While “most” policymakers worry about persistence, others see tariffs as one-off price bumps. Powell remains in the data-dependent camp. Fed Funds futures are now fully pricing in a September cut and leaning toward a second in December.

→ The market is increasingly front-running the Fed’s caution.

3. Soft Underlying Labor and Solid Treasury Demand Offer Cover

Despite tight jobless claims and a resilient NFP headline, wage growth, participation, and private hiring data continue to flag. Meanwhile, a strong 10Y auction signaled underlying demand for duration, giving further comfort to the market’s dovish view.

→ Traders are betting the Fed can ease without stoking volatility.

Final Word: Patience Persists, But the Market Leans Ahead

With –121.9 bp of cuts now priced through 2026 and September seen as a near lock, the easing bias has resumed despite tariff rhetoric. Investors appear to be increasingly discounting trade shocks and inflation worries as short-term noise. All eyes now turn to July 15 CPI — the last major input before Powell speaks on July 17.

Unless CPI flares or trade rhetoric escalates into action, the market seems set on a lower-for-longer trajectory — and the Fed may need to catch up.

Tactical Portfolio

Morning Trade(s) and Market thread

Keep reading with a 7-day free trial

Subscribe to Capital Flows to keep reading this post and get 7 days of free access to the full post archives.