Macro Regime Tracker: The Fed is in a corner

Macro regime and risk assets qualified clearly

The Macro Regime Tracker offers a daily lens on how shifts in growth, inflation, and liquidity affect short-term risk and reward. Leveraging machine learning, AI, and cross-asset data, it identifies macro changes and their impact on market positioning.

Macro Regime Tracker Index:

Macro Regime Context

Macro Tear Sheets: Equities, Fixed Income, FX, Crypto, and Commodities

Macro Regime Dashboard: Excel spreadsheet for economic data and interest rates

Growth, Inflation, Fixed Income, Credit, and Equities Regime Tracker

AI and Machine Learning Strategies - Macro Regime and Positioning Premiums Strategies: S&P 500, 2-Year Interest Rates, Gold, and Bitcoin

Macro Regime Context:

See the market views and video I laid out in this report explaining how the Fed is being cornered with inflation risk:

Markets Are Forcing the Fed’s Hand—and the Curve Shows It

Markets Are Forcing the Fed’s Hand—and the Curve Shows It

All of the systematic models are laid out below.

Main Developments In Macro

US Monetary Policy & Inflation Outlook

TRUMP SAYS 'NOW IS THE TIME' TO CUT INTEREST RATES

TRUMP: CUT INTEREST RATES JEROME

SUPREME COURT LETS TRUMP PROCEED WITH SWEEPING WORKFORCE CUTS

NY FED: ONE-YEAR INFLATION EXPECTATIONS FALL TO 3.02% VS 3.2%

NY FED: 3Y INFLATION EXPECTATIONS UNCHANGED IN JUNE AT 3%

COUNCIL OF ECONOMIC ADVISERS CHAIR MIRAN SPEAKS ON FOX NEWS

MIRAN: WE COULD SEE MORE TRADE DEALS BY THE END OF THE WEEK

Trade & Tariffs

WHITE HOUSE TRADE COUNSELOR NAVARRO SPEAKS ON FOX BUSINESS

NAVARRO: LETTERS, DEALS COVER ALMOST 90% OF OUR TRADE DEFICIT

COMMERCE SECRETARY HOWARD LUTNICK ENDS REMARKS ON CNBC

LUTNICK: IF COUNTRIES ARE GOOD TO US, THEY MAY GET ANOTHER RATE

LUTNICK: TRUMP LEFT FLEXIBILITY ON TARIFF RATES IN LETTERS

LUTNICK: TRUMP HAS EU OFFERS ON HIS DESK, DECIDING HOW TO PLAY

LUTNICK ON EU: THEY'VE MADE REAL OFFERS

LUTNICK: EXPECTING TO TALK TO CHINA IN AUGUST WITH BESSENT

LUTNICK: STUDIES ON PHARMA, SEMICONDUCTORS DONE BY END OF MONTH

LUTNICK: COPPER TARIFF TO BE PUT IN PLACE LATER JULY OR AUG 1

LUTNICK: THE IDEA IS TO BRING COPPER PRODUCTION HOME

LUTNICK: TRUMP INTENDS TO GO TO 50% TARIFF ON COPPER

LUTNICK: EXPECT 15-20 TRADE LETTERS TO GO OUT OVER NEXT 2 DAYS

TRUMP: NO EXTENSIONS WILL BE GRANTED TO AUGUST 1 DEADLINE

TRUMP SAYS MONEY IS 'COMING IN' AUGUST 1 FROM TARIFFS

Japan-US Trade Talks

AKAZAWA, BESSENT SPOKE FOR 30 MINUTES, JAPAN'S MOFA SAYS

JAPAN CONTINUES TO SEEK MUTUALLY BENEFICIAL AGREEMENT WITH US

US, JAPAN AGREED TO CONTINUE VIGOROUS TALKS ON TARIFFS

JAPAN'S TRADE NEGOTIATOR AKAZAWA HAD PHONE CALL WITH BESSENT

AKAZAWA: SEEING MORE DOWNSIDE RISK TO ECONOMY FROM US TARIFFS

AKAZAWA: NO INTENTION OF SACRIFICING AGRICULTURE IN TALKS

AKAZAWA: CAN'T REACH AGREEMENT WITHOUT AGREEMENT ON CAR SECTOR

AKAZAWA: WON'T COMPROMISE ON ISSUES OF KEY NATIONAL INTEREST

AKAZAWA: TRYING TO REACH AGREEMENT WITH US OVER BROAD ISSUES

AKAZAWA: AGREED WITH LUTNICK TO CONTINUE VIGOROUS NEGOTIATIONS

AKAZAWA: SEE PROGRESS IN TRADE TALKS WITH US

AKAZAWA: FEEL JAPAN, US BUILDING TRUST ON TRADE TALKS

AKAZAWA: JAPAN HAS AVOIDED EASY COMPROMISES

Macro Tear Sheets: Equities, Stock/Bond Correlation, Fixed Income, FX, Crypto, and Commodities

Macro Regime Dashboard: Excel spreadsheet for economic data, interest rates, and real estate.

Momentum and Mean Reversion Models: Equities, Commodities, Fixed Income, and Currencies

You can find the educational primer and video explanation of these models here: LINK

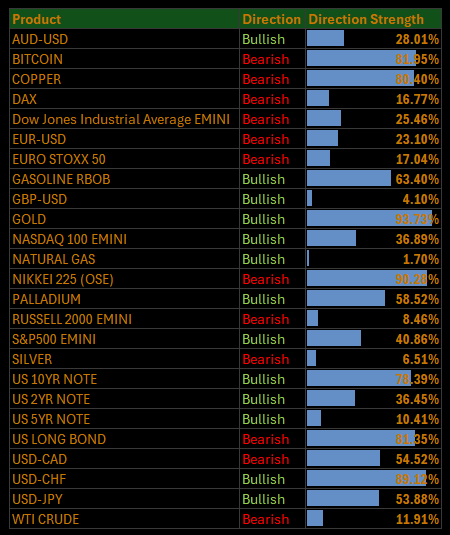

Here is a summary of all models and their directional strengths:

Growth, Inflation, Fixed Income, Credit, and Equities Regime Tracker

The Macro Regime Model offers a real-time view of growth, inflation, and yield curve dynamics, integrating these with credit market shifts, equity risk premiums, and positioning data. It connects upcoming catalysts to statistical drivers of asset prices, creating a unified framework that quantifies skew and clarifies risk-reward across asset classes.

Key Points To Set The Context:

S&P 500 Slips 0.12% as Tariff Jitters Cap Momentum, Energy Rallies on Copper Shock

The S&P 500 inched 0.12% lower Tuesday as investors digested intensifying tariff risk and rising long-end yields. While most sectors traded softly, Energy and Health Care outperformed, buoyed by Trump’s copper tariff push and renewed bid for defensive earnings. Markets appear to be entering a holding pattern near all-time highs ahead of July CPI, with fresh trade headlines keeping volatility surfaces elevated and participation narrow.

Sector Contribution Breakdown (Weighted Return to Index)

Financials (–0.10 pp) – Largest drag as rising long-end yields pressured banks amid limited risk-on appetite.

Consumer Discretionary (–0.08 pp) – Softness in retail and luxury goods on trade concerns and Prime Day margin compression.

Communication Services (–0.07 pp) – Platform names faded as ad-tech paused and media stocks faced tariff-linked uncertainty.

Staples / Utilities (–0.02 pp to –0.01 pp) – Light defensive pullback; rate moves offset fundamental support.

Energy (+0.08 pp) – Outperformed on copper tariff tailwind and broad materials strength.

Health Care (+0.06 pp) – Continued rotation into defensives; pharma headlines around tariff exemptions provided support.

Tech, Materials, Real Estate (flat to +0.01 pp) – Muted flows despite underlying resilience.

Sector Performance Breakdown (Unweighted Index Returns)

Energy (+2.69%) – Strongest gainer on the day, lifted by Freeport-McMoRan and materials names as copper surged.

Health Care (+0.66%) – Pharma led on speculation of delayed tariff application.

Materials (+0.45%), Real Estate (+0.35%) – Benefited from rate stabilization and commodity strength.

Tech (+0.04%), Industrials (+0.04%) – Flat-to-positive as global growth fears were balanced by firm macro data.

Discretionary (–0.75%), Financials (–0.73%) – Heaviest laggards as trade and yield fears weighed.

Comm Services (–0.77%), Staples (–0.44%), Utilities (–0.23%) – Broad underperformance across consumer- and yield-sensitive plays.

Macro Overlay: Tariff Risk Lingers, But CPI Is the Decider

Tariff Deadline Unmoved

Trump reiterated that the August 1 tariff start date is “firm but not 100%,” while his team continues to negotiate with over a dozen countries. Despite some late-stage deal optimism, uncertainty persists. Letters this week covered 90% of the US trade deficit, adding asymmetric headline risk.Yields Grind Higher

Treasuries weakened again, with the 10-year yield rising to 4.41% and the 30-year testing 5% for the first time since early May. Soft demand in front-end auctions and global curve shifts (notably in JGBs and bunds) contributed to pressure.Markets Hold Near Highs As Internals Fade

S&P breadth narrowed further, and the Magnificent 7 index edged down. Credit spreads remain well-anchored and vol curves are elevated but orderly. For now, equities are consolidating rather than capitulating.CPI Next as Inflation Refocuses Fed Path

The July 15 inflation print is the next major macro catalyst. Market pricing still leans toward a September cut, but tariff passthrough and any upside CPI surprise could challenge the path.

Tariff Clock Ticking, Market Pauses at the Peak

The S&P 500 is stalling just below its highs as policy risk competes with macro momentum. While copper, energy, and defensives are providing selective support, the broader market remains hostage to the outcome of trade negotiations and inflation data. Until CPI gives clarity, expect sideways grind, sector rotation, and increasing asymmetry in equity leadership.

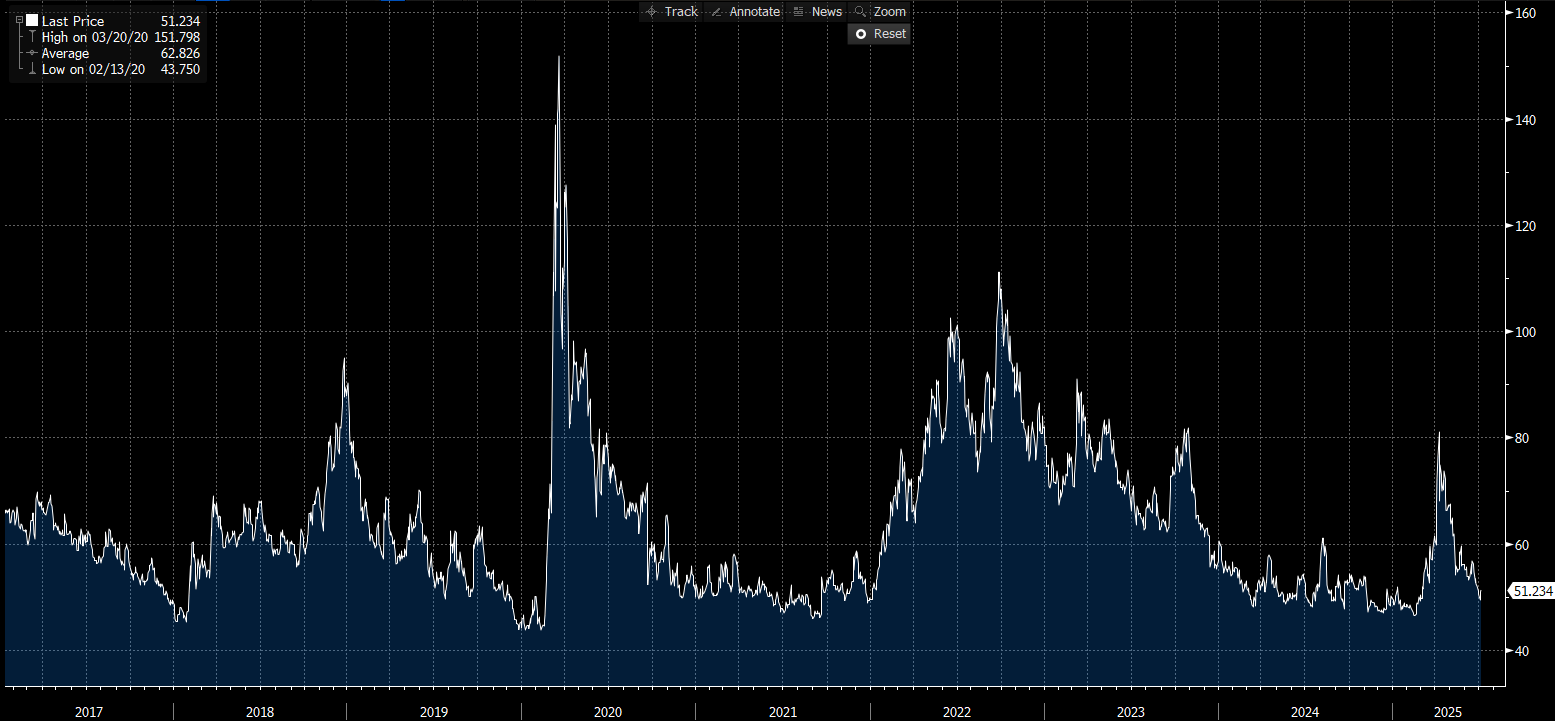

US IG Credit Wrap: Spreads Edge to 51.23 bp as Trade Countdown Saps Risk Conviction

Current Spread: 51.23 bp | 5-Year Average: 62.83 bp

Investment-grade credit spreads were little changed Tuesday, nudging wider by less than half a basis point to 51.23 bp. While still holding near post-pandemic tights, the market’s tone was noticeably less certain. A firm dollar, soft demand at Treasury auctions, and continued tariff overhang capped fresh inflows into high-grade credit, even as carry and stability remain broadly supportive.

Credit Context

< 60 bp: Duration-friendly, carry-positive zone for insurers, pensions, and liability-driven buyers.

60–70 bp: Macro noise threshold, where volatility or inflation threats prompt positioning cuts.

> 90 bp: Systemic stress unlikely unless global macro or geopolitical shocks return.

Macro Overlay: Stability Holds, But Confidence Is Uneven

1. Trump’s Tariff Clock Keeps Ticking

President Trump reiterated that the August 1 tariff implementation is "firm but not 100% firm," with no intention to grant further delays. With 25%–40% levies spanning over a dozen trade partners, and sectoral actions pending on autos, chips, and pharma, the window for negotiation remains but risk premia have quietly begun to rise across risk assets.

Credit remains resilient but directional conviction is lacking as traders gauge whether the tariff reprieve strategy turns into prolonged volatility.

2. Treasuries Bear-Steepen Again as Long-End Demand Falters

Yields rose across the curve, with the 10Y up to 4.41% and the 30Y nearing 5%. Soft demand at Tuesday’s 3-year note auction and spillover from JGB and bund weakness reinforced steepening pressure. That kept rate-sensitive IG names in check, particularly in housing, autos, and utilities.

Spread Floor Holds, But Market Is Tense

At 51.23 bp, IG spreads are remarkably stable in historical context but not without friction. The tariff regime is now functioning as a volatility overhang: staggered threats, sector-specific escalation, and global trade frictions are raising headline sensitivity. The credit market hasn’t broken—but it’s no longer fading every shock either.

Mag7 Model:

See the intro published for how to use the Mag7 models here: Link

Short-End Rates Wrap: Fed Path Steadies at –116.4 bp as Market Weighs Tariff Deadline, Labor Cools

Cumulative Implied Easing: –116.4 bp | September Cut Still Anchored

The OIS-implied path for Fed policy remained firmly dovish Wednesday, with markets pricing –116.4 basis points of total cuts by December 2026. That’s a marginal rebound from the prior day’s –118.6 bp, reflecting slightly firmer back-end expectations. While July is still fully priced out, September remains the favored pivot. Market conviction in the lower terminal endures, even as trade tensions mount and real rates firm.

OIS-Implied Rate Path

Front-End Meetings:

09-Jul-25: 4.330% → No live cut risk

30-Jul-25: 4.318% (–1.2 bp) → ~5% probability → Off the table barring a shock

17-Sep-25: 4.156% (–6.2 bp) → ~65% probability → Remains the base case

29-Oct-25: 4.012% (–14.4 bp) → ~58% probability → Still supportive of a shallow glide

2025 Year-End Outlook:

10-Dec-25: 3.837% → –49.3 bp total easing → Two cuts priced in with moderate confidence

Cycle Terminal:

09-Dec-26: 3.166% → –116.4 bp total → Terminal pricing still below 3.20%, despite inflation and tariffs

Macro Overlay: Policy Patience, Trade Deadlines, Labor Drift

1. Tariff Countdown In Focus, Market Not Blinking Yet

With Trump reaffirming his August 1 deadline for new reciprocal tariffs, markets continue to price risk conservatively not reactively. Rates remain anchored as investors treat the policy as a "negotiation lever" rather than a baseline inflation driver.

Still, some creep in back-end implied rates suggests the market is hedging against prolonged policy drift and soft Fed credibility.

2. Labor Data: Resilient Topline, Weak Guts

Despite an upside NFP print last week (+147k), internals continue to deteriorate:

Private payrolls: +74k → slowest since Oct

Participation: 62.4% → second monthly drop

Average workweek: 34.2 hours

Wage growth: +0.2% m/m → slowing trend

The labor market continues to offer the Fed cover for optionality supportive of cuts, but not forcing urgency.

3. Powell Stays Cautious, But Political Pressure Builds

Chair Powell’s messaging remains consistent: caution, data dependence, and tariff uncertainty. Meanwhile, former Fed Governor Kevin Warsh called for urgent cuts and criticized institutional inertia, adding political noise to the otherwise muted policy debate.

Markets aren’t buying rate hikes or a hawkish reversal but September now needs confirmation through inflation prints and trade headlines.

Path Holds Steady, but Tariff Deadline Looms

At –116.4 bp, the easing trajectory is broadly unchanged lower-for-longer still rules. But as the August 1 tariff clock ticks louder, volatility is shifting from the front-end to the tail. September remains the fulcrum, and unless CPI surprises hotter or trade blows up, the market has no incentive to price anything more aggressive.

What Matters Next:

CPI (Jul 15): Services disinflation or reacceleration could tip the odds

Tariff Deadline (Aug 1): Policy risk becoming inflation risk?

Fedspeak / Powell (Jul 17): Market wants consistency, not new guidance

Tactical Portfolio

Morning Trade(s) and Market thread

Keep reading with a 7-day free trial

Subscribe to Capital Flows to keep reading this post and get 7 days of free access to the full post archives.