Macro Regime Tracker: The RALLY

Macro regime and risk assets qualified clear

The Macro Regime Tracker offers a daily lens on how shifts in growth, inflation, and liquidity affect short-term risk and reward. Leveraging machine learning, AI, and cross-asset data, it identifies macro changes and their impact on market positioning.

Macro Regime Tracker Index:

We are seeing flows move in lockstep with the bullish ES trade I laid out for paid subscribers here:

And fading the NQ move on NVDA earnings here:

We are entering a period of time where understanding the inflation playbook will be the differentiator between success and failure. The entire playbook is laid out here:

Inflation Isn’t Transitory — It’s the New Macro Order (FREE INFLATION CYCLE PLAYBOOK)

Inflation Isn’t Transitory — It’s the New Macro Order

The livestream I did with Skigod today can be found here, and I would encourage you to check out his work: https://www.skool.com/bitcoinandbuildings

As always, the systematic models and strategies can be found below.

Main Developments In Macro

Fed governance & policy

*WHITE HOUSE: REMOVAL FOR CAUSE IMPROVES FED'S ACCOUNTABILITY

*WHITE HOUSE: LISA COOK 'CREDIBLY ACCUSED OF LYING'

*WHITE HOUSE: TRUMP FOUND THERE WAS CAUSE TO REMOVE LISA COOK

*WHITE HOUSE ON COOK: TRUMP EXERCISED HIS LAWFUL AUTHORITY

*LISA COOK SUES TRUMP OVER HIS MOVE TO OUST HER FROM FED BOARD

*SENATE BANKING COMMITTEE EXPECTED TO HOLD HEARING NEXT WEEK

*TRUMP PICK MIRAN IS ON TRACK FOR CONFIRMATION BEFORE FED MEETS

*ECB'S REHN: TESTING FED INDEPENDENCE CAN HAVE SIGNIFICANT RISKS

Trade, tariffs & geopolitics (US-facing)

*EU: PROPOSALS TO ENSURE RETROACTIVE US TARIFF RELIEF ON EU CARS

*EU PUTS FORWARD TWO PROPOSALS AS PART OF EU-US TRADE PACT

*EU PRESENTS LOWER US TARIFFS PROPOSALS TO UNLOCK 15% AUTO DUTY

*US OPEN TO DIRECT DIALOG WITH IRAN

*US WELCOMES EUROPEAN PLAN TO IMPOSE IRAN SNAPBACK SANCTIONS

*ZUCKERBERG LOBBIED TRUMP ON DIGITAL TAXES BEFORE TARIFF THREAT

*ZUCKERBERG MET WITH TRUMP AT WHITE HOUSE LAST WEEK

*GRAHAM IMPLIES US SHOULD IMPOSE TARIFFS ON NORWAY

*GRAHAM CRITICIZES NORWEGIAN FUND FOR PULLING CATERPILLAR STAKE

*SENATOR GRAHAM THREATENS NORWAY'S SOVEREIGN WEALTH FUND

Macro Tear Sheets: Equities, Stock/Bond Correlation, Fixed Income, FX, Crypto, and Commodities

Macro Regime Dashboard: Excel spreadsheet for economic data, interest rates, and real estate.

Momentum and Mean Reversion Models: Equities, Commodities, Fixed Income, and Currencies

You can find the educational primer and video explanation of these models here: LINK

Growth, Inflation, Fixed Income, Credit, and Equities Regime Tracker

The Macro Regime Model offers a real-time view of growth, inflation, and yield curve dynamics, integrating these with credit market shifts, equity risk premiums, and positioning data. It connects upcoming catalysts to statistical drivers of asset prices, creating a unified framework that quantifies skew and clarifies risk-reward across asset classes.

Key Points To Set The Context:

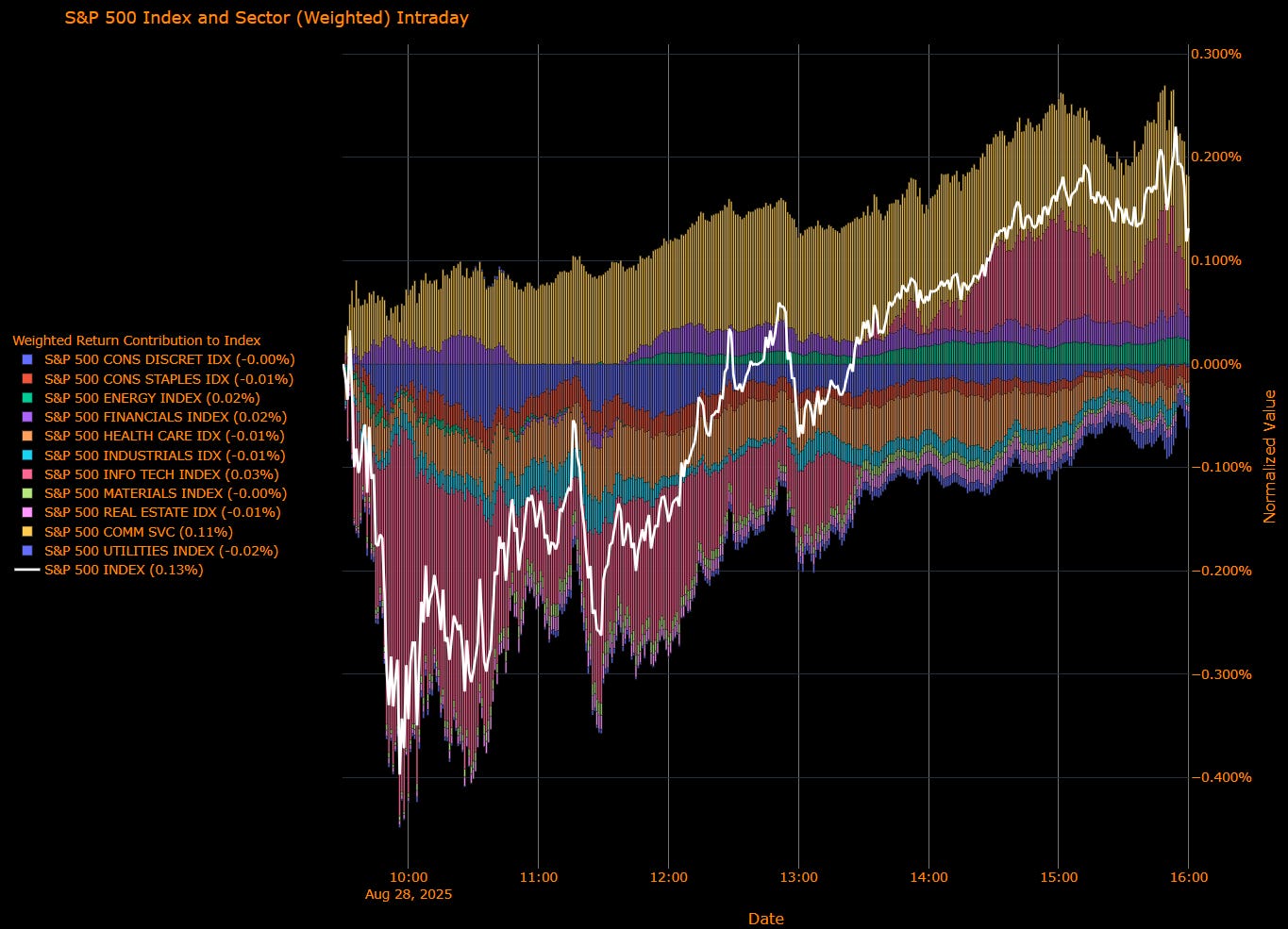

US Market Wrap: Narrow Green Day, Comm Services Does the Heavy Lifting; Curve Flattens Into PCE (S&P +0.13%)

A tentative cash session drifted higher into the close, with gains concentrated in mega-cap Communication Services while most defensives sagged. Macro tone was “good growth, waiting on inflation”: 2Q GDP was revised up to 3.3% SAAR with core PCE at 2.5% (q/q saar), jobless claims held steady at 229k, and traders stayed focused on Friday’s core PCE print. Rates flattened (2-yr +2 bp to ~3.63%, 10-yr −3 bp to ~4.21%), the dollar slipped, WTI and gold inched higher. Dell’s upbeat guide helped the AI-infrastructure story; Nvidia chatter stayed in the background.

Sector Contribution (weighted to index move)

Offsets: Communication Services (+0.11%), Information Technology (+0.03%), Energy (+0.02%), Financials (+0.02%).

Detractors/flat: Utilities (−0.02%), Real Estate (−0.01%), Consumer Staples (−0.01%), Industrials (−0.01%), Health Care (−0.01%), Consumer Discretionary (−0.00%), Materials (−0.00%).

Index: S&P 500 (+0.13%).

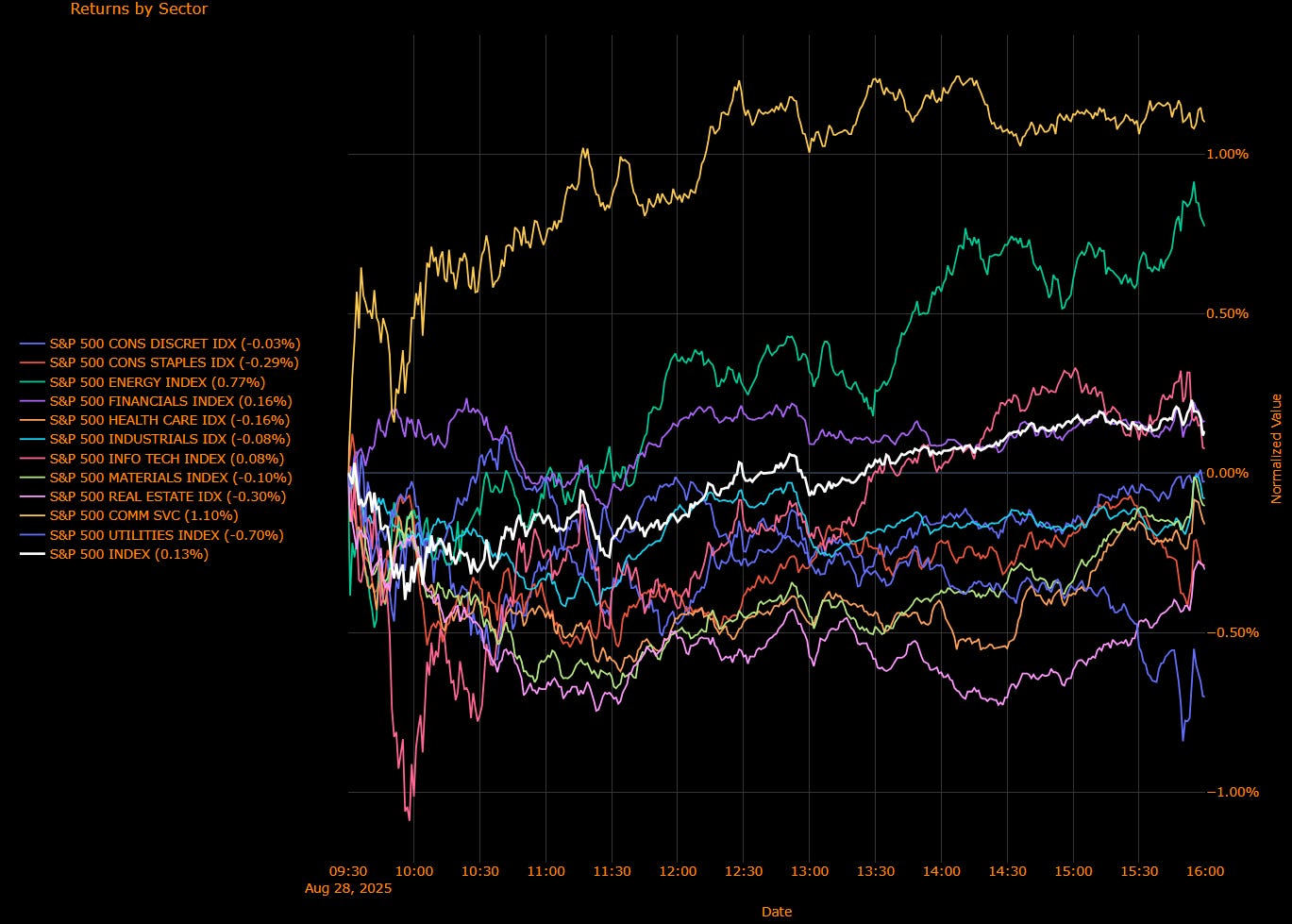

Sector Performance (unweighted breadth)

Leaders: Communication Services (+1.10%), Energy (+0.77%), Financials (+0.16%), Information Technology (+0.08%).

Laggards: Utilities (−0.70%), Real Estate (−0.30%), Consumer Staples (−0.29%), Materials (−0.10%), Industrials (−0.08%), Health Care (−0.16%), Consumer Discretionary (−0.03%).

Index: S&P 500 (+0.13%).

Macro Overlay

Growth vs inflation: Upward GDP revision (3.3% SAAR) and steady core PCE (2.5% q/q saar) keep the “resilient growth, disinflation not done” narrative intact ahead of July core PCE (consensus ~2.9% y/y). Claims at 229k still signal a cooling-but-not-cracking labor market.

Rates & auction color: The curve flattened with front-end yields a touch higher and 10s lower. The 7-yr auction tailed modestly (~3.925% vs 3.922% WI) with softer bid/cover (2.49 vs 2.79 prior) but heavy indirect take-up orderly, not exuberant.

Liquidity: Money-market fund balances printed a fresh record (

($4.19B), plenty of dry powder as policy approaches a pivot.Micro tells: Comm Services’ outsized contribution underscores mega-cap leadership (META/GOOGL complex), while Utilities/REITs lagged with long rates slipping, more “risk leadership” than “duration bid.” Dell’s stronger AI server outlook supports the capex cycle even as NVDA’s guide scrutiny lingers.

What's next….

A September 25 bp cut remains the market anchor; today’s flattening says “watch the front end” into PCE. In-line/softer core PCE likely extends the grind higher with leadership in AI-adjacent and comms; a hot print risks a brief de-risking and deeper flattening. Near-term pivots: Friday core PCE, 5s30s behavior into month/quarter-end, and whether Comm Services’ concentrated lift can broaden without defensives rolling over.

US IG Credit Wrap: Low-50s Steady; Curve Flattens Into PCE, Growth Fine (S&P +0.3%, USD −0.3%)

IG OAS: 50.12 bp • 5-yr avg: 62.59 bp (12.5 bp inside) • Cycle low: 43.75 bp (6.4 bp off tights) • COVID high: 151.80 bp (~101.7 bp tighter)

Spreads were essentially unchanged in a calm “rates-do-the-moving” tape: IG OAS hugged the low-50s as the curve flattened (2-yr +2 bp to ~3.63%, 10-yr −3 bp to ~4.21%). Cash equities were modestly higher, dollar softer, and haven metals/energy edged up supportive backdrop for carry over beta.

Credit Context

< 60 bp: Duration-friendly, carry-positive zone for insurers, pensions, and liability-driven buyers.

60–70 bp: Macro noise threshold, where volatility or inflation threats prompt positioning cuts.

> 90 bp: Systemic stress unlikely unless global macro or geopolitical shocks return.

Macro Overlay for IG

Growth: 2Q GDP revised up to 3.3% SAAR with final sales ~1.9%; claims 229k—cooling, not cracking.

Inflation: Core PCE (2Q) steady at 2.5% q/q saar; July core PCE ~2.9% y/y is the pivot for the front end.

Rates & auctions: The 7-yr tailed ~0.3 bp (3.925% vs 3.922% WI), bid/cover 2.49 with heavy indirects—orderly, not exuberant.

Liquidity: MMF balances at a record ~$7.21T; discount-window use eased to $4.19B—ample dry powder while cuts are priced by Oct (≈20 bp for Sep).

Micro tells: AI-capex tone constructive (Dell upbeat) even as NVDA guide debate lingers; not a spread event.

What to Watch

Friday core PCE vs ~2.9% y/y consensus; a mild miss likely extends the “carry grind.”

Curve behavior (5s30s/2s10s) into month/quarter-end—any re-steepening from politics/term premium matters more to returns than a 1–2 bp wiggle in OAS.

AI-hardware guides and capex signals (servers, power) for TMT/IG supply cadence.

Next week’s payrolls for confirmation of “cooling-but-resilient.”

Mag7 Model:

See the intro published for how to use the Mag7 models here: Link

Capital Flows Interest Rate Sensitivity Model:

All of the interest rate sensitivity models are now reserved exclusively for paid subscribers. If you would like to do a free trial, you can with this LINK.

Launch video for these models is here: LINK

Keep reading with a 7-day free trial

Subscribe to Capital Flows to keep reading this post and get 7 days of free access to the full post archives.