I strongly believe we are seeing a convergence in the flows of capital across every level of markets with an even greater concentration than I originally anticipated. The net result is a very high probability of having a gamma squeeze in my largest position, PURR, similar to the gamma squeeze in GameStop during the 2021 melt-up.

Let me lay out each factor and then show you how they all STACK on top of each other to create an asymmetrical outcome that people are not aware of right now.

The Big Picture Context:

I have been explaining my thesis behind PURR 0.00%↑ for over 6 months now. I started explaining it to paid subscribers just after the merger, when we were trading below $3.50:

We are now up 217% from the lows with A TON of momentum in our sails.

TWO things have changed since I originally laid out this thesis:

The credit cycle has caused a significant injection of liquidity and credit, which is causing an everything rally.

I have documented my views on the credit cycle extensively, explaining how the inflation risk has actually accelerated the fall in real rates, which has pushed more capital out the risk curve. Read these reports on this:

The microstructure of the market around PURR 0.00%↑ has dramatically changed over the last 2 weeks, which is creating a very high probability of a gamma squeeze in PURR 0.00%↑.

I have explained the entire PURR 0.00%↑ thesis since the beginning in the following reports (in order of date published):

They sold everyone a lie and then became the new establishment (Jan 16, 2026)

My Large Macro/Crypto Bet: Updated Analysis, Fair Value Indicator & Full Report (Feb 11, 2026)

If you want to review my entire thesis on ORCL, see here:

This is my next big bet (Oracle Risk reward) (see this if you want my levels and call strike for ORCL)

Oracle Model: LINK

AI Playbook, Larry Ellison’s Big Bet With ORCL, and New Stock Models

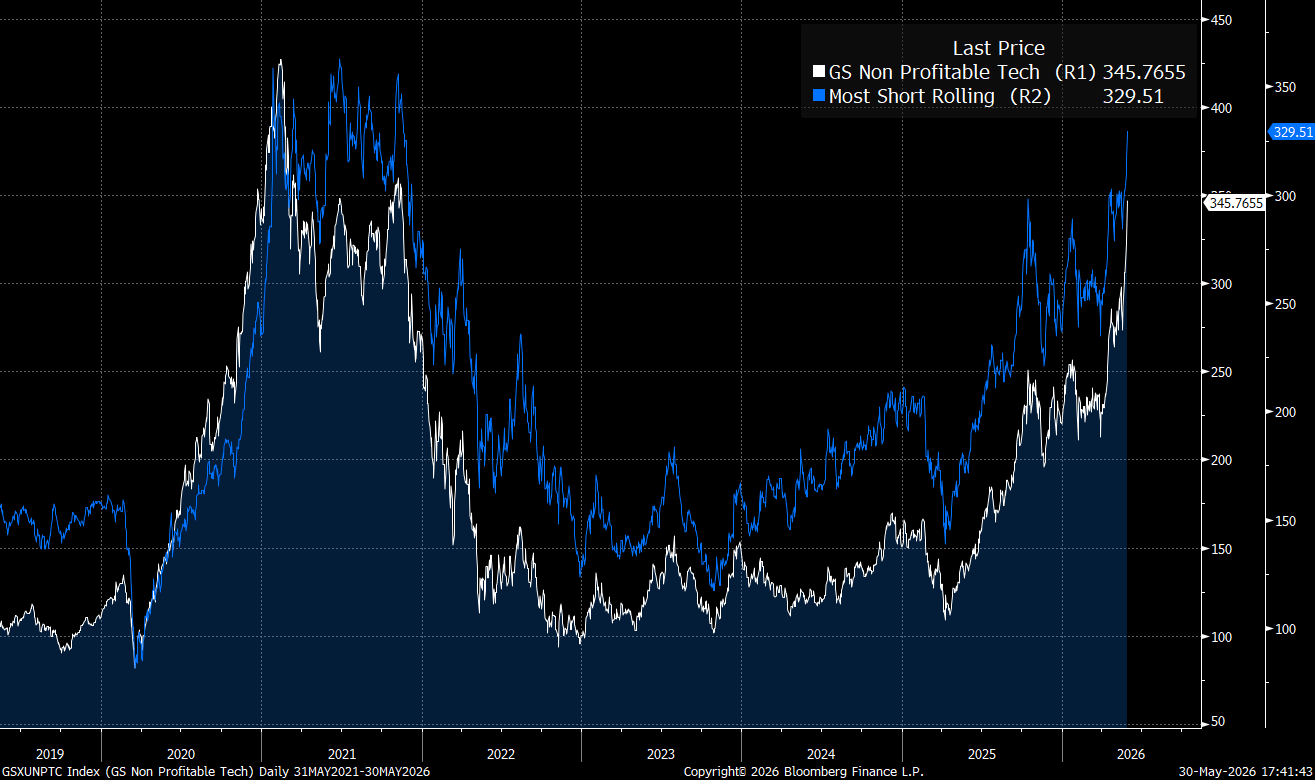

Over the last 7 trading days, it has become very clear that we have entered an “everything rally” similar to 2021. This is in direct alignment with the credit cycle thesis I have laid out. Citrini had a great comment on this as well:

As I have stated over and OVER, you always want to be long the right tail during a credit cycle melt-up. This is when the largest positive returns take place in markets.

We are already seeing shorts get squeezed in a massive way as bearish bets get unwound and traders are forced to buy low-quality companies due to the surplus of money in the system.

The Change in PURR:

Over the two weeks, the positioning in the market has changed dramatically in both how sector flows are changing, how capital is moving out the risk curve, and how institutional players are about to be forced to chase the buying pressure in $PURR.

Fundamentally, when we have an increase in the amount of capital in the system, traders are FORCED to take additional bets, or else they underperform the benchmark. This is also true for the underlying economy, with what many people label as “retail.” When incomes accelerate in the economy, more money can go into brokerage accounts to bet on high-beta names. This is not a bug of the system; it is a very important feature!

As this is taking place, Hyperliquid is the winner-take-all project in the crypto and TradFi space. I was laying out the Hyperliquid and PURR thesis when we were at the low 20s, and then another risk-reward set up after flows began to accelerate even faster:

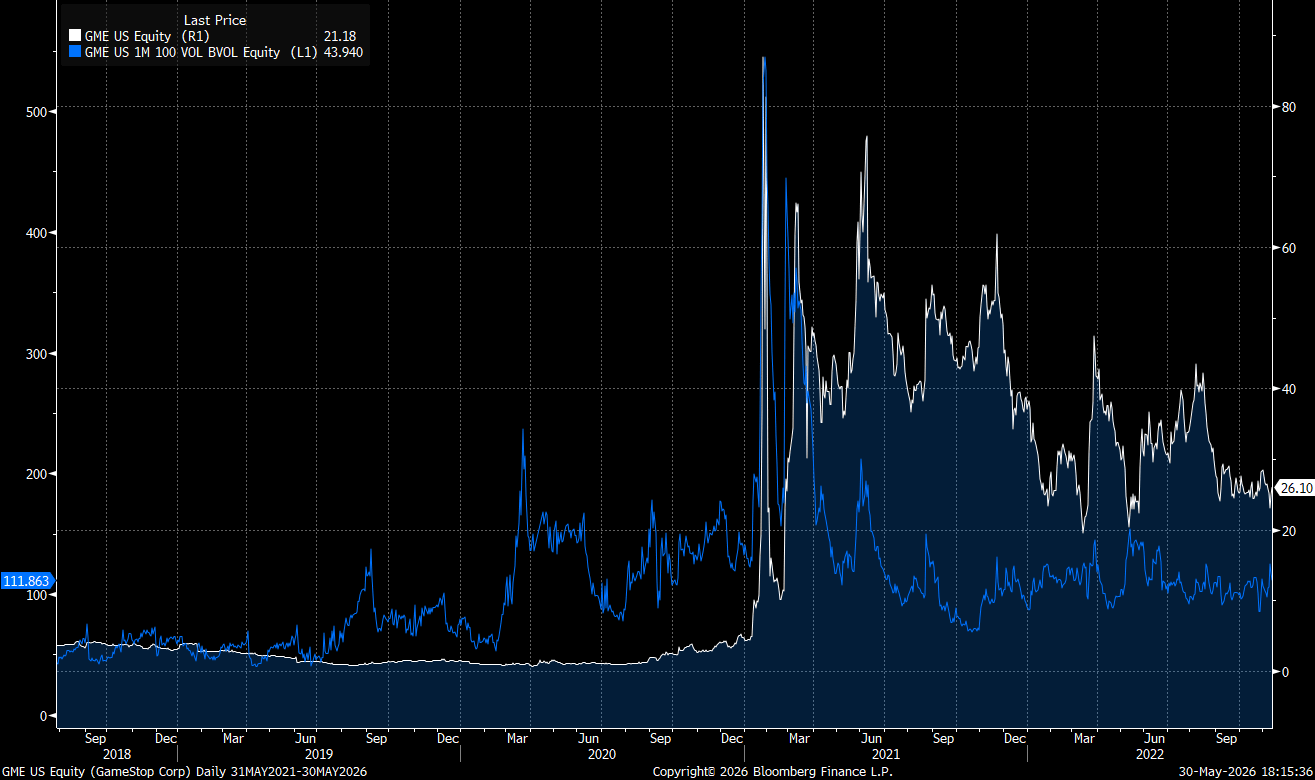

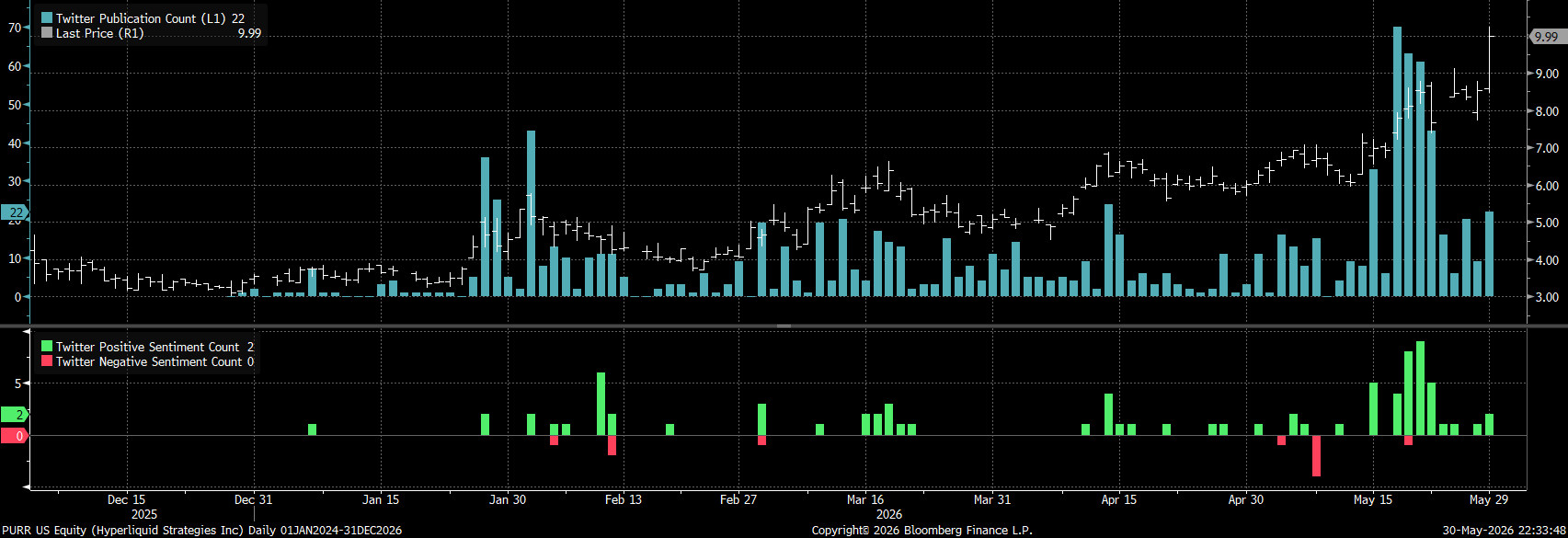

But things have shifted even more aggressively than I originally anticipated. We just had the largest day of volume in the history of PURR on Friday, as implied vol is rising with the price. When implied volatility is rising at the same time as the price, it shows there is a massive demand for calls.

This is where things are about to get incredibly unhinged, and the short-term upside is getting even more extreme. We are seeing massive call buying in PURR, which wouldn’t be a big deal if it were a larger stock with a larger tradable float. The problem is that it’s only a $1.4b market cap with a very small tradeable flow. This means that it only takes a small push to have a big move.

I wrote a short Twitter thread on this, explaining that once higher strikes are listed on the PURR 0.00%↑ stock, it is very likely to have a massive gamma squeeze because there just aren’t enough shares on the market to supply the demand for these types of squeezes. (please reshare this if you find it helpful)

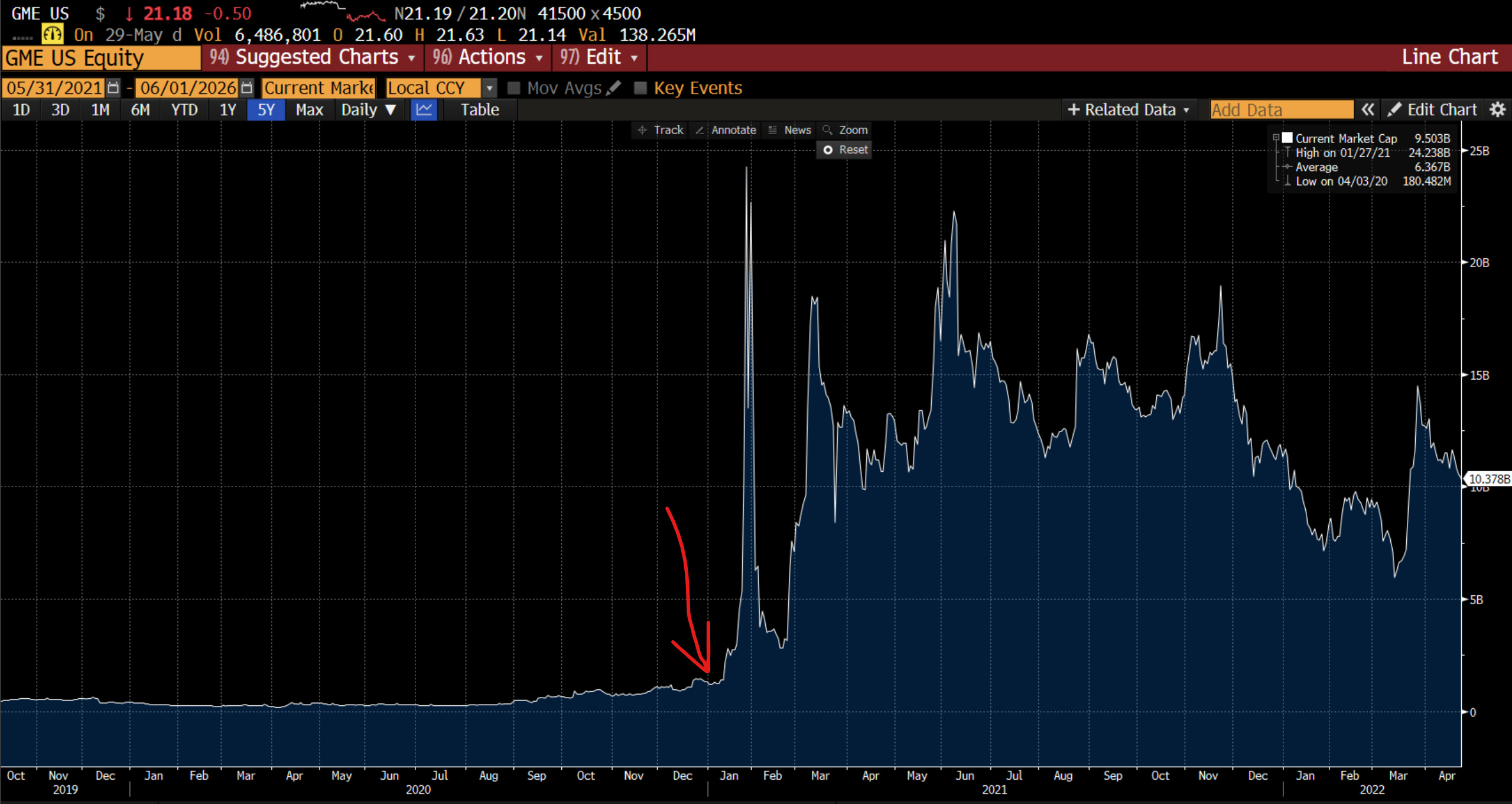

By the way, GME was at a $1.4b market cap right before it had its massive squeeze. I am not just drawing an arbitrary connection. This is 100% about a highly inelastic stock with massive potential for a gamma squeeze as higher strikes get listed and market makers are forced to buy shares in order to hedge their risk.

We only have strikes listed to $18 and it is highly likely that if we begin squeezing and they list higher strikes, a gamma squeeze will ensue. When a gamma squeeze happens, it is impossible to tell HOW HIGH a stock can go. This doesn’t even take into account that Hyperliquid could get integrated into the United States any day now, and PURR is THE only liquid market in the world right now to get call exposure to Hyperliquid.

Stack on top of this that PURR 0.00%↑ is getting added to the Russell this month, and you have the perfect storm for a massive call squeeze.

Again, it is literally impossible to know how high we can squeeze in such a low float stock during such an extreme part of the credit cycle (especially if Hyperliquid gets added!). If we follow the GME path, things could go way higher than anyone expects. The moment they list strikes higher than $18 dollars and volume begins to run through, it is game on.

I don’t think many people remember this but one of the main reasons for the short squeezes in 2021 was that higher and higher strikes kept getting listed on low float stocks during the credit cycle melt-up. If you traded during this time, then you know that many times we would trade all the way up to the highest strike and not go higher until more strikes were listed. During the gap ups in GME, this moved exactly in lockstep with how options were listed at higher strikes, and it happened well after shorts were covered.

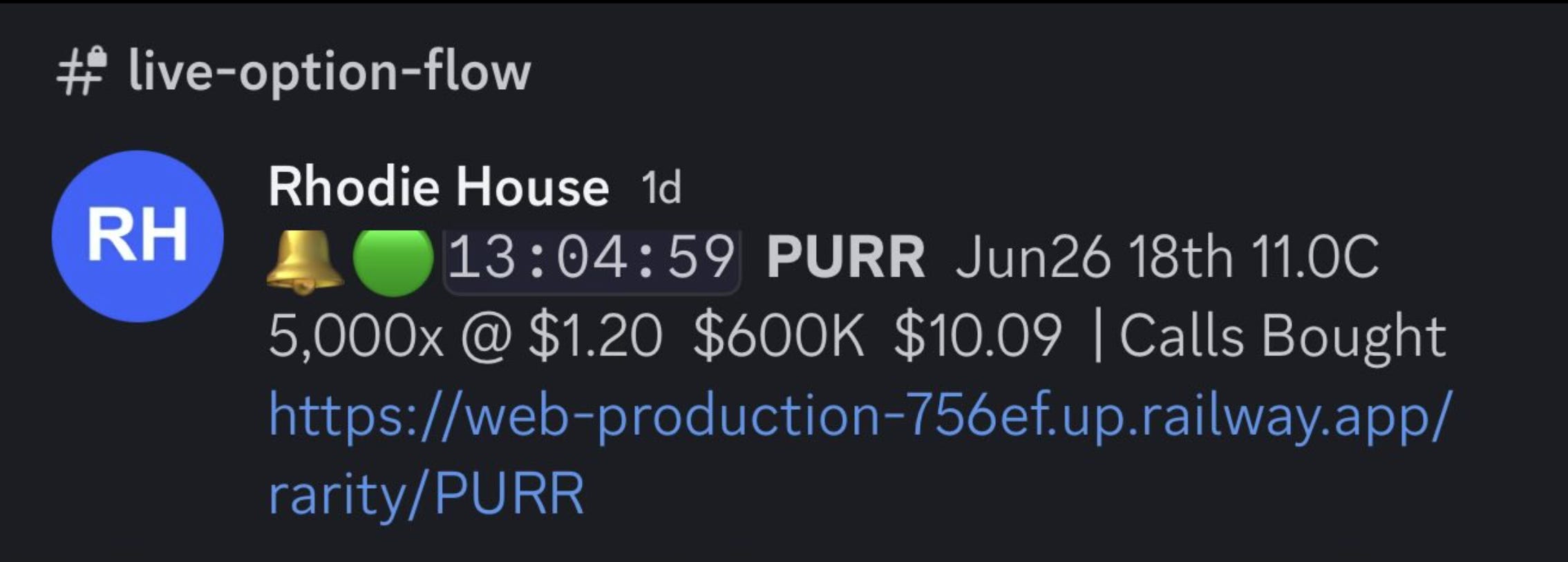

One of the tools I use to monitor option flow across situations like this is Rhodie House Options Intel. Judah does an excellent job at tracking these flows in real time, and if you’re actively operating in the option flow space, I’d recommend you check him out. We are going to see the flow for PURR come out in the option chain for the specific positioning dynamic I’m talking about.

The divergence in reality:

Everyone would like to think that Hyperliquid has “priced in” all of the good news because it’s all over the FinTwit timeline. I will say this over and OVER, sentiment isn’t a strategy. You need to map the flows of capital and what actually causes people to buy and sell instead of fading arbitrary accounts with zero signal. This is why understanding the fundamental thesis I laid out and the option strikes is so critical.

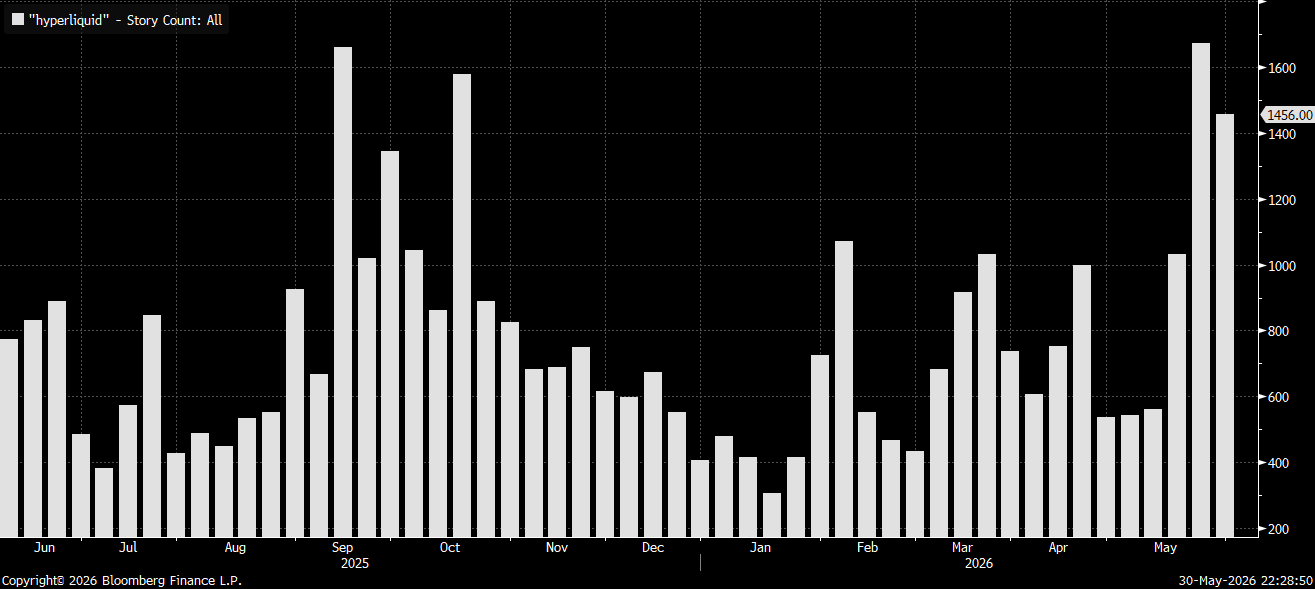

Even if we looked at quantitative metrics, article mentions of Hyperliquid are still below their 2025 highs:

Is there recognition of PURR on twitter? Maybe marginally relative to history. On the best days, there are 70 tweets mentioning PURR 0.00%↑.

On any regular day, there are thousands of tweets talking about treasury companies that have NEGATIVE P&L’s.

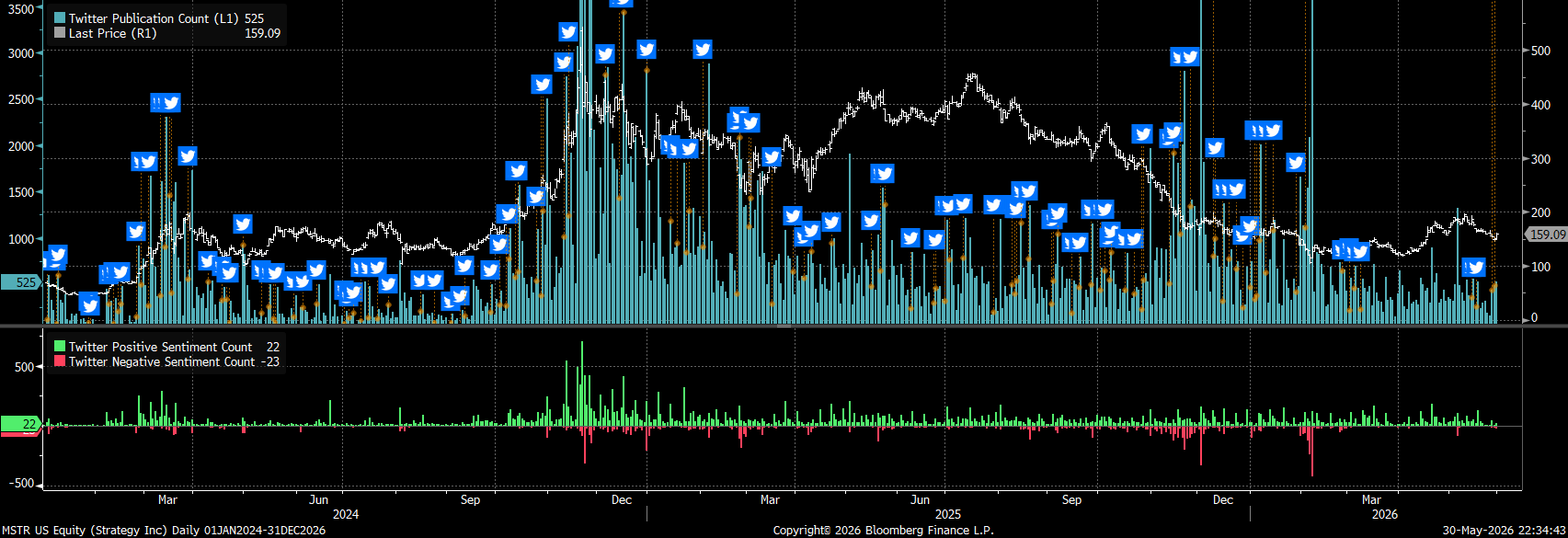

PURR is outperforming MSTR but has 1/100th of the recognition even on its best day:

The continual theme is that social media is a misleading machine meant to desensitize you to the actual causal mechanics in markets. It is supposed to distort your perception of reality and distract you. I explained this connects to the macro endgame we are approaching here:

The Endgame:

We are entering a macro endgame where the credit cycle, geopolitics, and AI are all converging so that everything has become the same trade. I continue to believe that significant risks are building under the surface but that the current flows are skewing equities to the upside. Therefore, I remain bullish on equities because we are likely to melt up much further before we crash.

We have entered the stage of the “everything rally” where capital is moving out the risk curve and you should expect crazier and crazier things to happen. Hyperliquid is the most disruptive and innovative project in the financial system right now and PURR is the single best expression of the trade.

I believe there is a very strong probability that we have a gamma squeeze in PURR within the next 60 trading days. If this occurs, it will gap up much higher than anyone expects.

I continue to hold the full PURR position into this.

Welcome to Global Macro. You get paid to hold risk.

The information on this website/Substack is for information purposes only. It is believed to be reliable, but Capital Flows does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of Capital Flows websites and systems including but not limited to data scraping, unauthorized entry into Capital Flows systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by Capital Flows and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to Capital Flows or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of Capital Flows.

I think you're overlooking a critical difference: GME had 140%+ short interest forcing covering, while PURR is pure gamma without that fuel. Gamma squeezes without shorts typically resolve faster and at lower multiples than what GME did. The Russell inclusion is also front-run by arbs weeks in advance, which often creates post-inclusion selling pressure rather than sustained buying.

The Hyperliquid thesis is solid, but comparing this to GME sets unrealistic expectations about magnitude and duration when the underlying mechanics are fundamentally different.

You're holding PURR into this... But are you holding it through this? Is a gamma squeeze move sustainable?