This is my next big bet

My entire goal in markets and on this Substack is very simple: map the macro regime so that I’m on the right side of it, and find the few large, asymmetric bets that become home run trades.

I laid out how Hyperliquid is going to disrupt the crypto and tradfi industry, and that the best expression is PURR 0.00%↑ due to the regulatory arbitrage. I laid all of this out for paid subscribers when we were in the low $3s, and we have almost doubled since then (link). This has been the largest position in my portfolio, and I continue to hold the trade (see my interview with the PURR CEO here: link).

Markets pay you to hold risk and take volatility. The entire industry is set up to suppress volatility, which is why when someone like Larry Ellison decides to take a massive bet and do the opposite of the entire industry, I want to be long.

My next big bet is ORACLE, and I am bullish with the following risk-reward (see my note below about building a position last week at $156):

If you were a paid subscriber, then you got my note last week about beginning to build a position in earnings around the $156 level and are now up after the pop. I have added more, and this is my next big trade.

If you want my entire thesis on Oracle, you can find it here. It is very simple, though. Larry Ellison has taken the entire company and leveraged the income statement and balance sheet to the AI build out, and he is the only major company that is pulling all negative returns into the present in order to have massive returns in the future.

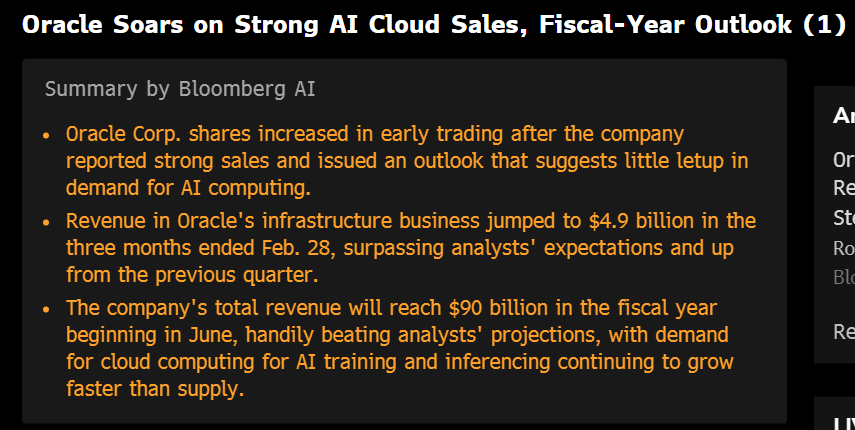

The earnings call is beginning to show the escape velocity of all their capex coming into sight:

Keep a very close eye on the TradingView indicator I provided to map the flows. We need to see continued buying pressure from sector flows and fundamental flows in Oracle: https://www.tradingview.com/chart/2taQ63im/

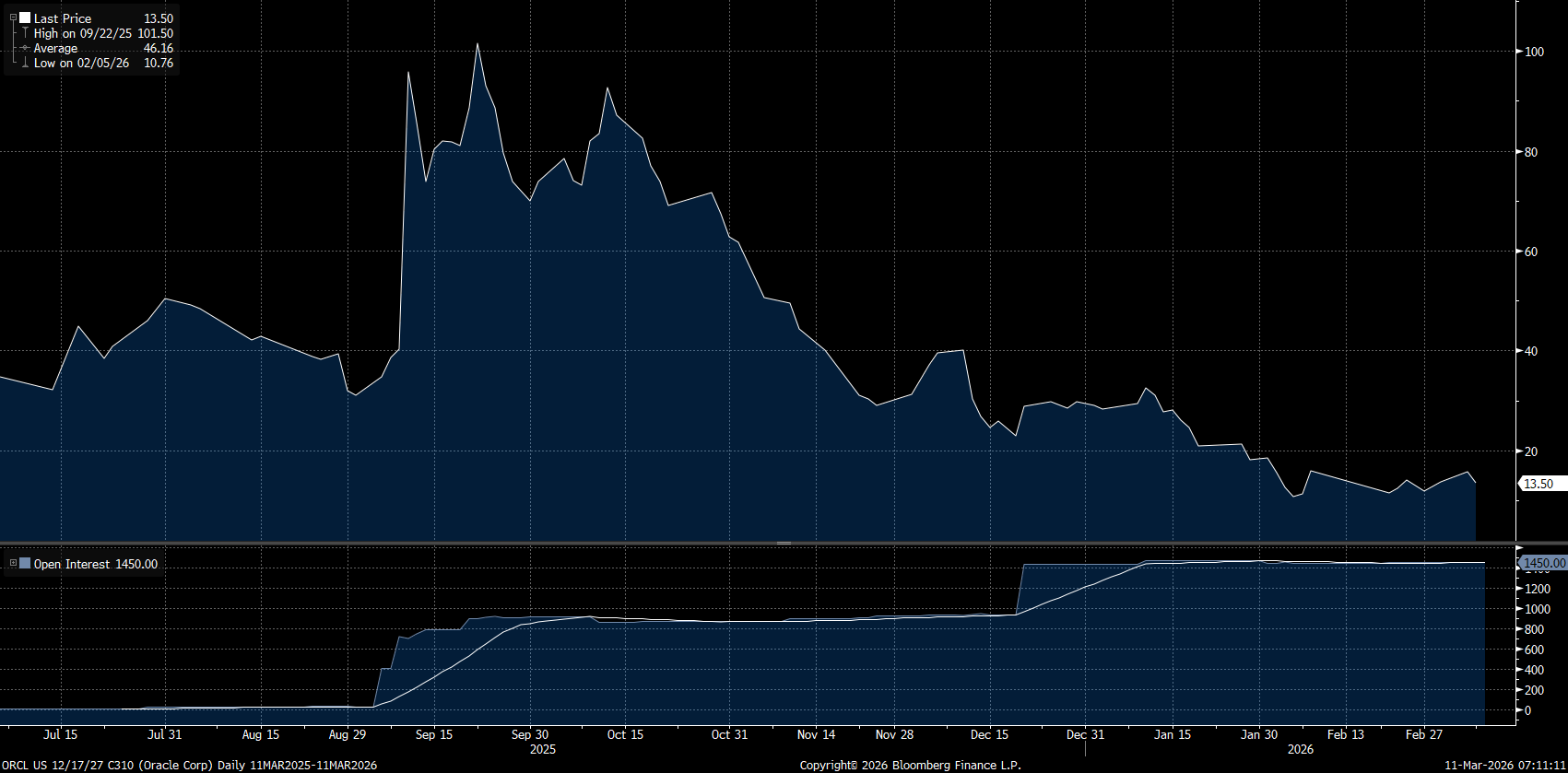

I am taking a small portion of my Oracle exposure and putting it into ORCL US 12/17/27 C310 Equity:

My Large Cycle View:

I have been very clear that I believe the current macro environment is unsustainable. We have significnat structural risks building under the surface in liquidity, the microstructure of the market, and positioning. However, we are not at a point in the cycle where there is a constraint to unwind it. And this is a global phenomenon.

This is why my recent comment to Burry focused on how to relate the changes in AI with macro liquidity. I believe there is a ton of importance to the risks Burry brings up, and I will always have respect for any risk taker. My larger concern is why all equity indices are sitting at all-time high valuations, and the driver of this:

If you want to understand more of my thought process around these trades and my current framework on the macro regime, I will be doing a livestream tomorrow at 9:15 AM MT.

Here is the link for joining:

The information on this website/Substack is for information purposes only. It is believed to be reliable, but Capital Flows does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of Capital Flows websites and systems including but not limited to data scraping, unauthorized entry into Capital Flows systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by Capital Flows and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to Capital Flows or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of Capital Flows.

The Hyperliquid call was well-structured. The Oracle thesis is interesting precisely because Ellison is doing what most CFOs won't: pulling future returns forward through the income statement and accepting the pain now. The question I keep coming back to is how this interacts with the liquidity constraints you flagged. If the macro unwind comes before the capex payoff window closes, the leverage cuts both ways. What's your trigger for reassessing the position size?

Hi Cap, where's your head at now with the Oracle trade? Lots of chatter about 5 year CDS. I feel like I don't want to buy anything right now, but does your thesis still stand in a scenario where the Iran war comes to some kind of conclusion without a radical market move?