The Credit Cycle Melt Up Always Sows The Seed Of Its Own Demise

The absurd principles that push you to think differently than others

The World Is Short Volatility

The entire world is short volatility, and it has to be. In a system where change compounds faster than capital can react, non-participation is the greater risk. Sitting out is not safety. It is a slow, certain form of loss.

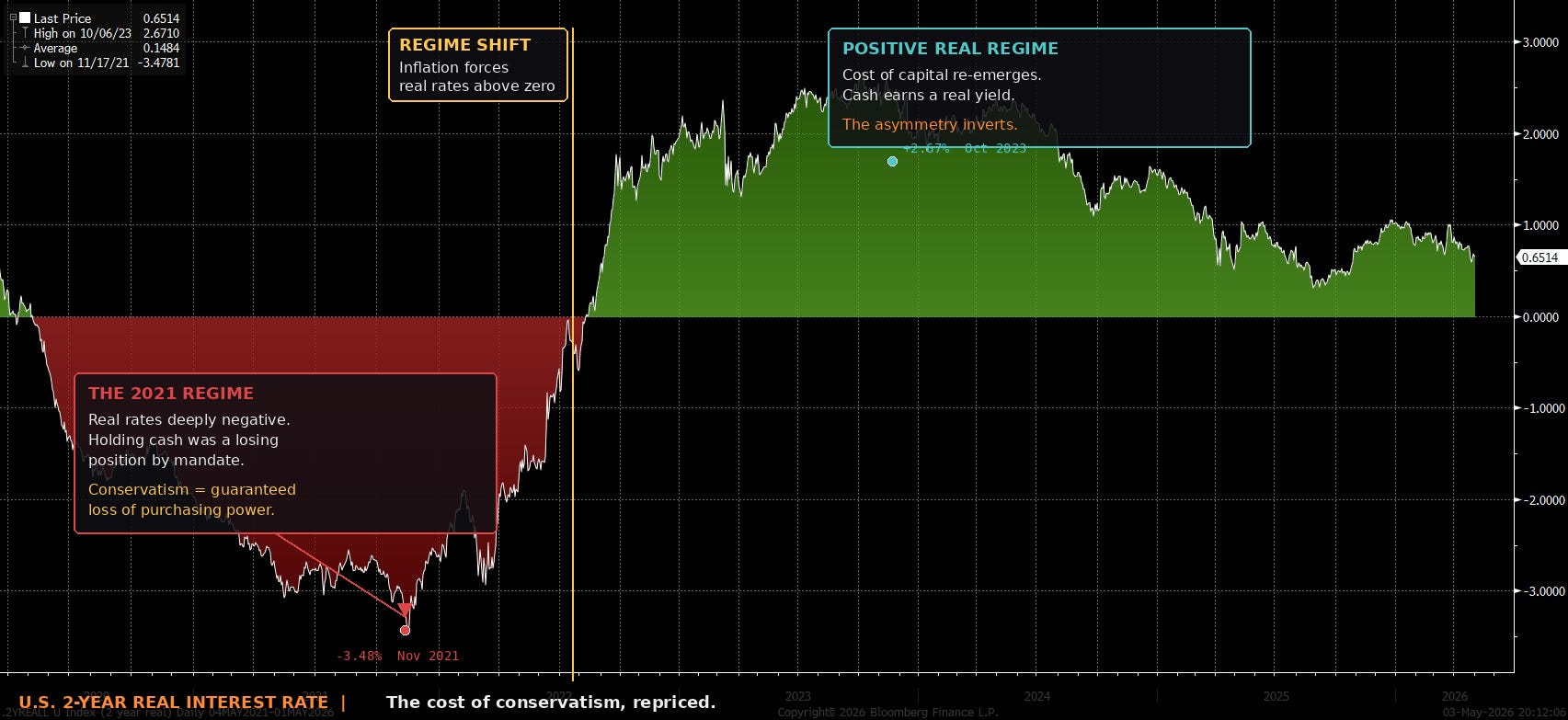

The 2021 cycle made this explicit. Real interest rates were negative. Holding cash meant losing purchasing power every month while the underlying economy was being retooled at a pace without precedent. Digital infrastructure, supply chains, social media distribution, e-commerce algorithms, and global integration all advanced simultaneously. The cost of conservatism was visible in real time. The participants who refused to be long change were quietly liquidated by inflation and obsolescence.

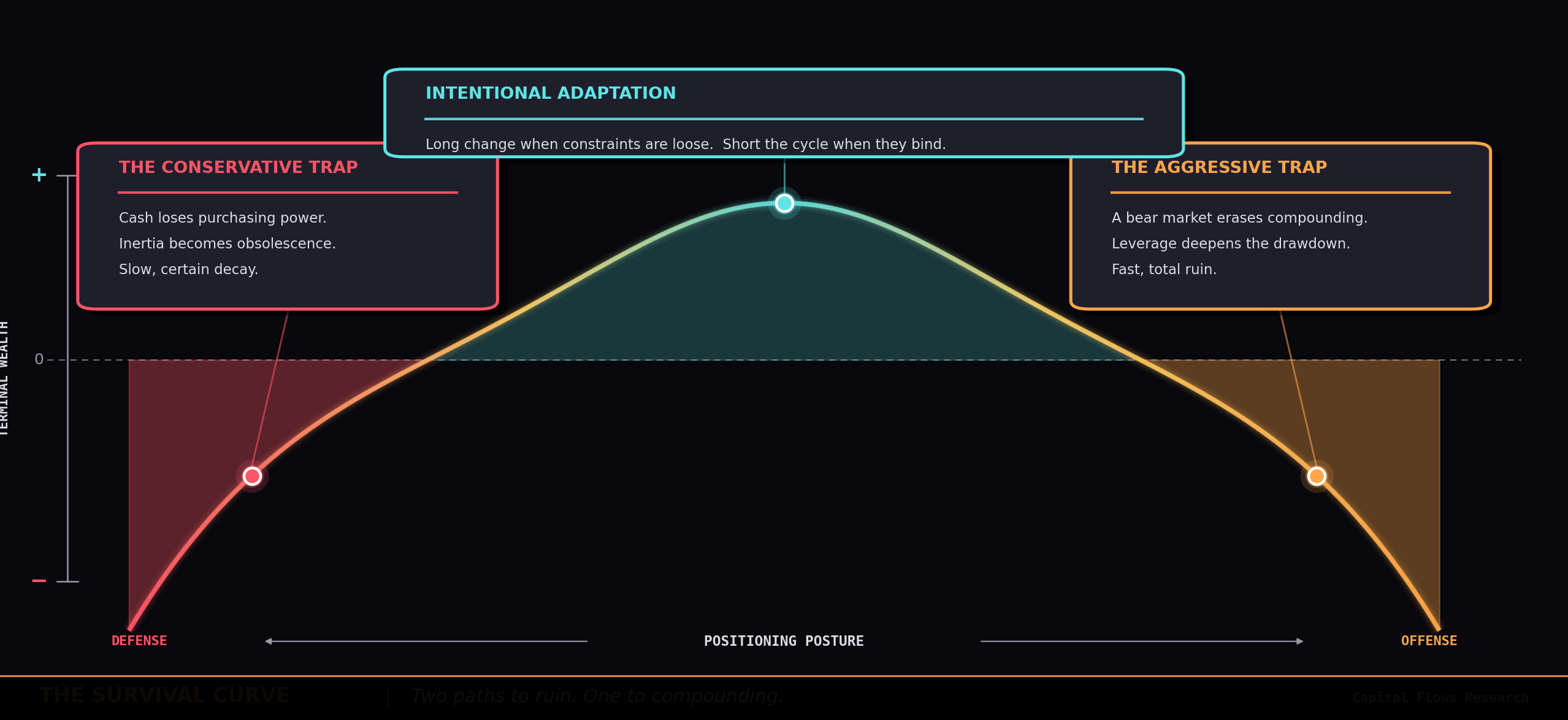

There are two paths to losing money. The first is being so conservative that you fail to adapt to structural change and watch your purchasing power erode. The second is being so aggressive that the eventual bear market washes you out and destroys the compounding you spent years building. Survival does not exist at either extreme. It exists in intentional adaptation. The discipline is knowing when to be long change, and knowing when the system has reached an unsustainable moment in which macro constraints begin forcing participants to sell the positions they have held longest and loved most.

2021 Was A Liquidity Cycle. 2026 Is A Technology Cycle.

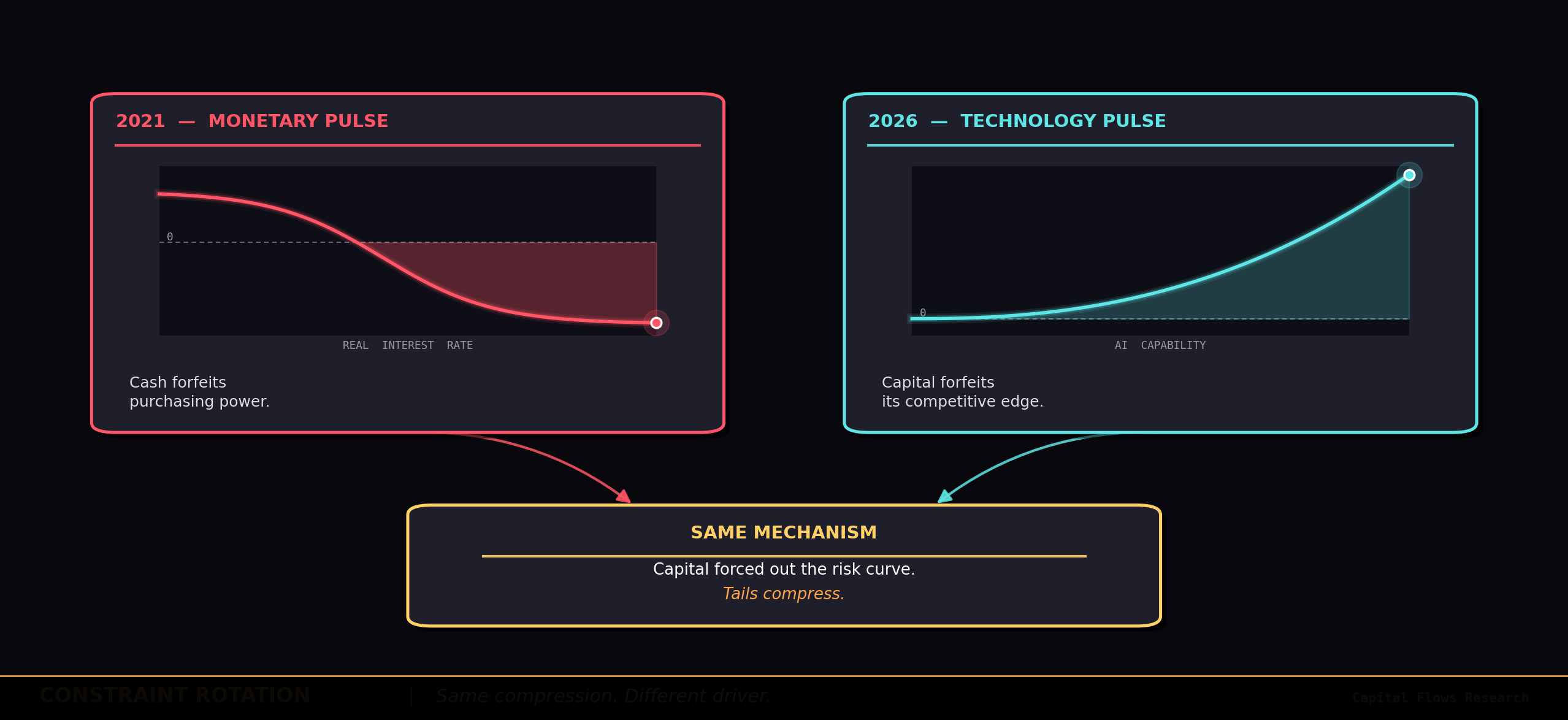

The cycle that made cash a losing position in 2021 is repeating itself, only the driver has rotated. In 2021 the constraint was monetary. Real interest rates were negative and capital was pushed out the risk curve by mandate. Today, I believe it is the same mechanism with a different input. The constraint is technological. AI is restructuring the production function of every industry at once, and the participants who fail to engage with it are forfeiting their edge the same way cash forfeited purchasing power. Software margins, distribution channels, supply chains, hiring decisions, and customer acquisition curves are all being rebuilt around models in real time. The input has changed. The mechanism has not.

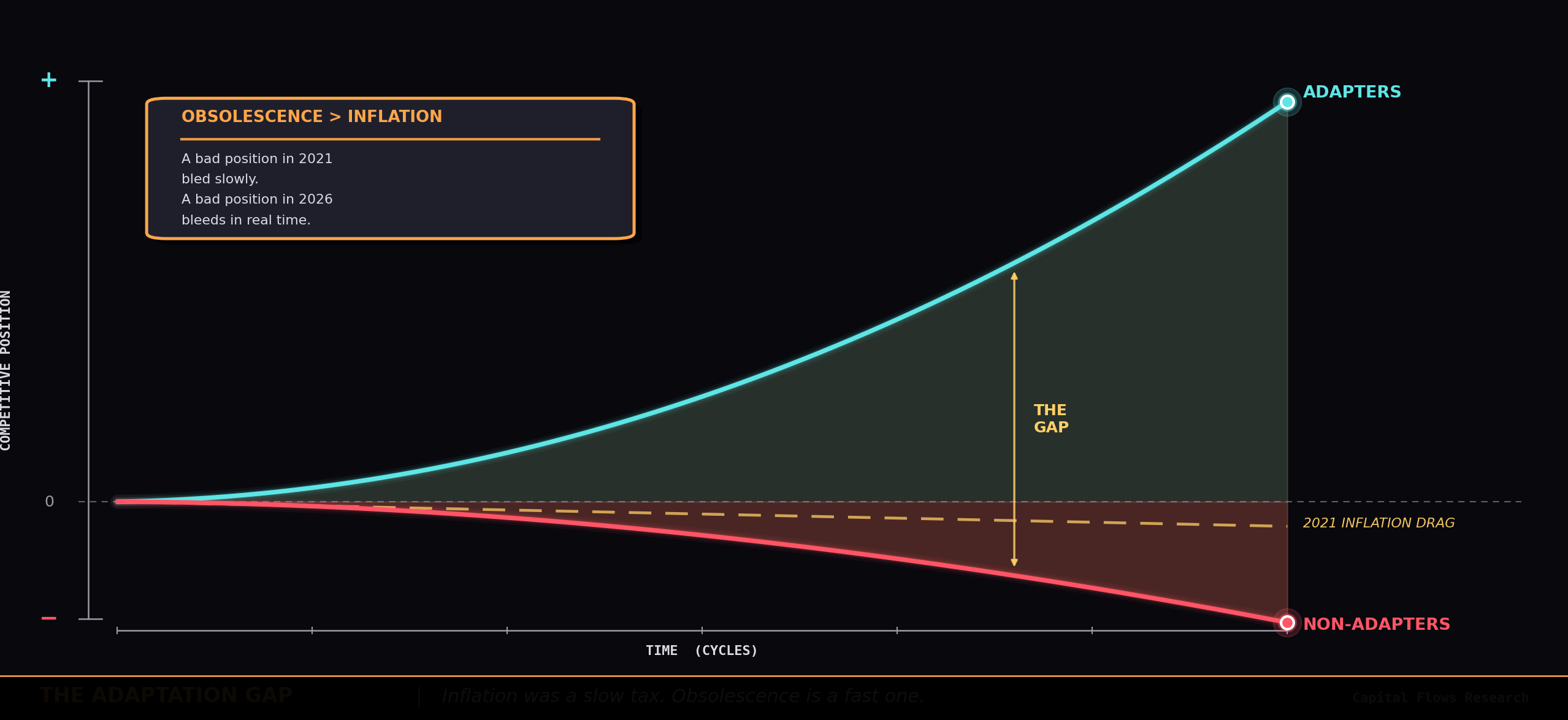

The cost of sitting out AI is not the slow erosion that defined 2021. In my view, it is competitive obsolescence, and it compounds faster than inflation ever did. A firm that fails to deploy AI loses its cost structure to one that does. A portfolio that fails to own AI exposure loses its return profile to one that does. The decision not to participate is a short position on adaptation, and the position bleeds every quarter, every product cycle, every hiring round. The conservative trap from the survival curve applies with greater force here than it did under negative real rates. Inflation was a slow tax on capital. AI obsolescence is a fast one.

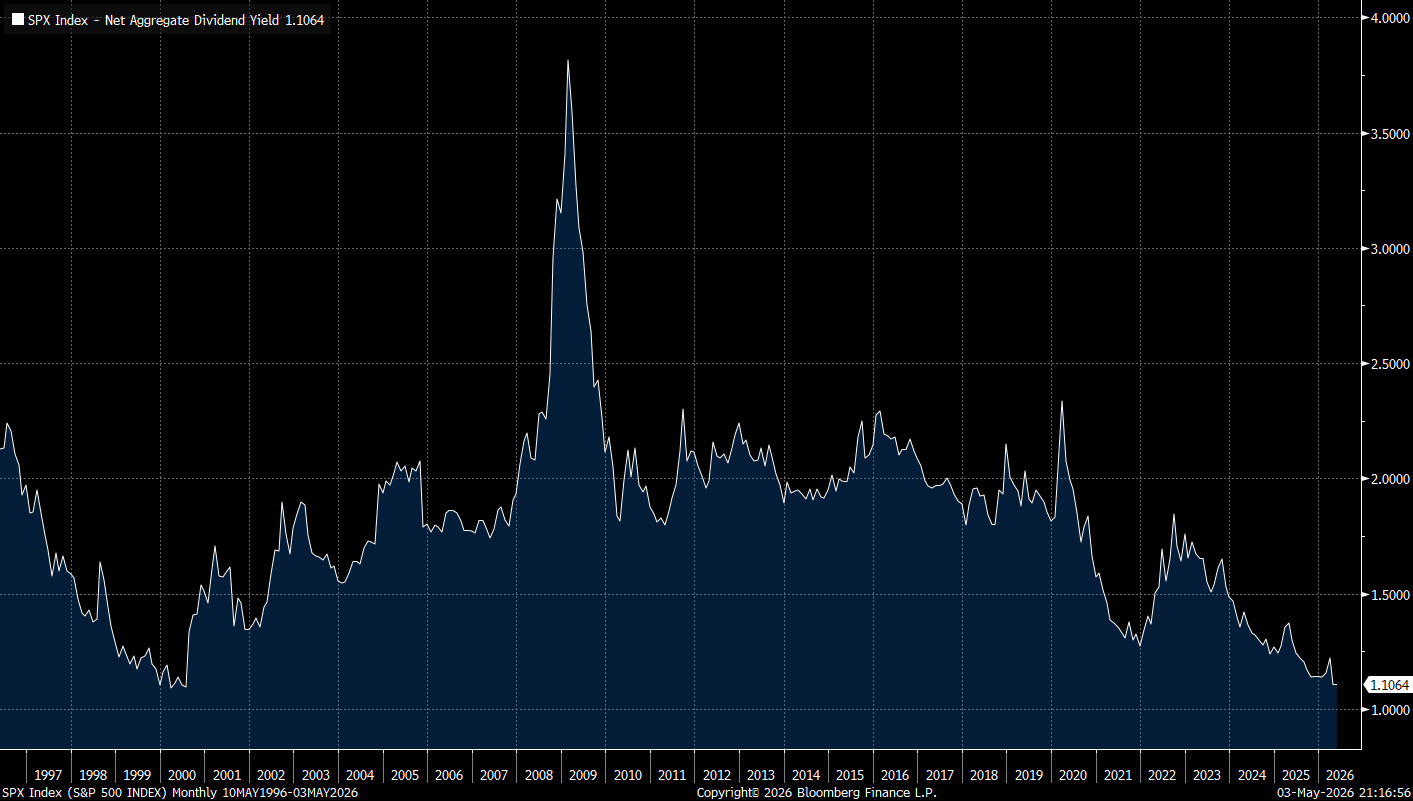

And yet we are seeing the system at the highest valuations in modern history. The SPX dividend yield has compressed to levels that map directly onto the late-cycle dynamic of 2021. The explanatory variable has changed. The compression has not. The marginal AI buyer has already bought.

My Main Point:

The point here is straightforward. We have a very clear analog to 2021, with one substitution. In 2021 the primary constraint was monetary. Today we still have monetary support, with real rates hovering near the zero bound, but the new constraint is technological. AI is forcing capital into equities the same way negative real rates did four years ago.

As I have been laying out for months, every signal points to a credit cycle melt-up unfolding in real time. And no country can afford to let its economy slip into recession right now, because China will use any opening to complete a final hollowing out of the Western industrial base. The credit cycle is no longer just a financial cycle. It is a piece of economic statecraft. Letting it break is not a policy choice anyone can afford to make. I would strongly encourage you to read these reports on the topic!

Walking The Thin Line: How AI Is Compressing The Tails

Tomorrow I’m walking through the thin line the market is currently walking. The credit cycle is melting up, AI is forcing capital out the risk curve, and policymakers cannot afford a recession with China waiting on the other side. Every one of those forces compresses the tails further.

I strongly believe that this is one of the most important periods of time in history, which is why I am doing these livestreams every single day. You can always find the recordings of the daily livestreams here: LINK

Here is the slide deck from the livestream I recorded on Friday (LINK), which explains WHY interest rates cause the rise and fall of nations. I also laid out every resource in the slide deck you would want to dig into if you’re the type of person who wants to build real knowledge about how money actually flows in the economic system.

Tomorrow’s Livestream: LINK

The information on this website/Substack is for information purposes only. It is believed to be reliable, but Capital Flows does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of Capital Flows websites and systems including but not limited to data scraping, unauthorized entry into Capital Flows systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by Capital Flows and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to Capital Flows or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of Capital Flows.

The 2021 analog is persuasive until you account for one difference: AI capex is actually productive spending. Negative real rates just inflated asset prices. AI spending creates real compute output that businesses pay for. Whether that makes the valuation compression sustainable is the whole argument.

The World Has Changed. Most People Haven’t Noticed Yet.

We are no longer in a normal economic cycle.

We’ve entered a new era one where inflation, geopolitics, and energy shocks are rewriting the rules of global markets.

Central banks like the Federal Reserve, European Central Bank, and Reserve Bank of India are not just managing economies anymore.

They are defending stability.

What’s really happening?

• Inflation isn’t temporary. it’s becoming structural

• Oil is no longer just a commodity. it’s a geopolitical weapon

• Interest rates are staying higher for longer

• Markets are no longer driven by easy money

This is not a slowdown.

This is a reset.

The hidden force: Energy

Oil above $100 is not just a price spike.

It’s a signal.

A signal that:

supply chains are fragile

conflicts are shaping costs

inflation can return anytime

Every oil shock today is a global economic shock.

📉 Markets are changing too

The old playbook:

→ Cheap money

→ High growth

→ Fast gains

The new reality:

→ Expensive capital

→ Selective growth

→ Volatility

Markets are no longer rewarding speed.

They are rewarding discipline.

The biggest shift most people miss:

We’ve moved from a world of abundance

to a world of constraints.

And in this world:

Strong businesses win

Weak models break

Patience beats timing

What should you do?

• Focus on quality, not hype

• Think long-term, not short-term

• Stay calm during volatility

• Build resilience, not just returns

This is not the end of opportunity.

It’s the end of easy opportunity.

The future will not reward those who react fast.

It will reward those who understand deeply and act wisely.