Trades: Updates

Steepener

“Clear thinker” is a better compliment than smart

-Naval

In the information age with infinite leverage, your ability to think clearly and have decisive judgment is the only way to achieve success. Hard work is a prerequisite to build this judgement but the ultimate decision is a result of clear thinking that grows out of the soil of hard work.

One of the key things I want to focus on today is how the shape of the yield curve is dynamically changing. If you are new, check out the bond primer I did here:

The Research HUB: The Bond Market

Hello everyone, Many subscribers have been asking for a primer on how the bond market works. In this article, I'm going to provide a breakdown with a TON of resources. My goal is to keep things clear and simple, avoiding any complex math. After reading this article, you'll see that understanding the bond market is essential for understanding macroeconomi…

Also check out Citrini’s recent articles as well:

Main idea: when the curve is inverted (long-end rates lower than short-end rates), banks and institutions are not incentivized to take on additional duration risk relative to the short end.

Think about it like this, if I can “T-bill n chill” in the short end getting paid 5.50%, why would I buy TLT when it’s yielding 100bps less?

The short-end pricing and long-term NGDP conditions account for changes in the shape of the curve across various durations. Prometheus Research and I did a whole conversation on how this functions in the term premia discussion:

Macro Alpha Webinar With Prometheus Research

We have a special treat today! I had a conversation with Aahan from Prometheus Research on how the mechanics of interest rates function. We discussed HOW to correctly conduct attribution analysis on interest rates and WHY the steepener trade has positive optionality from here. These types of conversations give you a peak behind the curtain of the multifaceted macro models Prometheus builds.

Where are we now?

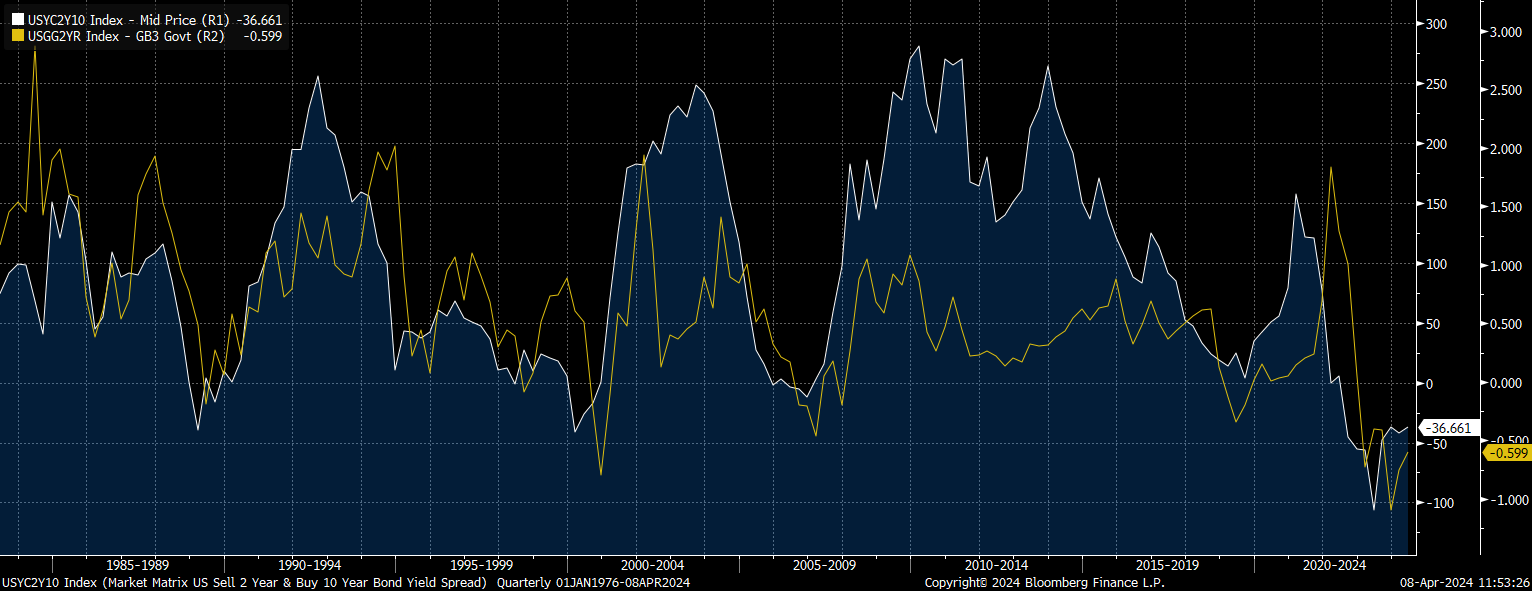

The 2s10s curve has steepened marginally since March but on a long-term basis, it remains in a range. On the other hand, the 3m2s curve has steepened significantly since January:

It is divergences in these curves that are critical to connect to tensions in the bond market:

What will cause a durable rally in bonds? We need to see persistence in a bull steepening for duration to have a sustainable rally. What causes this? it is the collocation of the Fed cutting rates AND nominal GDP conditions deteriorating considerably.

YoY nominal GDP is running at 5.9%:

And we have headline CPI ticking up marginally due to the rallying in crude prices:

On top of this, NFP just came in above expectations. Not a recession!

Bonds remain in a mean reversion range where alpha opportunity exists in taking the other side of market extremes into market catalysts. Within this, betting on the steepener continues to have a high-risk reward.

Keep reading with a 7-day free trial

Subscribe to Capital Flows to keep reading this post and get 7 days of free access to the full post archives.