Interest Rates, Equities, Recession?

Recession = interest rates down but interest rates down doesn't = recession

Hello everyone,

There has been some confusion among people in the news media and social media regarding how the relationship between stocks and bonds functions in both the presence and absence of a recession. For example, I keep hearing that if rates are going to come down, a recession is likely to occur. This is a conflation of two separate variables.

While rates typically fall during recessions, a fall in rates doesn’t mean there is a recession.

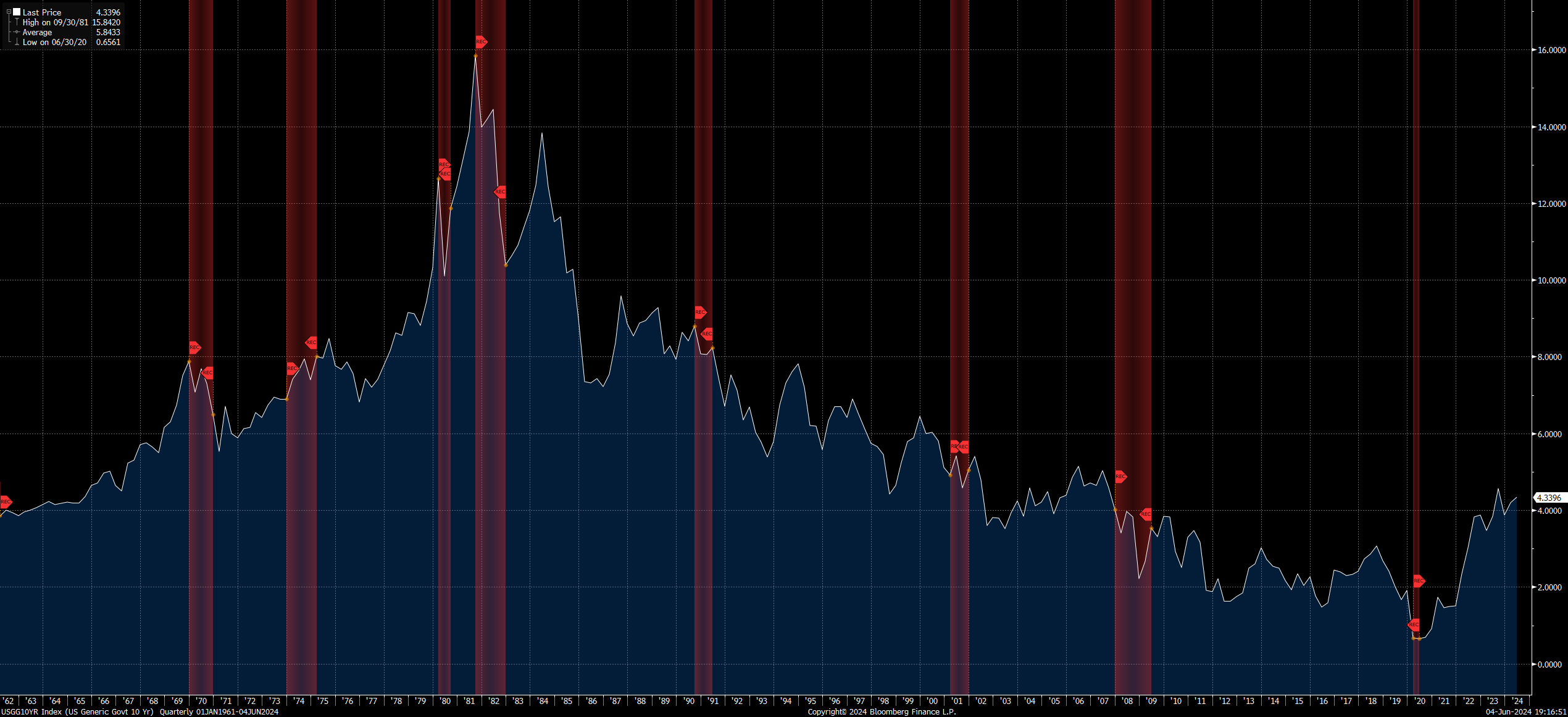

First, notice that interest rates can trend down for prolonged periods without a recession occurring. The fact that interest rates move down is often the reason a recession DOESN’T happen.

I have laid out the big picture of equities and rates here:

The Big Picture For Equities and Rates

Hello everyone, There are a lot of new people joining so I want to welcome you to the Capital Flows Substack. This is the place where I share all of my research, ideas, and trades for financial markets and life. If you are brand new and trying to get your barings, I have aggregated all of the educational primers in one place. There are comprehensive primers on how to think about equities, rates and overall macro. I have provided extensive lists of additional academic resources in each so that it will provide value to someone who is brand new or has been around markets for a while.

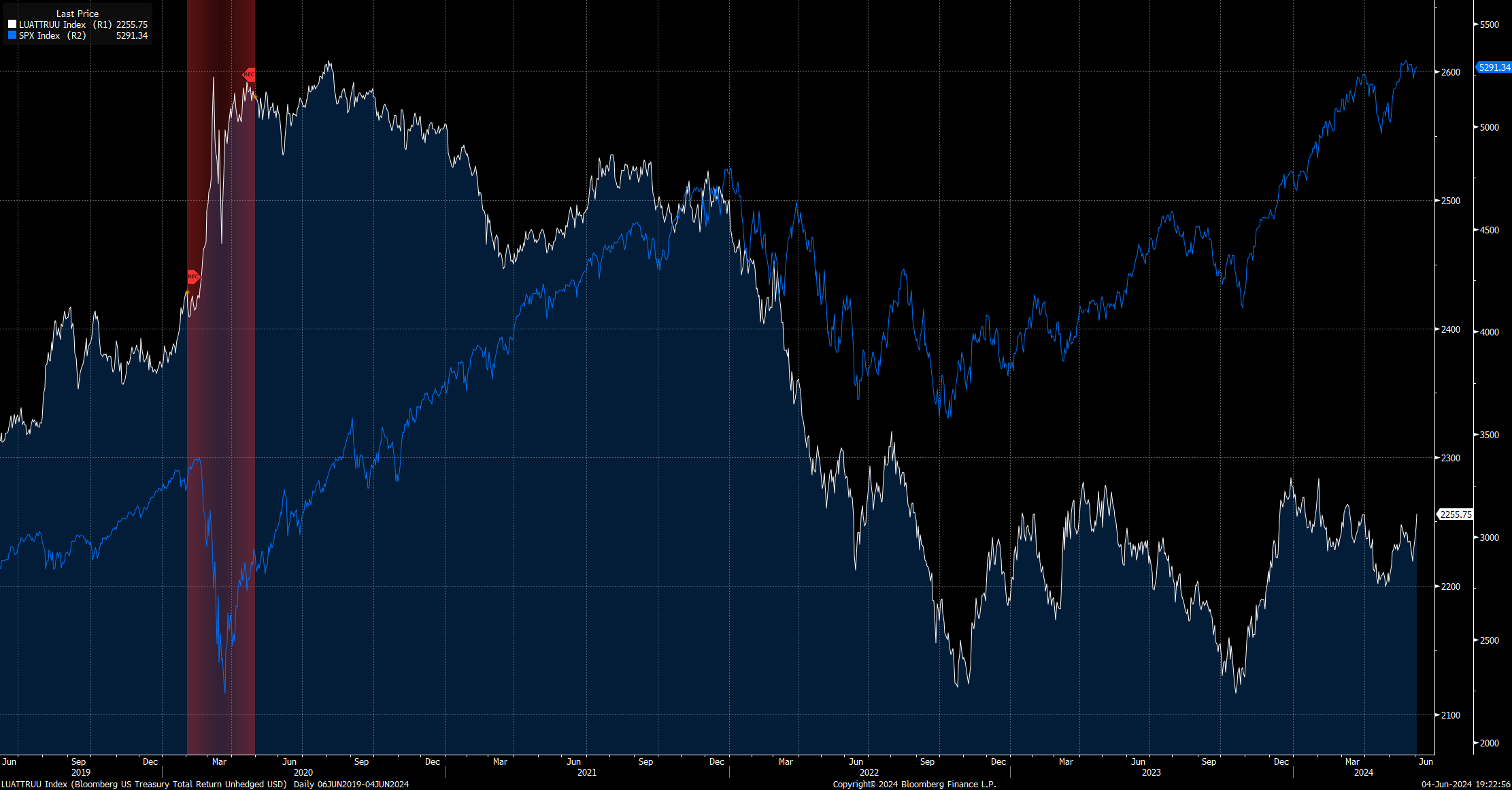

Remember, equities and bonds can rally TOGETHER for a prolonged period of time.

Thinking in a zero-sum way between stocks and bonds generates extreme views that don’t generate positive returns. For example, people thought that bonds had to rally if stocks sold off.

2022 crushed that false notion:

Then people believed that since bonds were rallying during 2023 that a recession was imminent. Then stocks and bonds rallied together:

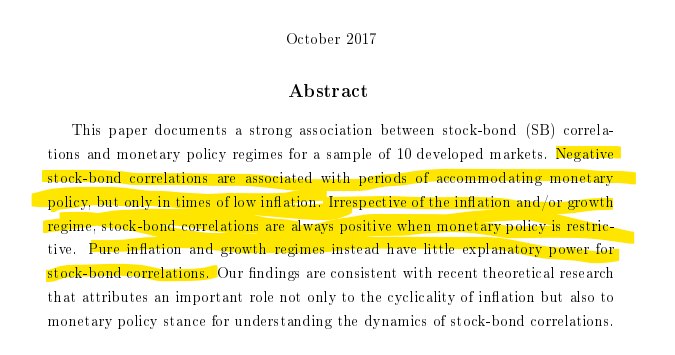

If you want to dig into this more, this is one of the main papers on the stock-bond correlation is this: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3075816

Just remember, people are always going to extrapolate a single part of the system to the whole. Your goal should be to see how each part of the system uniquely contributes so that the whole is GREATER than the sum of its parts.

The yield curve (and outright rates) function in a reflexive feedback loop with nominal growth. This creates path dependency between the two. I touched on this idea in the interest rate primer:

Interest Rates Primer

The Big Picture: I remember when I first started studying why interest rates were important. It was one of the most eye-opening experiences of my life. I originally thought interest rates were irrelevant yields that the boring parts of portfolios were made of. Stocks were always where the cool kids were making money. After conducting a historical study …

Main takeaway: I still have the view that a recession is unlikely in 2024. If the evidence changes then I will change.

If you want some homework, go look at 2019 and how much the ISM decelerated while the market rallied to all-time highs. Perma bears were having the time of their lives in 2019 on this divergence.

Most people forget that bonds tend to lead stocks.

I like that FM: "The Mexican Peso (MXN) may be moving due to the Finance Minister's intervention to prevent further depreciation following election-related declines, reassuring investors about fiscal discipline and investment continuity. Additionally, market sentiment towards risk influences MXN performance during periods of turbulence or stability. Economic data showing unexpected slowdowns in Gross Fixed Investment post-election could also impact MXN valuation as it reflects potential legislative changes that might affect the economy negatively. Analysis of global currency returns, points to MXN movement as the main driver of the cross."