The Credit Cycle and AI Are Sowing The Seeds Of Risk

AI is sowing the seeds for the future bear market

The rules are changing.

When the balance sheet and income statement of the largest economy on earth become cross-collateralized with how AI and global trade unfold together, the way that people thought the world always worked begins to shift. Everyone assumes it’s just a temporary disruption that will mean-revert, and they slap the “nothing ever happens” sticker on it.

This is not a temporary disruption. The rules of the game are shifting at the structural level. AI is simultaneously displacing service-sector labor, enabling autonomous manufacturing, attracting hundreds of billions in credit issuance at the tightest spreads in a generation, and pulling the largest foreign capital inflows into US equities in history. These are not separate stories happening in parallel. They are one integrated system, and the transmission mechanism that links them all is the credit cycle.

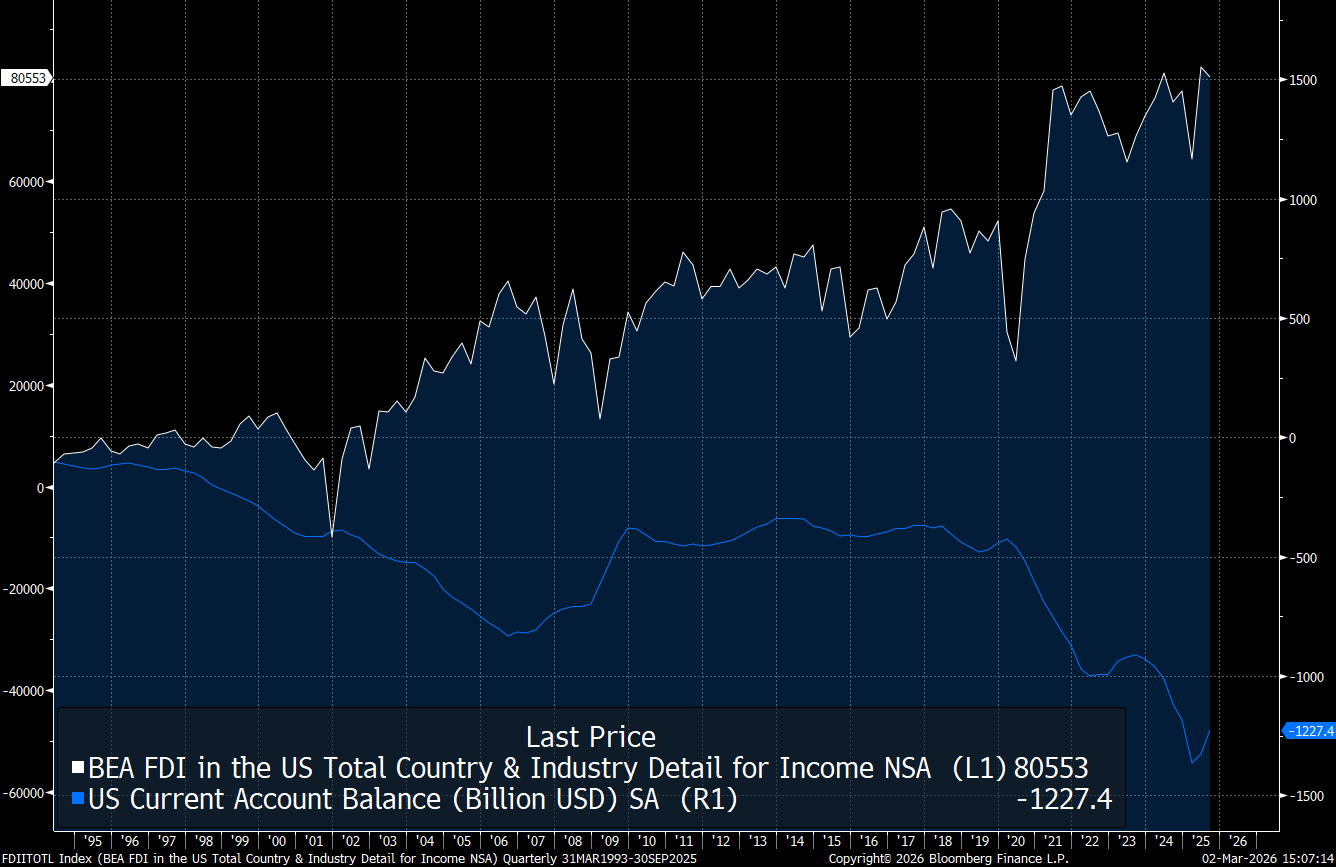

Foreign direct investment in the US (white) is at a historic high at the same time the current account (how much the US imports vs exports) is at a historic low. The simple point here is that everyone has taken the dollars they’ve gotten from trade and invested them in US equities.

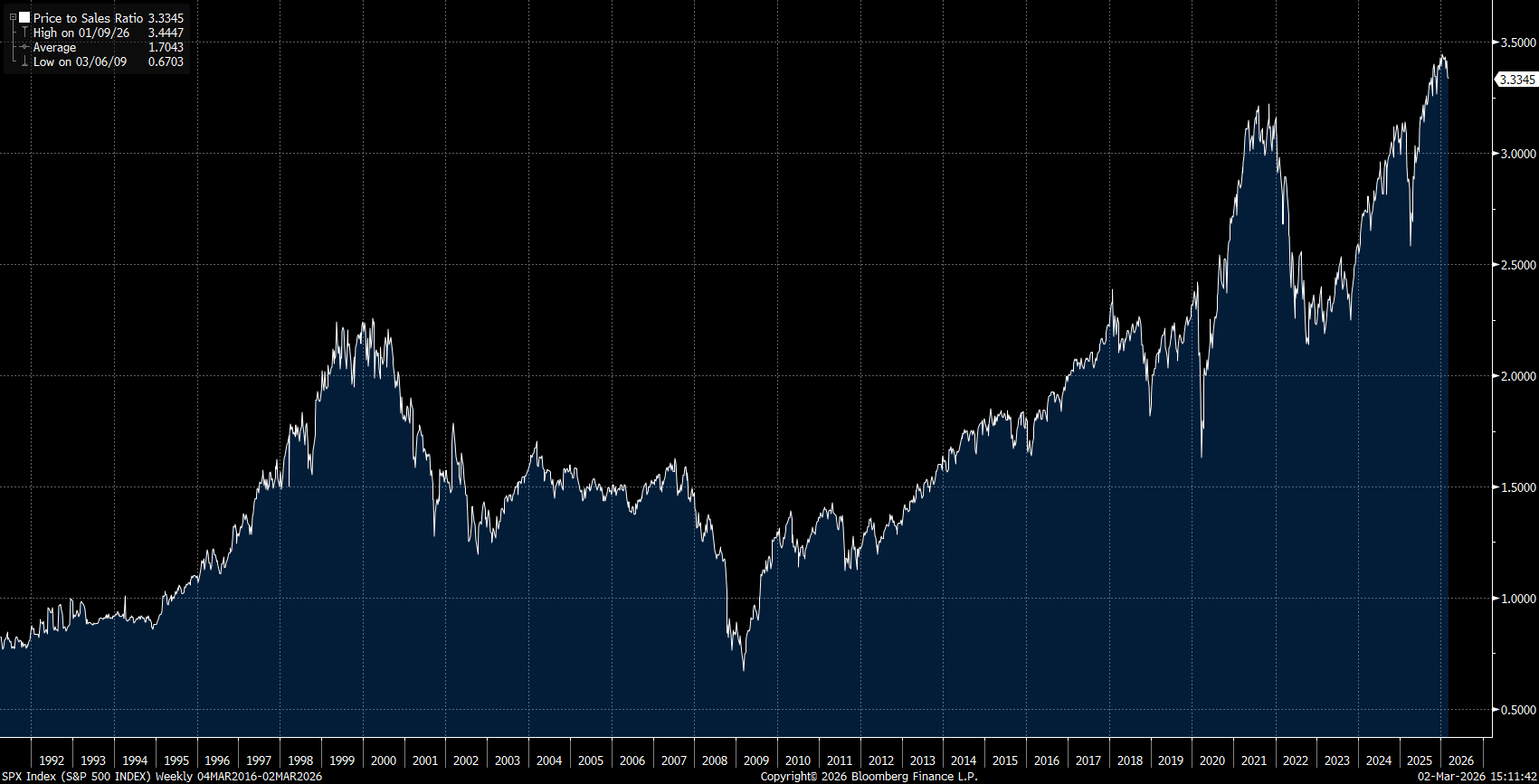

The capital flows from foreigners have flowed directly into the AI theme, which has pushed US equity markets to the highest valuations in history.

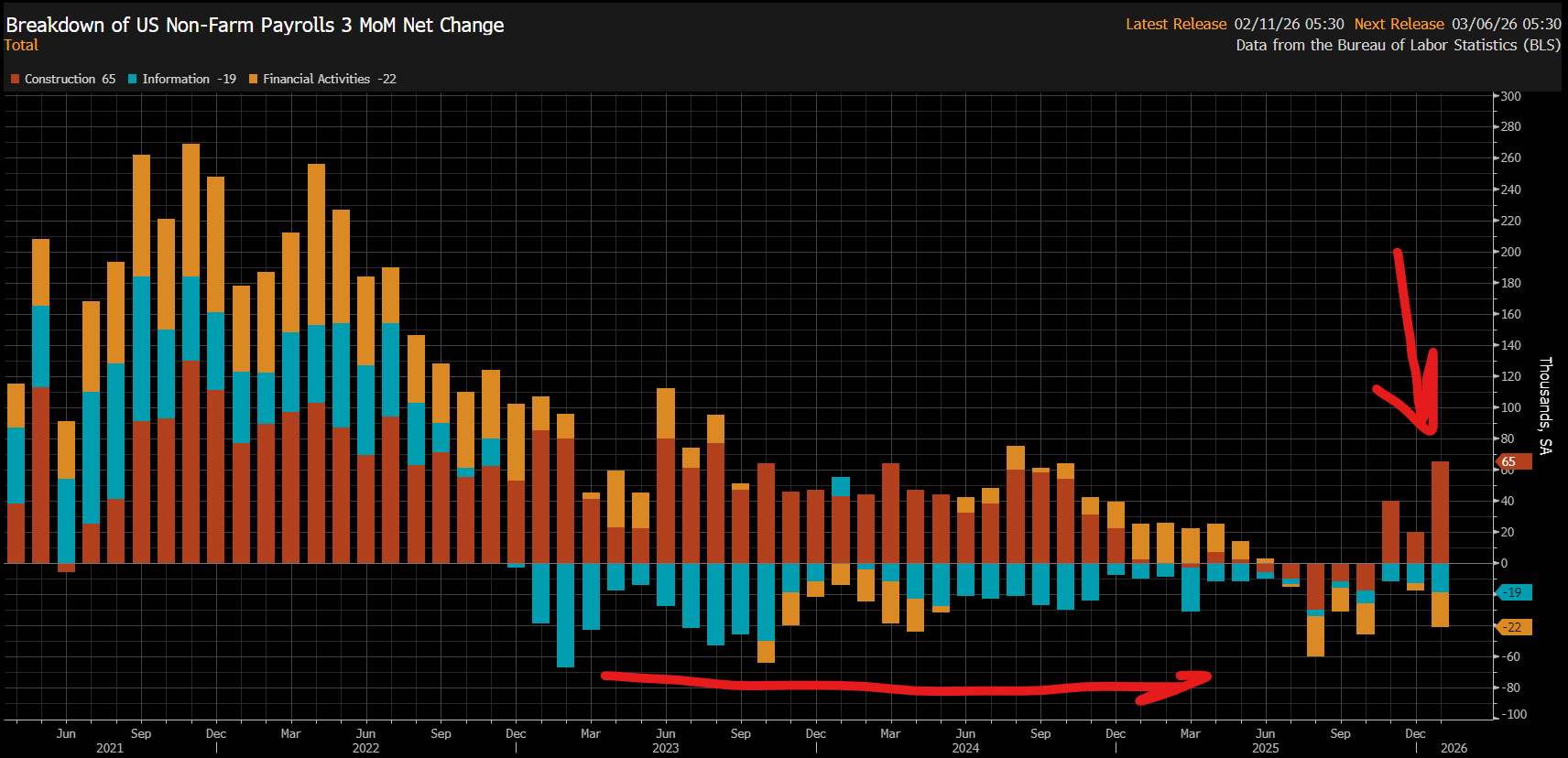

The problem is that as capital flows into AI-related themes, AI is rebalancing the entire labor market and trade, which are themselves the two largest sources of capital supporting these valuations. Notice here that the information technology and financial services sectors have been contracting in their share of the labor market growth, while sectors like construction are rising.

This is playing out in the public markets right now as all of the companies with the highest sensitivity to the power portions of the AI supply chain are benefiting the most, while names in the fintech and information space are getting hammered.

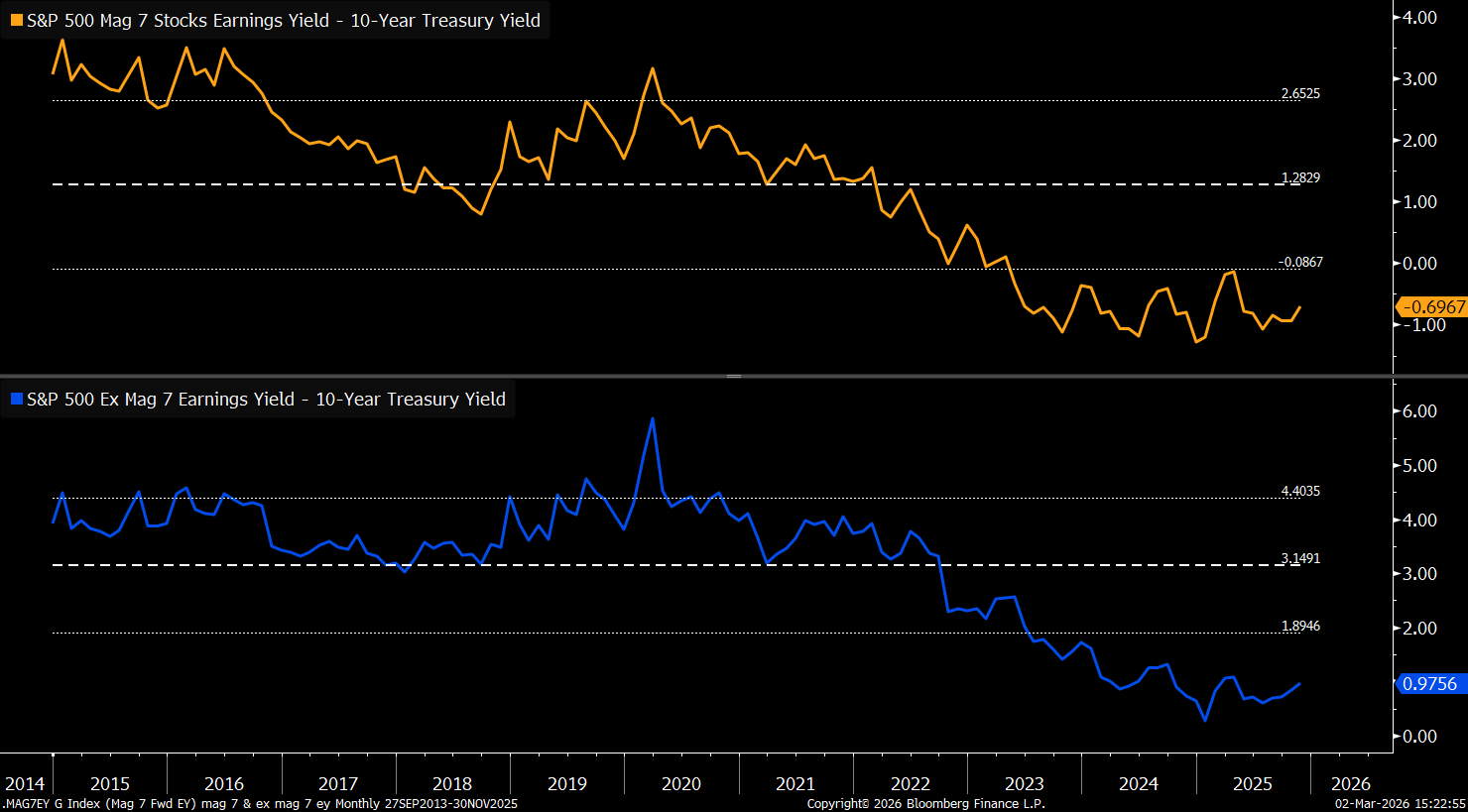

The more important thing to note on the public market side is that the entire earnings yield for Mag7 is negative relative to the S&P 500 Ex Mag7.

This is why the SPY/RSP ratio has been collapsing, because the earnings yield differentials are fairly extreme right now.

The implication BEHIND these moving parts is that the underlying factors are converging and cross-collateralizing in new ways.

So what rules are changing and how does this connect to the credit cycle?

There has been a very simple accounting mechanism that supported the flows into markets over the last 20 years:

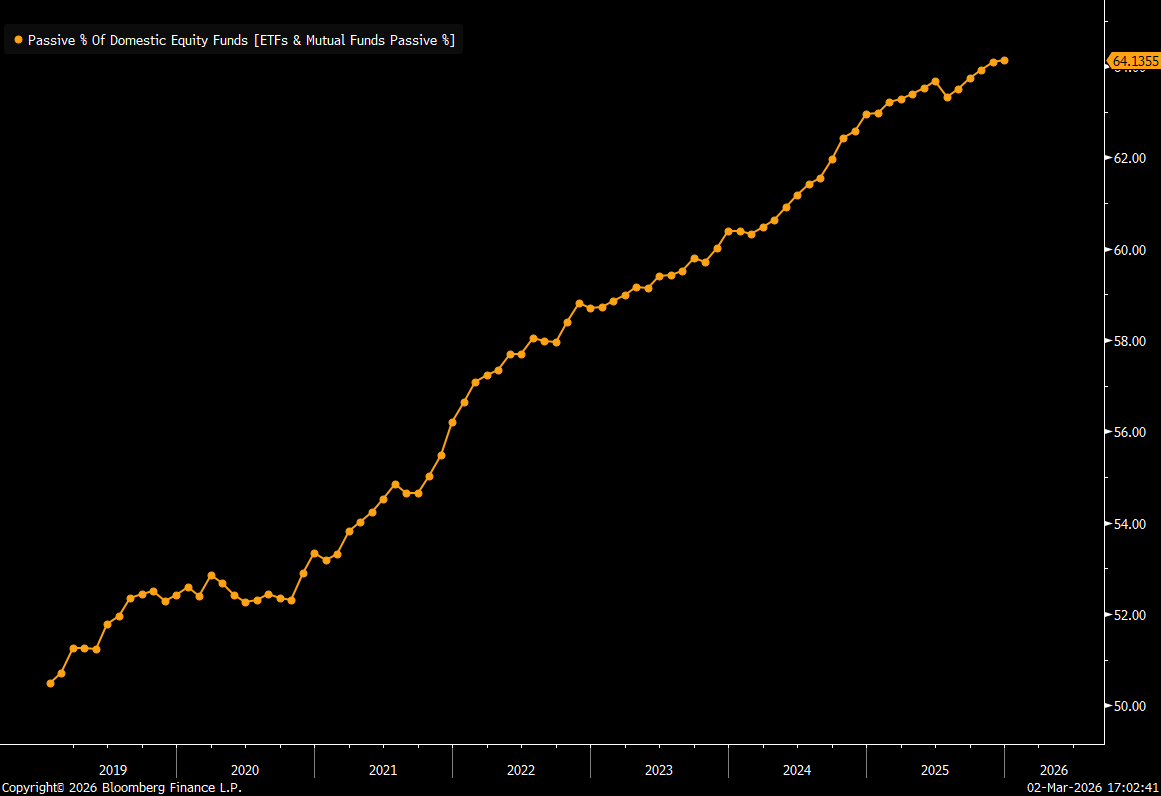

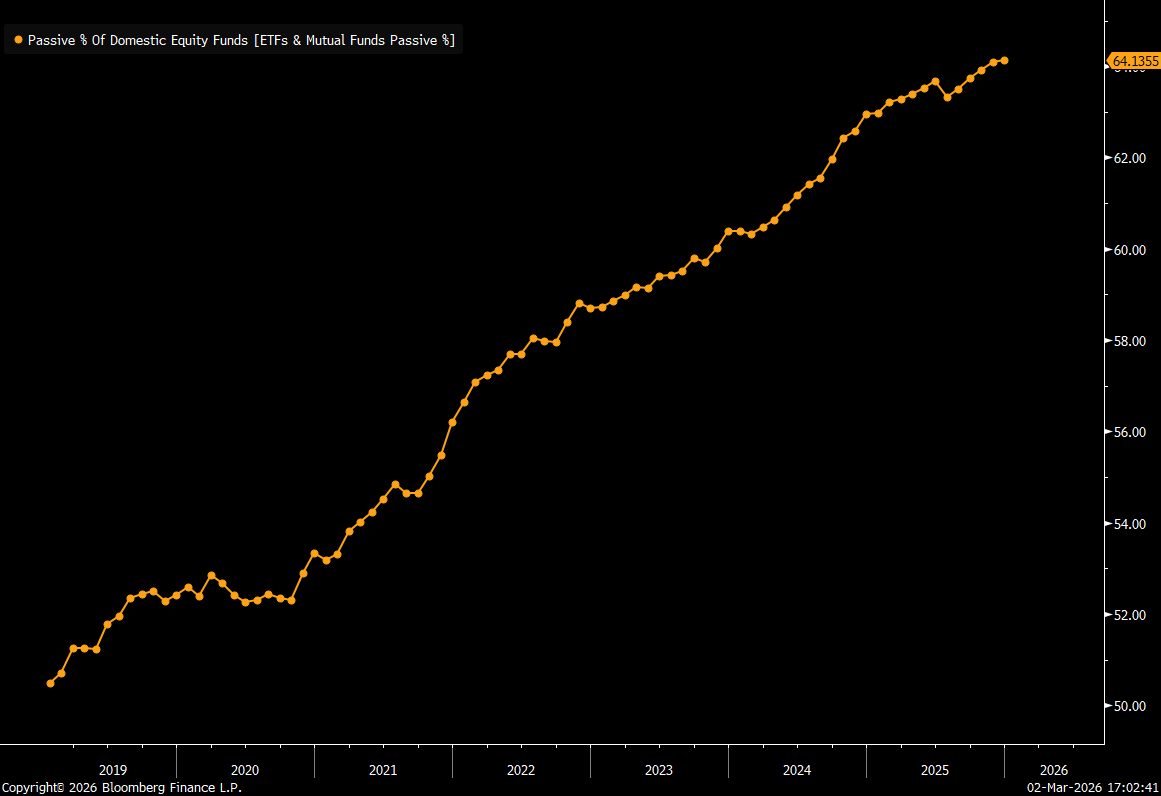

Passive flows come from the incomes of everyday people. As people make more income, some of this goes into 401ks and this capital indiscriminately buys the index. It’s an amazing source of liquidity into the greatest companies in the world

Cross-border flows from foreigners. When another country wants to do business with people in the US, they give them goods or services for dollars. If I want to import a bunch of clothes to resell, I need to calculate how much it would cost for me to produce them, and as long as I can import them cheaper than making them here in the US, I give dollars to foreigners who make my goods for me. Here is the thing though: those foreigners who have those dollars end up with A TON left over that they need to put into dollar-denominated assets. So foreigners buy bonds and stocks, which they have been doing for decades ever since globalization exploded. The problem is: what begins to happen when my goods become exponentially cheaper to produce in the United States? I begin to invest in a manufacturing facility here and then begin producing here. In the past, this would mean more manufacturing jobs would get added to the United States, but the problem now is: what if I switch from importing goods to manufacturing them in the United States with robotics supercharged with AI? The foreigners will no longer have the surplus of dollars to funnel into US equities, and I’m not hiring new people who will get income and have part of their income go into passive flows.

So in many ways, the efficiency from AI is sowing the seed for a significant risk. This is why I think the recent clip by Friedberg was so good in touching on the meta behind this larger issue. If you are driving productivity, will we end up having way more stuff than we consume? And then if we shift to a new type of system, will this begin to change HOW capital flows through the system for the channels of macro liquidity and credit?

https://x.com/theallinpod/status/2028504746303054039?s=20

You can see that the presence of AI is in many ways sowing the seeds for dramatic change in a very fragile system. When you churn the entire labor market and shock the system of global trade with geopolitical events, as equities are at all-time highs, it brings into question: WHO is going to be the marginal buyer of equities moving forward?

If the United States is facing these risks, every other country is facing even GREATER risks, especially given how complacent foreigners have become with hedging their FX risk (see the report I wrote here on this risk: LINK)

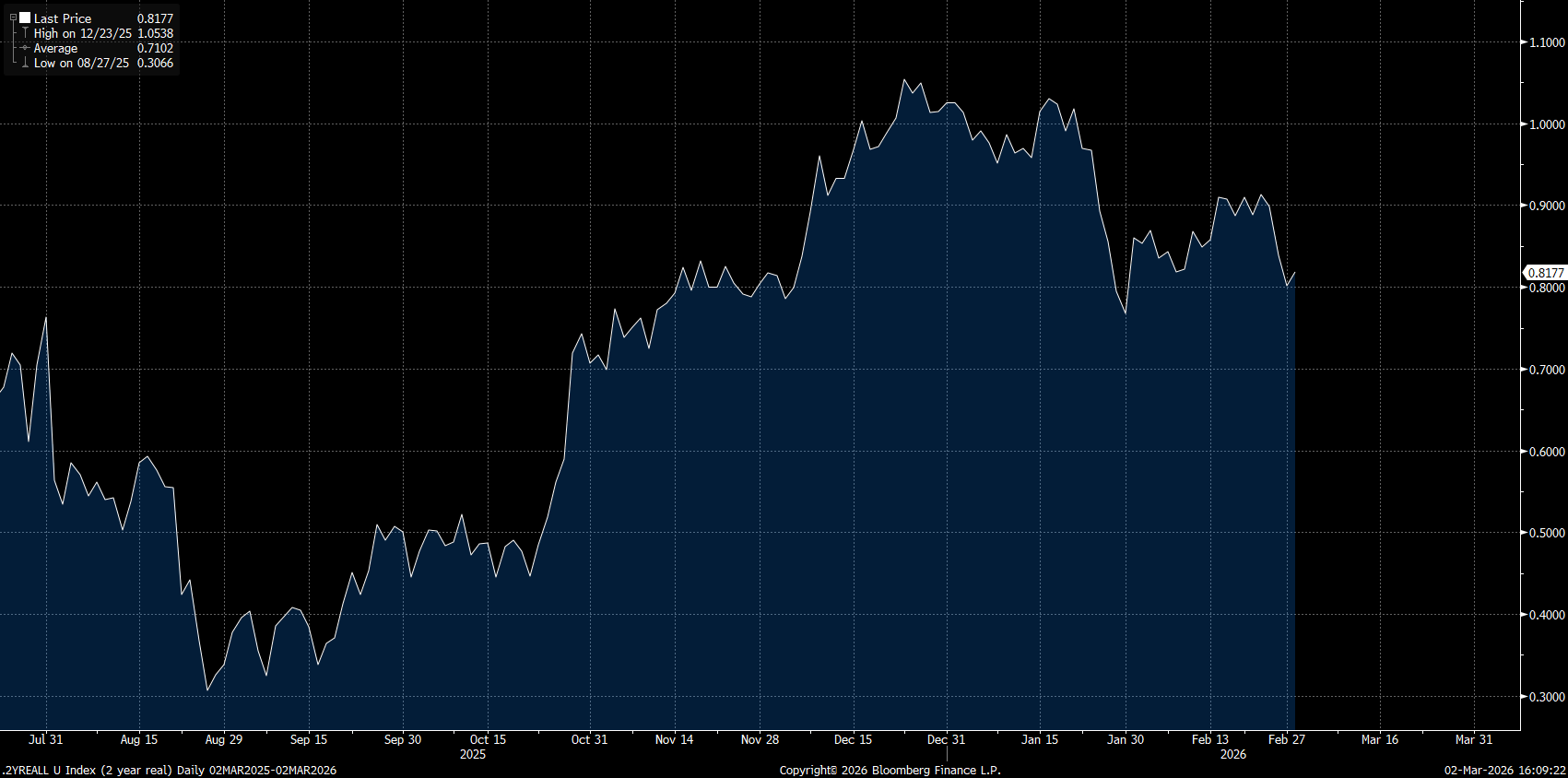

My entire point here is NOT to say we are moving into an imminent market correction. On the contrary, I believe the fall in real rates will continue after Kevin Warsh becomes the next Fed chair, and the amount of complacency we are seeing in positioning is way too bearish for me to begin betting on the beginning of a bear market.

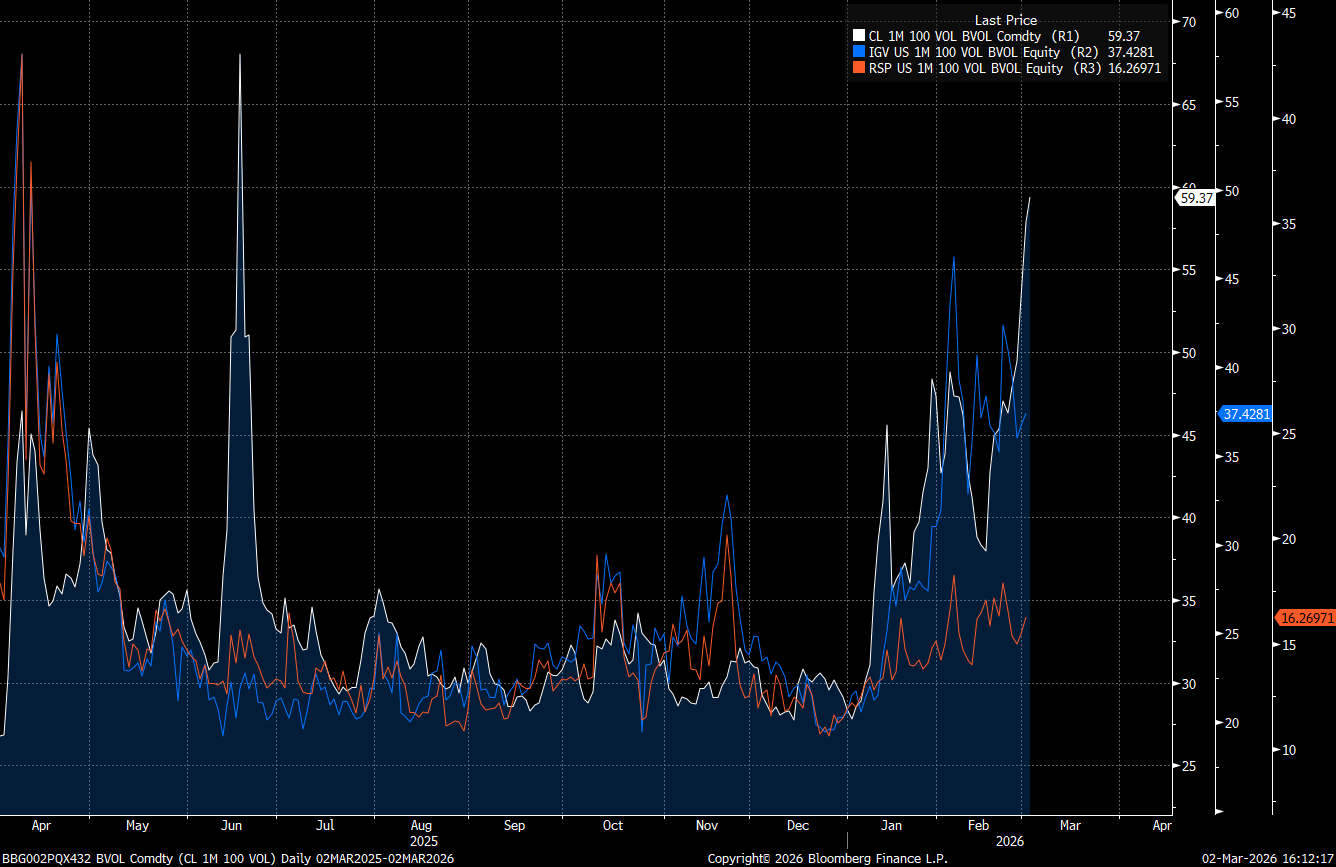

When you have volatility blown out this much in crude and the software sector (IGV) relative to the broad equal-weighted index of the market (orange), it shows how much risk premia exists in the market.

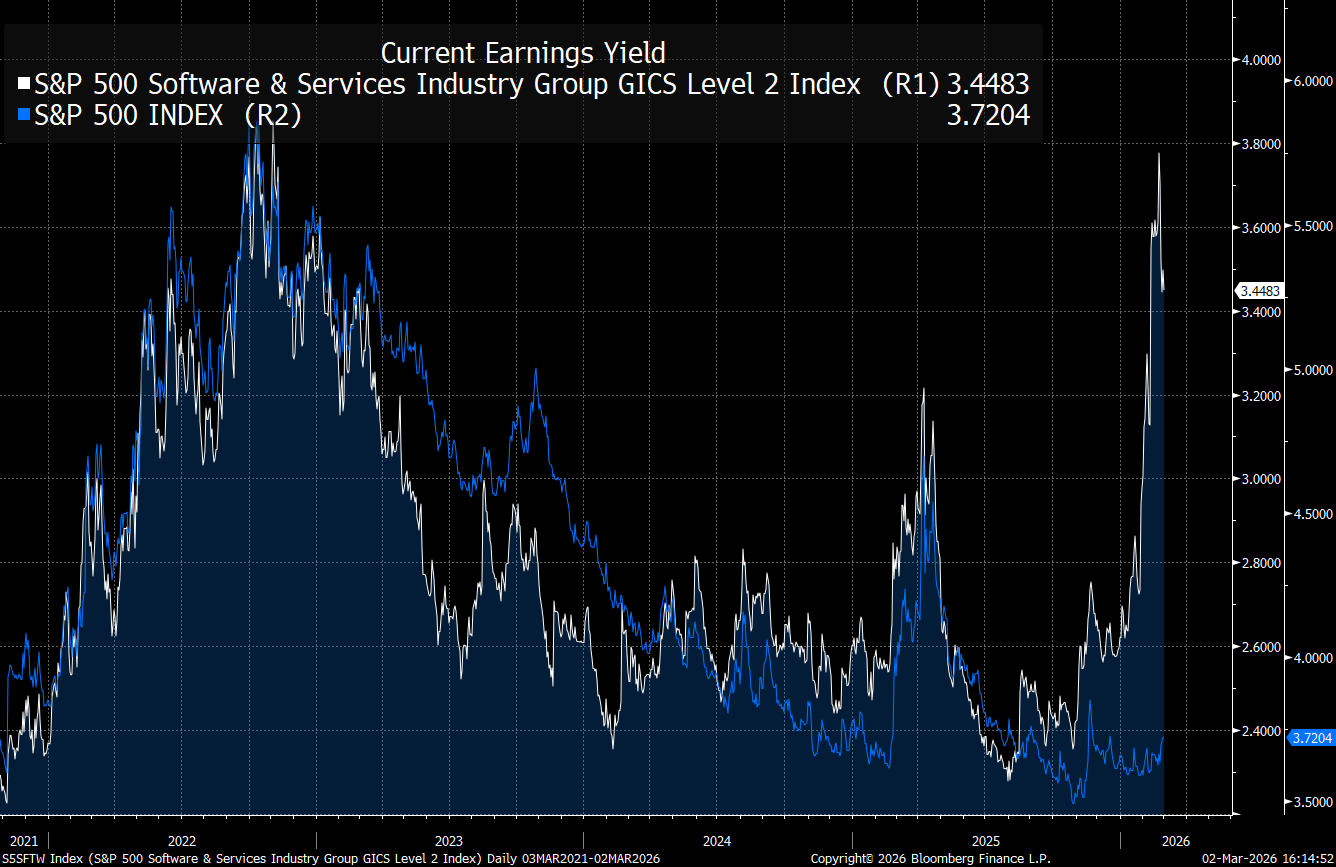

The current earnings yield of the software sector has made a massive deviation away from the earnings yield of the S&P 500 and is functionally pricing in the same level of risk that we saw in 2022 when everyone thought we were going to go into an imminent recession.

The best part about this is that people are only just beginning to realize that the data all these software companies have is going to become the new form of oil in the world we are moving into. Larry Ellison had a great clip on this where he talked about this fact:

https://x.com/Globalflows/status/2028505267810492898?s=20

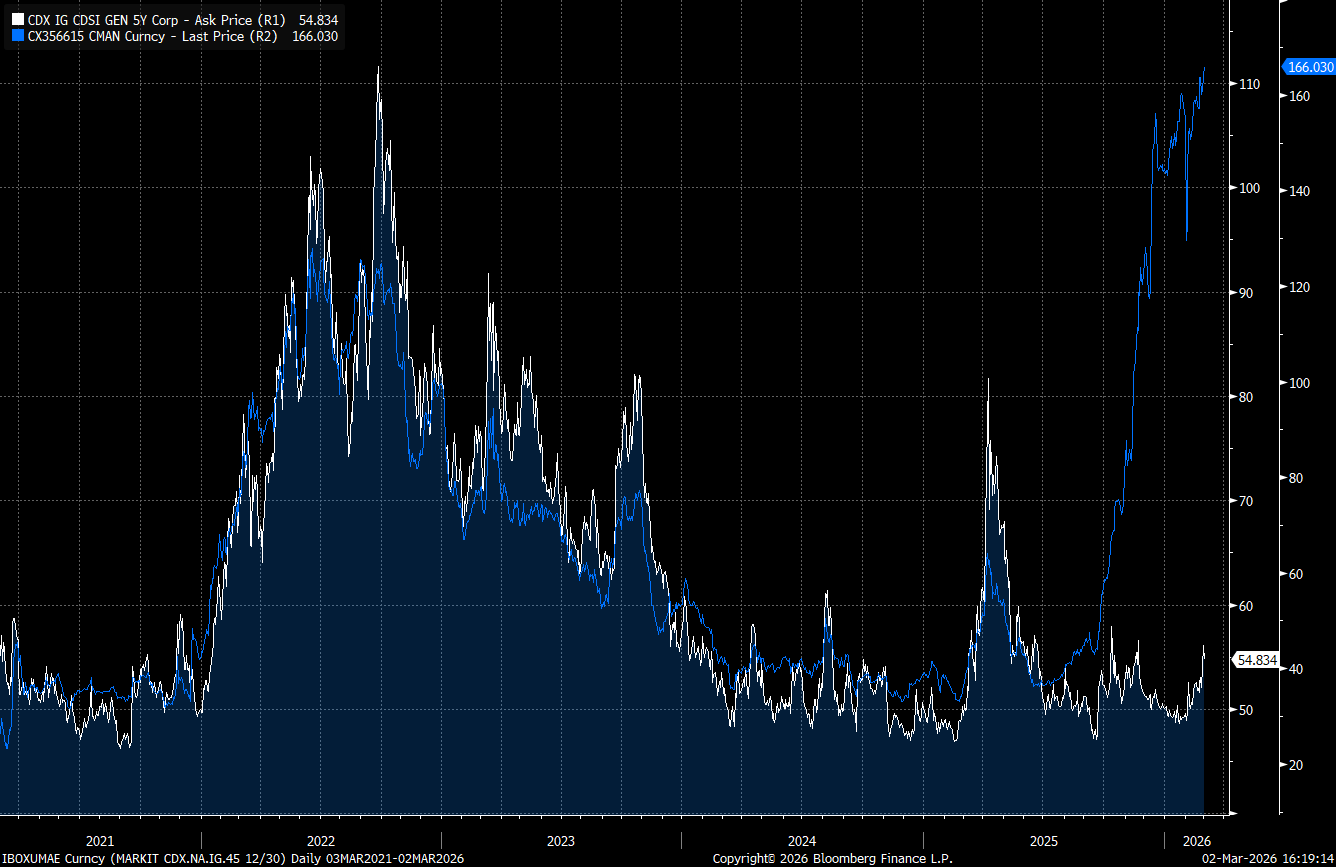

It is literally insane that the market is pricing default risk HIGHER than 2022 in names like Oracle, which are positioning themselves to be the primary beneficiary of the disruption AI is causing. I firmly believe that in the same way consensus was wrong in 2022 that a recession would materialize and crash the stock market further, we will see people begin to realize the absurdity of “software” being dead and we will move into a new narrative where “data is the new oil.”

See my report on Oracle here:

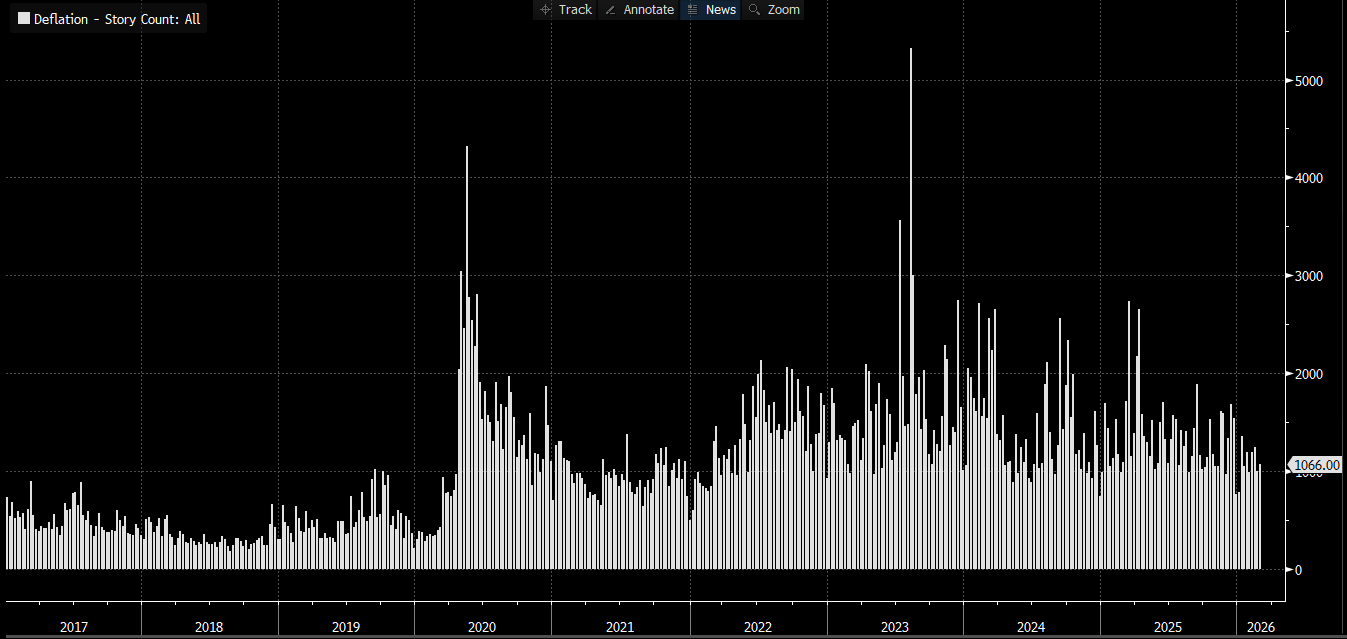

I will leave you with this final point. Ever since we entered the new era of social media converging with markets in 2020, there has been an excessive and reductionistic focus on recession. The story count for “deflation” and “recession” is now at an elevated level relative to history. There is so much focus on fear, which only clouds people’s judgment.

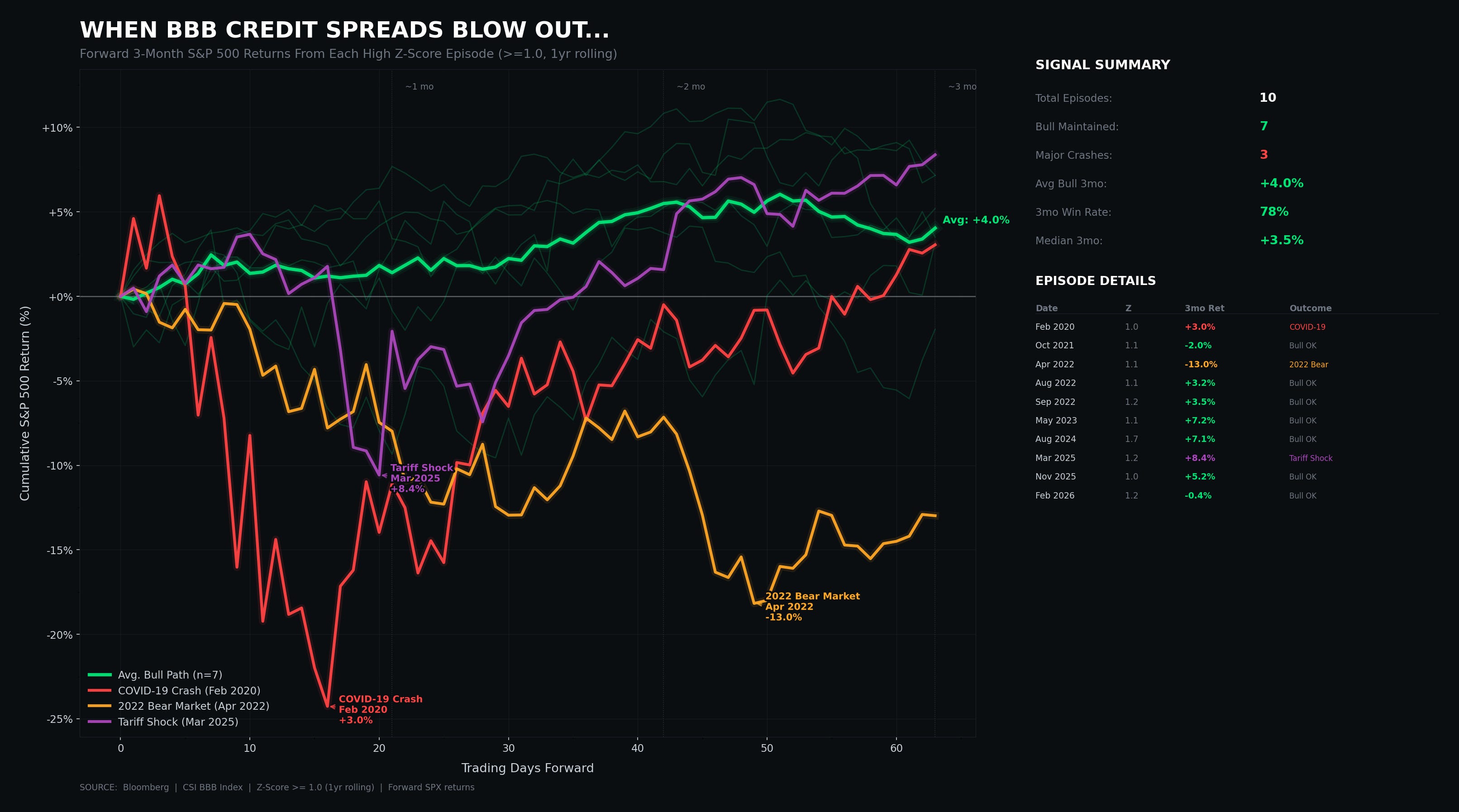

During this period of excessive fear-mongering, we continued to see equities resume higher after any marginal stress occurred in credit spreads. The Covid crash, tariff shock, and 2022 bear market were the most aggressive drawdowns, but even those turned positive on a short-term horizon.

Focus on the disrupters in the market, because when dispersion and rotation occur, taking advantage of these opportunities is the primary way to generate exceptional returns.

I laid out all my current market views here:

The information on this website/Substack is for information purposes only. It is believed to be reliable, but Capital Flows does not warrant its completeness or accuracy. The information on the website/Substack is not intended as an offer or solicitation for the purchase of stock or any financial instrument. The information and materials contained in these pages and the terms, conditions and descriptions that appear, are subject to change without notice. Unauthorized use of Capital Flows websites and systems including but not limited to data scraping, unauthorized entry into Capital Flows systems, misuse of passwords, or misuse of any information posted on a site is strictly prohibited. Your eligibility for particular services is subject to final determination by Capital Flows and/or its affiliates. Investment services are not bank deposits or insured by the FDIC or other entity and are subject to investment risks, including possible loss of principal amount invested. Your use of any information which is proprietary to Capital Flows or a third-party information provider shall only be used on individual devices without any right to redistribute, upload, export, copy, or otherwise transfer the information to any centralized interdepartmental or shared device, directory, database or other repository nor to otherwise make it available to any other entity/person/third party, without the prior written consent of Capital Flows.

Fully agree with the thesis here over the long run for sure, but to your point, we melt up first imo. Not many people are talking about the geopolitical tensions of this too...e.g what happens to the Indian Services sector of which 70% is made up of IT Services / Outsourcing (makes up about 50-55% of Indian GDP) > what is the impact downstream on some of the social tensions between Pakistan and India?

The credit cycle / AI cross-collateralization point is the thing most thematic investors in this space are under-weighting. It's not just that Mag7 earnings yields are negative vs. S&P ex-Mag7. It's that the foreign capital flow engine funding those multiples (globalization surpluses recycled into US equities) is being eroded by the same AI efficiency the market is pricing in. That's a structural feedback loop, not a cyclical wobble. The counter-argument worth stress-testing: the equipment and infrastructure layer of the AI supply chain (TSMC, ASML, AMAT) is still being driven by a multi-year capex commitment cycle with locked-in orders, meaning even if demand softens at the application layer, the equipment layer has 12–18 months of forward visibility baked in. Does the credit cycle risk you're describing hit the platform layer (NVDA, hyperscalers) before or after it hits the enabler layer?