The Research HUB: FX Primer, Pt 2

The primer for understanding and trading FX

Hey everyone,

This is part 2 of the FX primer. Here is the initial breakdown of the 5 part series:

5-Part FX Primer Breakdown:

Part 1: FX - Resources, The Big Picture, Variables, Aggregating Knowledge, and Essential Tools.

Part 2: FX - Synthesizing Information from Part 1: Theory, Practice, Causal Mechanics vs. Regression Analysis.

Part 3: Delving into Historical Case Studies: The Importance of Studying History, Continuity vs. Discontinuity, and the Challenges of Backtesting in FX.

Part 4: Examining the Current Environment.

Part 5: Integrating Knowledge: Top-Down and Bottom-Up Analysis, Attribution Analysis, the Expectations vs. Actual Matrix, and Quantitative Models.

Be sure to read Part 1 here:

The Research HUB: FX Primer, Pt 1

Hey everyone, This article will serve as Part 1 of a 5-part series, acting as an FX primer. For those interested, I've previously written primers on both the S&P500 (link) and the bond market (link). If you have spent any time at all in FX markets, you know that sometimes a move makes total sense, and then the next move makes zero sense. On top of that, FX isn’t like equities where it just always (theoretically ;) ) goes up and to the right!

In part 2, we will be building the interpretive framework that will function as a foundation for our analysis. This will be an important one!

Intro:

There are several ideas I am going to lay out about this process:

The Problem With Compounding Knowledge and Communication:

Part of the difficulty in education is that we are all at different levels of our knowledge and experience. However, in order to communicate productively, there needs to be some shared presuppositions about how things work. A lot of the ideas I am going to cover in this article will only really make sense if you have a decent grasp of the first article (link) and all of the articles/books referenced there. This will especially be important when we talk about data on multiple time horizons and “netting out” accounts that balance. For example, a balance sheet has to balance. The balance of payments has to balance.

Causality:

The difficulty with talking about causality is that there are so many dynamic inputs. For the purpose of education and communication, we will often say, "let’s assume all things remain constant and this one variable moves; the outcome would be x." This is a helpful communication and learning tool, but in practice, the world doesn’t work that way. This is key to remember. Theory is very important, but it will only get you so far in the real world of complex systems.

Econometric Models:

Ever since it became cool to bash economists, there is a large number of people who think econometric models are worthless. In my mind, when I build a model, there is an intended range of implications that I can make with it. Attempting to make conclusions outside the range of a model doesn't mean the model is broken; it means you’re broken. ;)

Money:

The final idea that will transition us into some FX concepts is that “all money that is anywhere comes from somewhere.” This has become a very popular idea in macro circles and for very good reason. The main idea is that there are always sources and uses for money. At the end of the day, capital flows always balance, even if we have difficulty quantifying and predicting them. This is a key qualifier for markets because even though we can roughly quantify moving parts that net out, we are still operating under the Heisenberg principle of uncertainty.

Synthesizing Information from Part 1:

Let’s first start by expanding on several ideas from Part 1:

1st quote:

To truly understand FX, you basically need to understand everything else. FX is kind of like the meta asset because it’s connected to every other asset.

A country is similar to a company in that it has a balance sheet and an income statement. A currency is the conduit through which you can access the goods or assets of a country. In a sense (with many qualifications), a currency is like equity in a country. The thing is, you need to know the overall “value” of a country’s underlying goods and assets. Just as Amazon has many different branches that generate revenue, a country has many different parts that would attract capital or constrain someone to purchase the currency. Just as you can’t extrapolate the AWS portion of Amazon to the entire company, you can’t extrapolate a single part of GDP or a single asset to the whole.

What we need to do is break down every variable of a country, see how it contributes to the whole, and then connect it to the currency.

2nd quote:

An FX pair is the expression of the GIP differential between two countries.

Several points expanding on this idea:

The ideas of growth, inflation, and policy (or liquidity) are now very clear in financial education. The GIP of a country determines the top-down returns of all assets.

A country’s GIP connects to other countries via the balance of payments. This already makes intuitive sense if you understand the components of GDP. There are import and export line items in GDP. What you need to do is understand how the balance of payments connects with both the balance sheet and income statement of a country. A good place to start with this is the IMF balance sheet manual (link) and the book I originally recommended by Michael Pettis, "Trade Wars are Class Wars" (link).

The goal is to identify the relative GIP between countries and quantify this through the balance of payments via the capital account and current account. The way to form views on a currency is through the quantification process of looking at the relative GIP as it's transmitted through the balance of payments. Remember, GIP accounts for the returns and risk premia of the assets in a country. You then want to compare these returns/risk premias with the other country. The difficulty with this is that the underlying structure of the economy generating returns is always dynamically changing. For example, in each FX regime, there is usually a different underlying contribution to GDP and the returns (as well as market capitalization) of assets. This is why you need to quantify the underlying macro landscape and then connect it to the BoP.

So how do we tangibly connect these ideas together? That is what brings us to the next section.

Theory:

If you want a really good breakdown of how to quantify all of these moving parts, I would direct you back to the book I recommended by Adam S. Iqbal. Adam provides many of the calculations that are helpful.

However, from a big-picture perspective, once you have the moving parts together, you'll want to accomplish two things: 1) define the risk-reward of the actual situation and 2) understand how the market is pricing the risk-reward.

Risk Premiums and Returns

“Changes in the risk premium are the primary driver of price movements in FX and other asset markets and are therefore more important in understanding market price movements than changes in macroeconomic variables, such as the expected real exchange rate, expected inflation, the balance of payments, interest rate differentials and the remaining plethora of factors that are cited in FX analysis.”

Adam Iqbal made an excellent point about returns and risk premiums being the primary drivers of price movements in FX. However, the question is: what drives these risk premiums? This is where connecting all of these underlying factors, like macroeconomic data, to asset markets become valuable.

When I think about risk premiums in the context of currencies, I always view them as connected to the risk premiums of other assets in the country. For example, if there is a negative carry on a currency, there is likely a good reason connected to how capital is shifting across the risk curve in domestic assets.

Main idea: returns and risk premiums are connected to GIP. These returns, risk premiums, and GIP are transmitted through the BoP.

This goes back to the idea I mentioned above about relative returns produced by relative GIPs in a country. Part of the question is: how do we quantify this? Well, fundamentally, the returns are going to be reflected somewhere. What we would need to do is understand how relative risk premiums and their changes connect to the FX forwards and FX spot.

FX Forwards and Spot

If you don’t have a Bloomberg, the FX Swap monitor on CME is really helpful: https://www.cmegroup.com/trading/fx/cme-fx-swap-rate-monitor.html

When we begin to get into the FX forward market, we need to understand covered interest rate parity and uncovered interest rate parity.

I introduce two concepts that are central to understanding movements in FX markets. The first, covered interest parity (CIP), is arguably the most important concept for FX market participants to understand. It relates the forward exchange rate to the spot exchange rate through the foreign and domestic interest rate. Second, I discuss uncovered interest parity (UIP) and the carry trade. UIP conjectures that the forward exchange rate reflects the market’s expectation of the future spot exchange rate. I apply the asset pricing model of Chapter 1 to show that UIP should not hold in general and that the risk premium is the difference between the expected future spot rate and the forward exchange rate. I derive the relationship between UIP and the well known FX carry trade to show that the expected profits from the carry trade come from risk premium in currencies. Also, I distinguish between the concept of FX carry, which represents a type of buffer against adverse movements in the FX rate, and the expected profits from carry trading.

Covered Interest Rate Parity:

Forward contracts provide the basic building block of the CIP relationship. A forward contract sets the price today at which an investor will buy (or sell) a currency at a date in the future. CIP says that this price depends on the current spot price, and the interest rate differential between the currencies.

The carry trade:

The carry trade typically attempts to profit by borrowing in low interest rate currencies and investing in high interest rate currencies. This is equivalent to trading a forward contract, and then unwinding the delivered spot in the FX market upon delivery.

The main idea behind understanding FX spot, FX forwards, CIP, and UIP is that we are attempting to quantify how risk premiums are expressing themselves at a point in time and how they are priced into the future. Since our view of the future is always in dynamic flux, both the spot and forwards are constantly moving to price probable outcomes.

I am trying to keep things simple here because there can be a lot of complex math surrounding the quantification of these forwards. Fundamentally, however, when you begin to understand what drives an FX move, you will start to think about correlations and macroeconomic data differently.

For example, real rate differentials take on greater significance when you understand how they connect with forwards. Here is a chart of the TIP/WIP ratio with DXY overlaid. It's not the best way to express the real rate differential, but if you don’t have a Bloomberg, it can be a helpful tool.

The key thing, though, is that returns across markets can change. We will actually begin digging into this in the next article. Other countries don’t have the same asset and liability makeup as the US, which means if you are basing your understanding of FX on a single example (the US), it will be incredibly difficult to transition that skill set.

Macroeconomic Varaibles:

Alright, so we have this idea of returns and risk premiums driving FX.

When we talk about the underlying economic data and modeling it as it connects with risk premiums, there is a very specific way to do it. What you need to do is connect 3 major things: GIP differentials, the balance of payments, and the impossible trinity.

There are a lot of narratives out there that very specific events always cause specific FX moves. For example, people will say government spending or a specific central bank policy causes the devaluing of FX. The problem with these blanket narratives is that people never quantify how much government spending is taking place and how it contributes to GDP or is transmitted through the balance of payments.

You always need to quantify it. You can accomplish this simply by breaking down the line items of the country’s balance sheet (see NIPA data for the US) and income statement (see GDP and GDI). This quantifies variables and their actual contribution to the whole.

Once you begin to understand the underlying flows in the economy, their transmission through the current account and capital account will make more sense. The net effect will be how the financial account reflects the net holdings.

The BOP accounts record the economic transactions that a country makes with the rest of the world during a period of time. Before diving into the detail, let us study a simple example of international trade that highlights two of its most important components, namely the current account, and the financial account and their interrelationship.1 The key intuition is that the current account logs net exports, such as transactions in goods and services, and the financial account logs capital flows, such as transactions in stocks and bonds, and that the current account and financial account are approximately equal to each other.

In a previous article I wrote, I went over GIP path dependencies. These will be key ideas because preconditions in GIP set the probabilities for risk premiums in assets and FX:

Macro Report/Insights: GIP Path Dependencies

Hey everyone, As I have emphasized over and over…….. In the information age, you simply need to be at the right place, at the right time, with the right information to succeed All of us have access to the same data, the same market, and the same resources. Sure some people have fancy tools but on the whole, we all operate under the same uncertainty.

Fundamentally, we want to bring together all of these moving parts in the underlying economic data and net them out so we can see offsetting relationships. Then we can begin to define the probable outcomes of the underlying situation given the preconditions that exist. From here, we can compare this to how the market is pricing the path and destination, which begins to create opportunities for us to trade.

A lot of times, all you need to find is a mispricing or unrealistic expectation of the market and take the other side. Many times, you don't even need to know the exact outcome of the actual situation.

Practice:

Let’s talk about a few practical things:

We know the goal is defining R:R in the underlying situation and how the market is pricing that R:R. A really important thing to do here is to quantify these R:R on multiple time periods. For example, using 1st, 2nd, and 3rd derivatives to begin quantifying economic data. This allows your view to incrementally be confirmed or falsified.

When looking at data, always think about how the various combinations set the preconditions for the next step. As I laid out in my macro report (link), both the path and destination are important. Fundamentally, the future is always a function of the present.

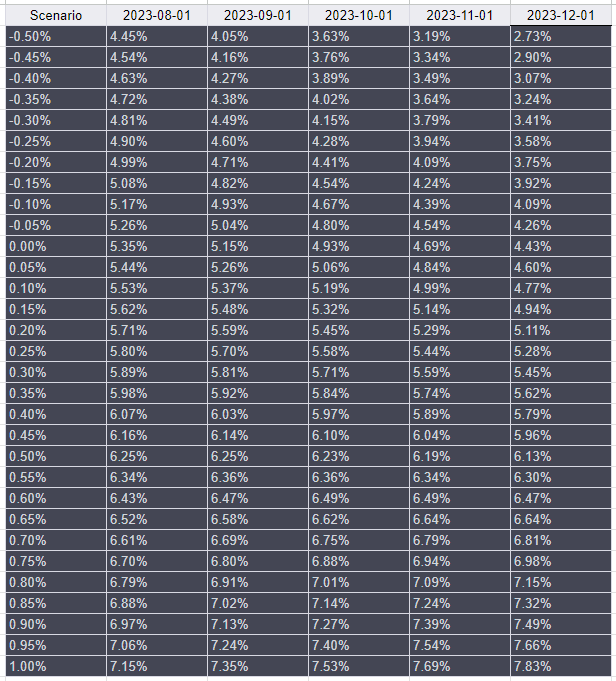

As I mentioned above, many times you simply want to identify an extreme that is unrealistic and fade it. An example of this is how I explained inflation scenarios in the macro report (link). Here was the table I shared. Basically, all you have to do for this is take the YoY numbers, input them into ChatGPT, and then ask it to take the MoM speed and extrapolate that current speed of deceleration to the next 6 months.

The thing is, I don’t need to know where a specific economic data point will be in 6 months. All I need to know is that it's incredibly unlikely for it to be where the market is currently pricing it to be.

Obviously, these are all extrapolations, but the speed of change connects to amplitude and duration. If x speed is maintained, where will we be at y time? In reality, there are much more sophisticated ways of running these types of economic models, but these are a great starting point just to frame the big picture. Once you begin to run these types of analyses across all the variables that have been laid out above, the picture will become much clearer.

Causal Mechanics vs. Regression Analysis:

Let’s begin to wrap up with one final thought:

I remember a while back someone said to me, “Oh no, you can never understand the drivers of FX. I have run regressions with every possible combination and there isn't consistency.” Well, yeah, obviously! The whole point is that you need a logical framework for identifying how the causal drivers change!

In my mind, any type of correlation or regression in FX is bound temporally. I run correlations or regressions to function as a test or reflection of my other models. If I am seeing a specific correlation that is not in confluence with the R:R that my FX model is indicating, then it is likely I am not understanding the situation.

Regressions are reflections!

Additional Resources:

There are several Twitter Spaces where Prometheus and Myself discuss a lot of these economic concepts:

Most recent:

Older Convos:

All of the BoP data and information can be found on the IMF website:

The BIS has a lot of excellent papers breaking down international flows, the balance of payments, and the issues facing us today. I found these papers specifically helpful:

Conclusions:

As you dig into each of these parts more, you will realize it's not just about knowing the parts; it's about how you bring them together that creates alpha. As you can see, there is a significant amount of complexity surrounding FX. Many people only use momentum scores or simple spreads to generate views. This creates opportunity for those who truly understand the underlying dynamics.

On top of this, remember, FX isn't just about trading. FX impacts everything, so if you have specialized knowledge in this field, you could work for any company that needs to manage its FX exposure.

I truly enjoy the challenge of FX because the value of your analysis is made explicit:

In the information age, you simply need to be at the right place, at the right time, with the right information to succeed

Part 3 will be coming soon!

Thanks for reading!

Thanks for this. awesome primer ! I do have a question. How do you align the understanding/direction of BOP into the timeframe at which you're trading? It seems these short-medium term moves, 1 week to a 2 months are driven by events(market expectations of monetary policy, geopolitics, rates).

Is the BoP more long term, say 6 months-1year?

Sometimes it seems like a currency can deviate from having positive BoP due to the short term catalysts. Maybe I am misunderstanding. Thank you in advance💪🏽

Another great article! I’m gonna re-read it

several times, so much info to absorb. The king of alpha sharing keeps going 🔥