Alpha Report: Macro Inflection In Interest Rates

How high can interest rates move between now and the end of December?

Since the 1980s, there has been a structural downtrend in interest rates. This has quite literally shaped the entire financial industry on an international basis.

Why does this even matter? Because trends like this shape entire generations of people and how they think about the world. The macro context for WHERE we are and WHY interest rates are important have been laid out in recent reports/podcasts:

Recent podcast explaining the current cyclical context: Macro Podcast: The Inflection Point For Interest Rates

Podcast: How Interest Rates Shape The Rise And Fall Of Nations

Educational Primers:

Structure Of Report:

Today, we are going to dig deeper and precisely show the following for interest rates:

What is the cyclical skew of interest rates?

How are the forward curve and positioning changing shifting the risk-reward of interest rates?

What is the actual risk of inflation reaccelerating and how should we monitor this correctly?

How are interest rates impacting each sector including equities, credit risk, and the real estate market?

What is the best way to manage risk and redundancy plan moving forward?

Announcement Reminder:

I want to remind everyone that TODAY is the last day to lock in the current price for the Substack before there is a price increase. All of the details for this have been laid out here: Link.

You can start a free trial on the Substack and pay nothing to review all of the research I have provided (this means you have zero downside and unlimited upside).

Everyone who is currently a Paid Subscriber has access to all of the in-depth macro research and trades at the current price ($80/month or $960/year). This price will never change for you. In order to continue future innovation and improve the quality of research, the price for new subscribers will increase.

This price will be increasing to $90/month or $1,080/year on Friday, November 22nd. If you subscribe BEFORE then, you will lock in the lower price ($80/month or $960/year) and never pay more than this. If you are here early and long the Capital Flows Substack, then you get to lock in the lower price for all the future upside.

What is the cyclical skew of interest rates?

The current context for macro has been laid out in the following reports:

We are going to build on these ideas and further refine the specific analysis and implications for interest rates and how they are impacting financial assets.

Big picture, we are operating between cyclical tensions where nominal growth is clearly higher but inflation is decelerating as the economy normalizes and interest rates are at a higher level. This creates a cyclical tension in interest rates where we are unlikely to break to new highs (above 2023 levels) but a strong move back DOWN to the lower bound is not imminent.

Why is this the context? Because nominal GDP on a YoY basis remains squarely positive making it incredibly difficult for interest rates to move back to 2018-2020 levels. We are likely to remain in this type of macro environment for at least the next 18 months.

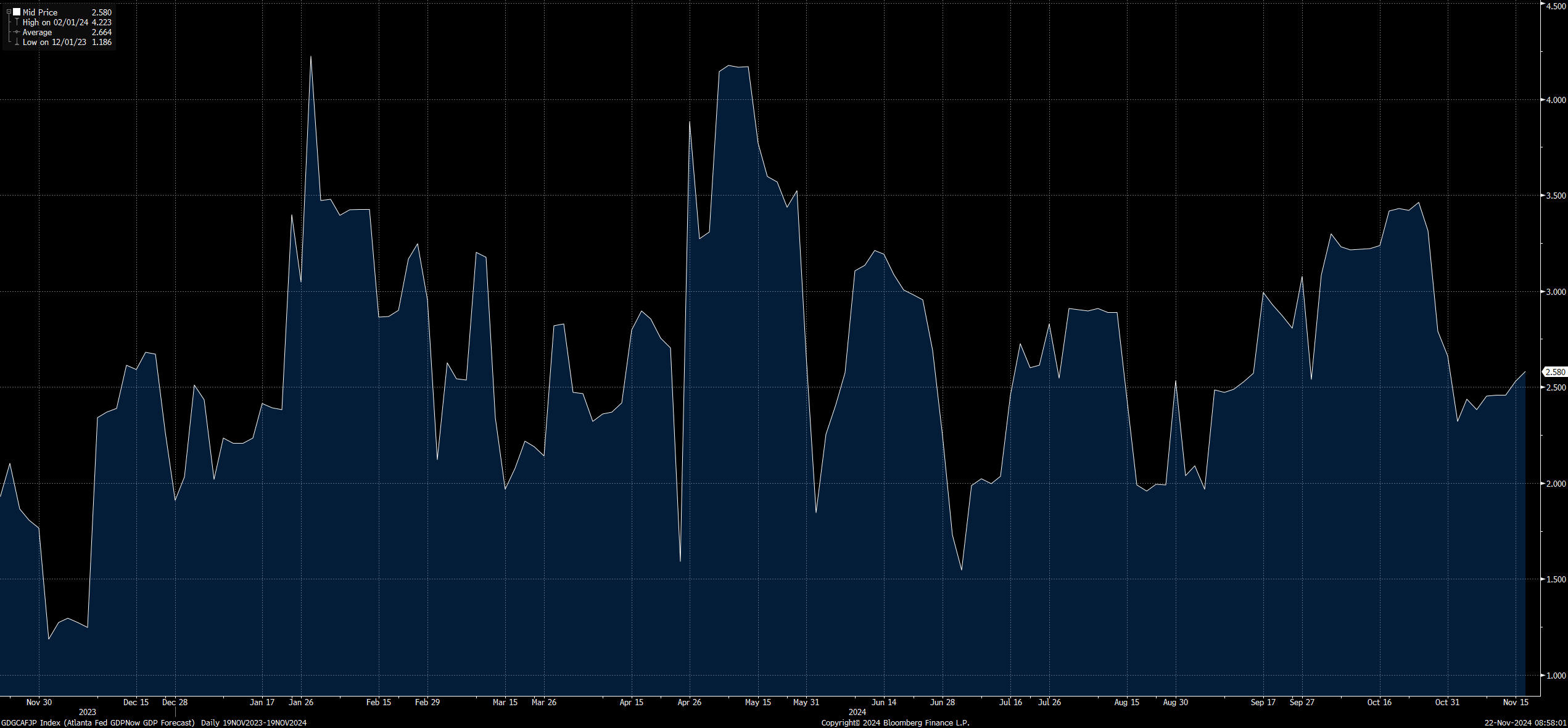

We can visualize these levels and understand that for rates to be considerably lower or even BELOW nominal growth, a recession must occur to “reset” inflationary forces in the economy.

Until metrics like the Atlanta Fed nowcast or initial claims begin showing clear signs of deterioration, a recession remains a low probability.

On the other side of the coin, the Fed continues to hold the Fed Funds rate ABOVE core CPI.

This dynamic of slowing the speed of rate cuts and increasing the speed of pauses naturally puts DOWNWARD pressure on inflation. The chart below shows the 2-year nominal rate and inflation swaps.

The implication behind the chart above is that as real rates remain elevated (nominal rates above inflation swaps), this will transmit into inflationary and growth pressures. The chart below is nominal rates minus inflation swaps overlayed with credit spreads (yellow). In other words, HOW MUCH is the higher real rates transmitting into growth and credit risk in the economy?

The more that higher interest rates transmit into growth, the lower the Fed can move real rates. This is where understanding the pricing of the forward curve and how it relates to these correlations is critical for the next 30 days in markets.

How are the forward curve and positioning changing shifting the risk-reward of interest rates?

Keep reading with a 7-day free trial

Subscribe to Capital Flows to keep reading this post and get 7 days of free access to the full post archives.