Interest Rates, Equities, and Bitcoin: Updates

The skew for assets within the macro regime

The primary way to differentiate yourself in markets and any domain of society is the quality of your thinking as its expressed in HOW you interpret the world. In public markets, we functionally all have the same data and information. If you have a Tradingview account and use the CME tool (link), you functionally have everything you need.

Every time there is an earnings release or data print, algos are waiting to pounce and price the new data. On top of this, tens of thousands of traders (maybe more?) are watching it closely to potentially execute trades. Just because you don’t think about the algos or individuals on the other side of your trade, doesn’t mean they don’t exist.

As myself and

laid out in the podcast, you need to find someone dumping their position to take the other side of. This is the entire goal of alpha generation!

If you aren’t constantly in the process of developing an informational edge where you have a significant advantage over other market participants, you’re failure is inevitable. This is why I constantly lay out things in the educational primers. Please reference the Macro Alpha Primers and respective podcasts that I have done thus far here:

Macro Alpha Primer: Credit Risk and Duration Risk and Macro Podcast: Macro Alpha Primer

Macro Alpha Primer: Correlations and Macro Podcast: Macro Alpha Primer

Macro Alpha Primer: Macro Catalysts, Hedging Pressure, and Positioning and Macro Podcast: Macro Alpha Primer

I have also laid out the macro views here:

Educational Point On Interest Rates:

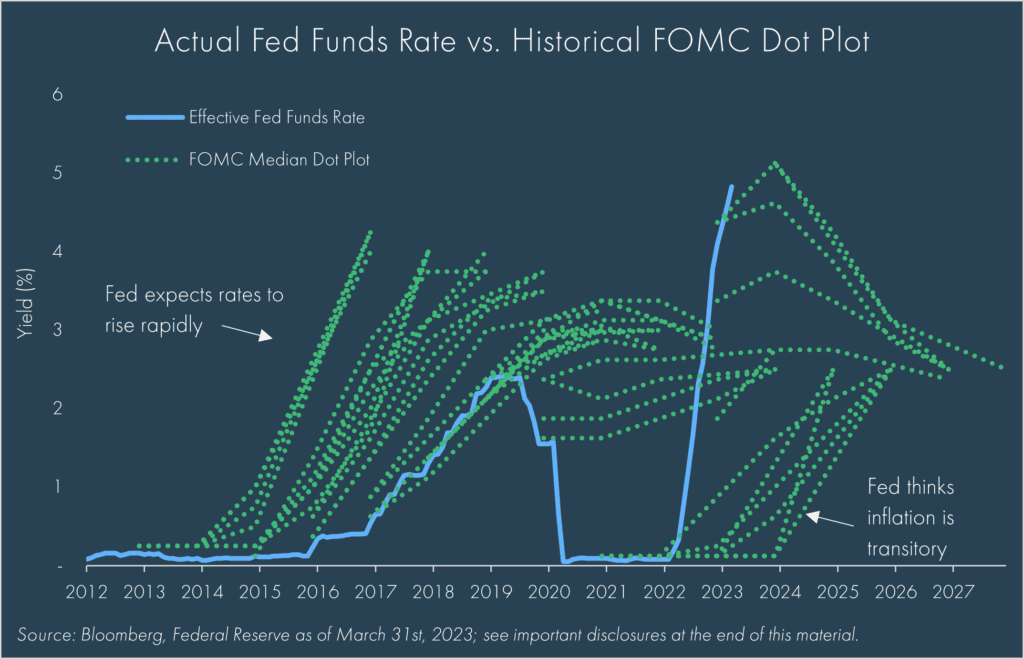

Before we get into the specific views I have laid out on interest rates and the trades I am running, I want to cover an educational point on interest rates and inflation (please see full interest rate primer here: Link). The market is ALWAYS in the process of warehousing the risk of future uncertainties. As a result, there is always an implied expectation about the future. The chart below shows 2 year inflation swaps (white) and the 2 year interest rates (blue). While these react to data prints in the present, they are fundamentally pricing a specific future in two years.

The following charts illustrate that the expected path of rates (by the Fed and market) vs what is realized is functionally ALWAYS incorrect (link).

There is always a spread between what is expected vs what is realized which is why opportunities to generate returns exist. It is important to remember that the market is a place where transactions between participants take place. When people say “the market is always right”, we arent implying that its expectation of the future will always be realized. This phrase is typically used when people make excuses for not aligning themself with the process of the market.

If by its nature, there is a large spread between what is expected and realized, how do we go about interpreting markets? THE RULE: Path dependency. This mindset is a huge shift from typical “business cycle” analysts. When people say the market moves in cycles, this information is equivalent to saying the Twin Towers fell because of gravity. Is it true? Yeah sure. Is it helpful and tell the full story? NO!

While we can look at the past and see historical oscillations in economic data, try comparing this to the expected and realized path priced by assets. Once you do this, you will begin to recognize that things are never as clear as they seem. On top of this dynamic, the implied expectation of the future is actually an input into the realized future. For example, if the market expects lower or higher interest rates in the future, it begins to price this and impact both the economy and financial assets.

There are a lot of moving parts here which is why I always encourage people to go through the educational primers I write. When you have the foundation of how the system works and a real-time synthesis of it, then you BEGIN to set the context for taking bets.

Let’s shift to real-time synthesis of macro. I will be covering the following topics:

How the data this past week fits into the macro regime I have laid out (see macro report here: Link)

How does this directly connect to the risk-reward and trades I am running in the rates space?

Why we have seen equities chop in a range since their rally off the August lows?

Where are we moving next with Bitcoin?

Macro Data:

We continue to see confirmation in the data that we are NOT in a recession. Notice that the real GDP data came in ABOVE expectations. Why does this matter? The macro bears who said we have been in a recession “under the surface” continue to have their view falsified. On top of this, initial claims continue to come in either in line with or below expectations.

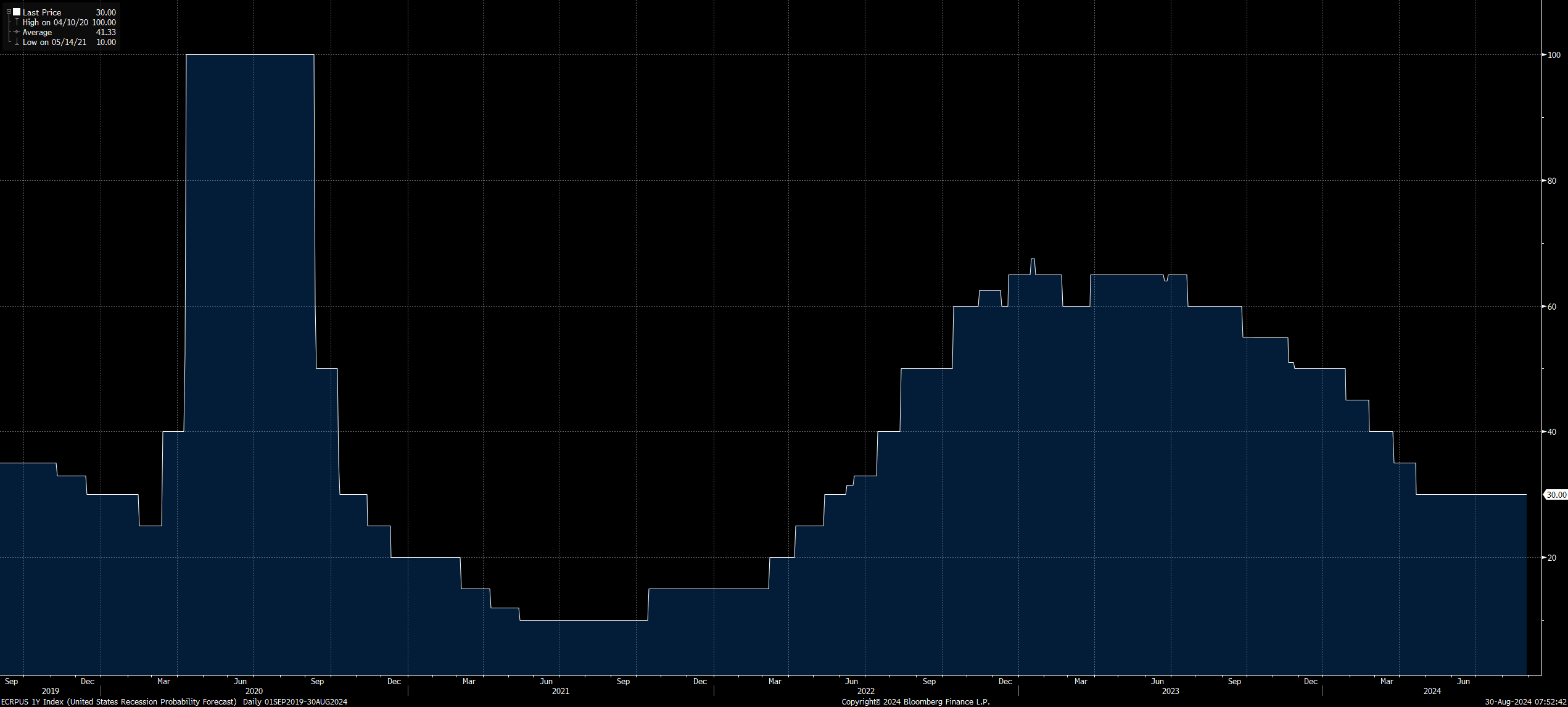

Economists still believe there is a 30% probability of a recession within the next year as well:

I have already laid out the context for how recession vs growth scares and how they get priced on the forward curve is going to function into the end of the year here:

Until we see a move up to 300 in initial claims with a pervasive impact across a multiplicity of sectors, betting on a recession or shorting stocks on a macro basis is a fools errand.

The other important data point is the personal income and outlays data which will be important to understand for our analysis of rates and equities.

Keep reading with a 7-day free trial

Subscribe to Capital Flows to keep reading this post and get 7 days of free access to the full post archives.