The Research HUB: FX Primer, Pt 4

The primer for understanding and trading FX

Hey everyone,

This is Part 4 of the FX Primer!

5-Part FX Primer Breakdown:

Part 1: FX - Resources, The Big Picture, Variables, Aggregating Knowledge, and Essential Tools.

Part 2: FX - Synthesizing Information from Part 1: Theory, Practice, Causal Mechanics vs. Regression Analysis.

Part 3: Delving into Historical Case Studies: The Importance of Studying History, Continuity vs. Discontinuity, and the Challenges of Backtesting in FX.

Part 4: Examining the Current Environment.

Part 5: Integrating Knowledge: Top-Down and Bottom-Up Analysis, Attribution Analysis, the Expectations vs. Actual Matrix, and Quantitative Models.

Intro:

In this article, we will build on the foundation we set in the first three articles to examine the current regime in the US.

The main point I want to emphasize is that you need to be very careful using the US as the mental model for how FX works. This FX series is not meant to focus solely on the US dollar. While the US dollar is and will continue to be a significant currency, the United States occupies a unique position geographically, financially, and demographically.

What I would suggest is reviewing the Country Analysis article and connecting the concepts there with the ideas I am presenting in the FX Primer:

Country Analysis

We are expanding on the previous article and will be starting with approaching a country correctly. Here are the bullet points from the original article. Country: - Country Profile/History - Demographics - Investment/Output Capacity - Geography - Natural Resources, Weather, Transportation Networks, Technological Abilities

Alright, let’s get into the complexity!

Impossible Trinity:

Impossible Trinity in the US:

The Impossible Trinity, also known as the Trilemma, is a fundamental concept in international economics. It posits that it's impossible for a country to have all three of the following at the same time:

A fixed foreign exchange rate.

Free capital movement (absence of capital controls).

An independent monetary policy.

The US does not have a fixed foreign exchange rate, as the Fed doesn't actively intervene in currency markets to make the dollar trade at a specific level or within a specific range.

If you want an example of what a fixed exchange rate looks like, consider the Saudi currency:

Now, the thing you need to keep in mind with the fixed foreign exchange rate portion of the impossible trinity is that the degree to which a central bank can peg a currency is dependent on how much foreign reserves they have. Additionally, there is a spectrum of interventions for this. For example, the BoJ or PBoC might not actually pin their exchange rate, but they will intervene in currency markets or manipulate the currency strategically.

The US doesn't have any capital controls either, which means foreigners can freely move their money in and out of US markets. This is actually one of the reasons the US dollar has reserve status. The US has the deepest and most liquid markets for investors to seek returns and preserve their capital. When people talk about the Yuan being the next reserve currency, part of the problem is the capital controls in China.

Finally, the US does have an independent monetary policy. The Fed makes their decisions based on inflation and unemployment. Given the Fed's mandate, their primary concern is their charter as opposed to capital flight or a specific target for the dollar.

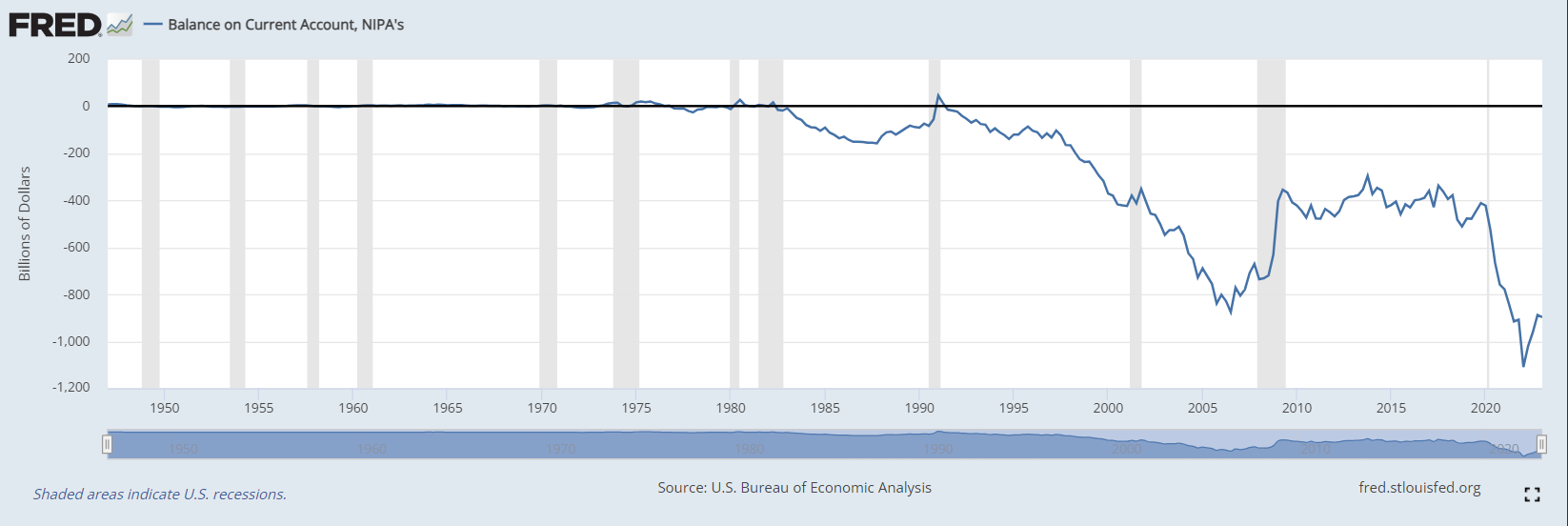

Balance of Payments:

Here is the current account for the US:

The current account is always connected with the supply and demand situation. The current account reflects the differential between demand and output. For example, if the US has more demand than it has output, then it will import more. This can actually create a scenario where the US gets used to importing goods and begins offshoring a lot due to the lower costs. This creates preconditions for supply chain issues. Trade Wars are Class Wars touches on this dynamic.

This is where you need to differentiate between the flow and capital structure. The current account reflects the flow of goods and services through the balance of payments. However, we also need to see how the balance sheets of various countries overlap with the US.

Another way to put it is that the current account might reflect the income statement (or at least be connected to it since imports/exports are line items in GDP), and the balance sheet is reflected in the assets foreigners hold in exchange for those goods (see IMF balance of payments manual in Part 3 for differences between capital account and financial account).

You can begin to break down the US balance sheet and see how much is owned by foreigners by going through the Financial Accounts of the United States: https://fred.stlouisfed.org/release?rid=52

In the same way a small company might overleverage its balance sheet and then begin to have issues meeting debt service payments due to a cyclical downturn in their revenue, a country can face the same pressure on their balance sheet. Wherever that country is on the impossible trinity spectrum will determine where the risk is expressed. It comes down to asset-liability mismatch.

As we have seen in the US, a lot of the risk has been expressed in the dollar. However, since it has reserve status, much of the devaluation has been offset by the continual bid by foreigners.

A lot of the correlations in markets and the sensitivity of cross-border flows to regime changes in GIP are due to the overlapping of countries' balance sheets and balance of payments.

This brings us to GIP regimes and GIP differentials...

GIP Regime and GIP Differentials:

When I think about GIP regimes, I model them in terms of impulses. For example, the dominant part of the inflationary impulse was in 2022. The impulse began to fade as we entered 2023, even though inflation remains elevated. A lot of my ideas around this were framed by The Origin Of Wealth.

You always want to identify the dominant impulse and then figure out how this impulse is driving risk premiums and returns across all assets. For instance, during 2022, the dominant driver of returns was accelerating inflation and Fed tightening, as opposed to slowing growth. This means that as there is a marginal change in that impulse, its impact on returns will begin to change.

If we begin to transition to a regime where negative growth becomes the dominant impulse, then we are starting to shift to what is driving returns and risk premiums across assets. However, it is possible that if we see some negative growth, the Fed could cut, which introduces an additional input into the expected returns of assets that you need to net out.

I touched on this in the S&P500 (link) primer, but there is fundamentally the earnings function and valuation function of an asset. The net change in both of these is what changes expected returns and realized returns. Liquidity in the market moves the valuation function, and growth in the economy moves the earnings function. This is why monitoring BOTH is key.

The bottom line is that after you have quantified the ideas from Parts 1-3 of this primer, you can begin to map how GIP impulses and GIP differentials are changing and thereby impacting relative returns and relative risk premiums.

Again, a lot of these ideas are laid out in Book#4: Foreign Exchange: Practical Asset Pricing and Macroeconomic Theory by Adam S. Iqbal. There are many other books that Adam cites that also expand on these ideas.

Conclusion:

Once we finally bring all these ideas together, we can start connecting the big-picture analysis and views to weekly developments and execution. This is where monitoring expectations vs. actuals in data prints and the subsequent price action can truly generate alpha.

This is also where we begin to overlay quantitative models that provide an additional edge to the risk-reward we have established thus far.

This is what Part 5 will be focused on!

In the information age, you simply need to be at the right place, at the right time, with the right information to succeed

Thanks for reading!