The Research Hub: What Is TRUE Diversification?

It's not 60/40

Hey everyone,

I want to start by thanking each one of you for taking the time to subscribe, read, and support me. We are almost at 4,000 subscribers on this Substack which is kind of crazy because it only feels like yesterday when we hit 200!

If you want a little more background on where I am heading with this Substack, read this article:

Synthesis Of ALL The Research + Special Announcement

Hello everyone, This will be an important article! I am going over two things: Special Announcement A Complete Synthesis Of All The Research

I have written educational primers on the S&P500 (link), the bond market (link), and FX (link). I am going to add a primer on intraday analysis/trading very soon so be on the lookout for it!

After I write the intraday trading primer, I will write another synthisis article pulling together all the research and providing some more background on myself as well as developments that will be taking place on this Substack.

Diversification:

Today, we will be talking about diversification. Now here is the deal, the people who read this Substack span a wide variety of fields, sectors of the markets, and trading styles. I will show WHY knowing the logic of diversification is incredibly valuable regardless of the TYPE of participation you have in financial markets. I will even touch on taking advantage of other participants’ poor diversification.

Let’s start with 3 overarching principles:

I used to think the idea of diversification was a fancy way of making excuses for poor returns. Then I realized, it 100% is an excuse in most of the financial industry because most “finance professionals” don’t understand how diversification works. They simply feed a line to people about their target date funds or “well-balanced portfolios.” TRUE diversification produces higher returns because TRUE diversification creates a whole (portfolio) that is greater than the sum of its individual parts. In my mind, diversification is something that is advantageous and produces higher returns. For example, if the portfolio is truly diversified, then either there will be outperformance on the upside or less of a drawdown on the downside. Either of these outcomes allows you to have a greater advantage to either use leverage or strategically rebalance.

Diversification is based on how the system or environment functions. When we approach the idea of diversification, it is usually coupled with the idea of correlations. The point at which this breaks down is when correlations change or all go to 1. This is why it is important to know the causal mechanics of a system and WHY correlations change. If you don’t know the WHY behind correlations, you will always be at risk when correlations change.

The final idea is that there is a fundamental difference between an event happening and your exposure to that event. For example, if I tell you that the market crashed, this isn’t necessarily good or bad because its impact is dependent on your exposure. On top of that, you could be long stocks in a portfolio and not lose money in a crash if you have offsetting positions or hedges.

Break Down System and Exposues:

There are two books I would start with to understand the concept of diversification in financial markets:

Now, part of building a diversified portfolio is knowing the moving parts you can have exposure to. On top of that, if you are just running idiosyncratic trades, knowing all the moving parts can be incredibly valuable for having visibility and knowing positioning in the market.

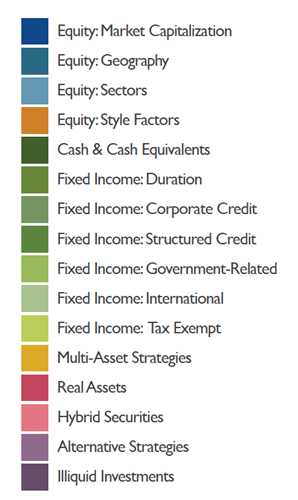

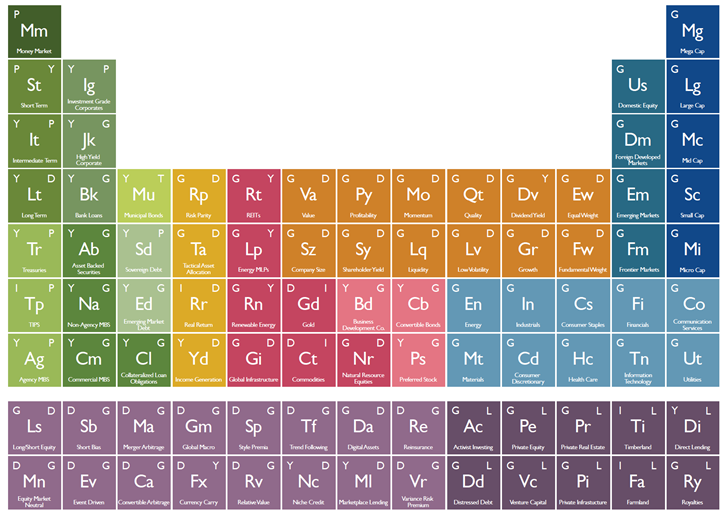

The author of the Allocators Edge breaks down the system across a number of spectrums:

And then he provides an entire period table of them. I really like thinking about this framework!

Now let’s say you don’t have the time or ability to quantify all of these differences on the table. Instead, you can try to find ETFs, mutual funds, or indices that roughly track the performance of each element.

You can begin to connect each of these elements to the macro regime you are in and how the various scenarios set up various correlations that could take place in the future.

When you begin to think about expressing ideas in multifaceted ways, then you begin to think about your exposure differently. If I can really match the right makeup of assets and weightings to the current market regime, I can actually use more leverage.

The ultimate goal is to have a whole that is greater than the sum of its parts so that I can increase my overall returns or decrease my overall risk.

Monitoring Positioning:

Now let’s say that you just trade a single asset directionally on a specific time horizon. Why in the world would you care about diversification and all of these moving parts in the system?

Well, the first reason is that the majority of the market usually holds some type of aggregated portfolio as opposed to being concentrated in a single asset. This means that constraints to buy or sell are not purely based on the levels or performance of a single asset.

For example, the famous 60/40 stock bond portfolio during 2020 and 2022 illustrated this. During 2020, bonds went up and stocks went down. This allowed portfolios to lose less overall and rebalance.

When we look at stock bond price action during this time, we can see the rebalancing flows very clearly:

Now think about what happened in 2022 when BOTH stocks and bonds fell? There is no ability to rebalance like there was during 2020. The result? Investors sell BOTH stocks and bonds to move to cash.

Remember, cash is an asset too! Don’t think of cash as some neutral type of place you can stay if you don’t want to make a decision. Cash is fundamentally an asset. The value of cash is dependent on its purchasing power relative to a basket of goods or assets.

So let’s say you are trading stocks or bonds during these periods of time. Knowing the WHY behind these correlations can be incredibly valuable for taking directional trades. That is the reason you want to understand diversification and correlations in the system. It can be incredibly lucrative for taking individual directional trades.

A lot of this will also connect with quantifying risk on/risk off regimes in markets. Here is the article I wrote on it:

The Research Hub: Risk On / Risk Off Regimes

Hey everyone, There is a lot of discussion out there as to if we are still in a bear market or have entered a new bull market. What complicates things further is everyone seems to have a different definition of a bull or bear market that they assert is “the correct definition”, as if something could even be possible.

I would also encourage you to check out the article on wealth management because it also covers a lot of these ideas from a big-picture perspective:

How To Think About Markets, Trading, and Wealth Management

This is the first publication so I am going to lay out a number of ideas in order to frame the research, thoughts, and trade ideas I am going to write. When we approach wealth management and markets, it’s important to have foundational principles and a framework to conceptualize the information and decisions we make. If you don’t have a clear understand…

Conclusion:

Aggregate portfolio decisions and diversification are something I spend a lot more time thinking about these days because I am trying to get better at constructing bets that aren’t purely directional.

I still think there is a lot of opportunity in this arena because people are so married to taking really large directional plays instead of leveraging a very specific collocation of assets.

Keep improving and adapting!

In the information age, you simply need to be at the right place, at the right time, with the right information to succeed

Thanks for reading!

Gist of the post:-

If a single data point (grwth nmbrs, infl nmbrs, etc) could up and down your whole portfolio then its not diversified...be prudent to know the difference between diversification and "die-versification"