Alpha Report: Rates, Equities, Catalysts

How to run trades in confluence with the current macro regime

In this report I am going to over 3 things:

Why the risk-reward and hit ratio of your trading (and life) matters.

How the tensions I noted in the macro report are likely to play out

Trades I am running in connection with the macro skew

Intro:

If you haven’t read the macro report, please review it here:

Comprehensive Macro Report

All of the research on interest rates and equities has been provided. I continue to hold the long ES trade published May 30th noted here: Here are the links to all the main pieces I have done recently explaining the tensions of the macro situation. Equity Report:

You can also check out my podcast on the books I’m reading here:

The Gilded Age: Jay Gould

Hello everyone, Welcome back for another podcast on the books I’m reading right now. The book I am covering today is one of my favorites and I have absolutely enjoyed reading it. It is a biography of Jay Gould whose life is an incredible educational depiction of operating at the highest levels and succeeding.

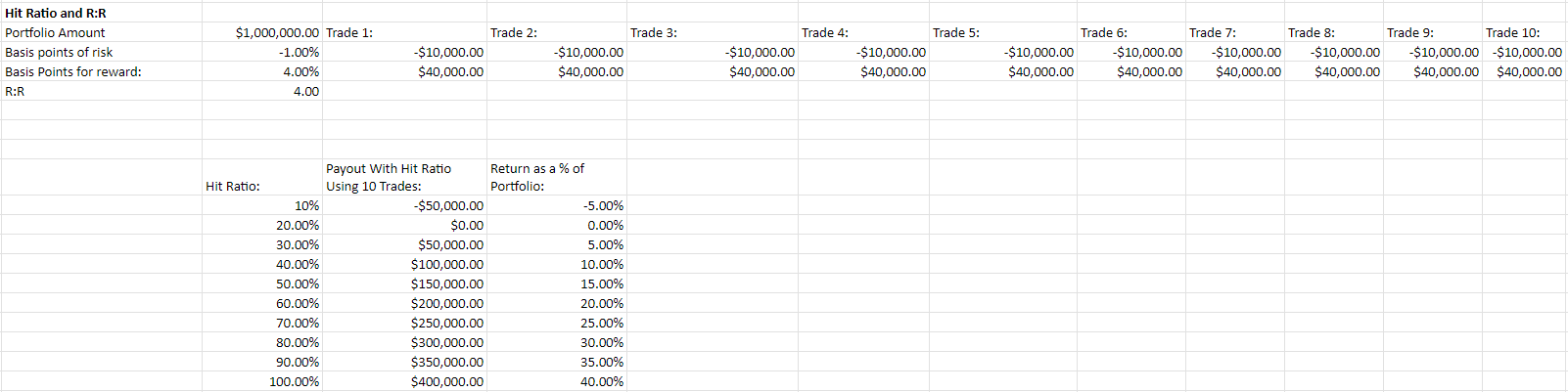

Risk Reward / Hit ratio:

Suppose I run 10 trades in a quarter. In that case, the combination of my risk reward ratio and hit ratio will produce my P&L. For example, below is a breakdown of a million-dollar portfolio amount run across 10 trades (uncompounded) with the returns based on hit ratio. If I run 10 trades that have a 4:1 risk reward and I am risking 1% of my portfolio each time then the amount of money I will make depends on my hit ratio. The hit ratio scenarios are broken down in the bottom end of the page. Notice that a 30% hit ratio is still positive in the money you make.

What does this mean? It means that you could only be right 30% of the time and still make money. This is why defining asymmetry in your risk reward (more upside than downside) is critical. You never want to take coinflip trades.

While the direction you want to go in life is driven by passion and desire, it is quantified and planned in these TYPES of metrics. All of us have a payout in life based on the opportunities (trades) we take advantage of. This isn’t just about markets, it’s called life.

I bring this up because people can forget that they need to connect the TYPE of strategy or trading they employ with the risk management of their P&L. Coherence in all processes and actions of your process is THE KEY for consistent success in any endeavor.

This brings us to HOW we should manage risk in this specific macro regime.

Extension of the macro report:

I have laid out the tensions of the macro situation in the macro report (link). The financial news media and consensus analysts continue focusing on the wrong variables and making unrealistic extrapolations.

These people still want to see a recession in all interpretations of data.

In reality, we remain in a period of time where tensions exist. We are not at an inflection point. We are definitely not in a recession and the data says the OPPOSITE of this.

The ISM is expected to accelerate this week with the price component decelerating (Goldilocks). ISM services is expected to slow marginally. The main event of this week is the minutes and NFP.

As I stated in the macro report, the economic surprise index is negative but this doesn’t imply a QoQ contraction in real GDP.

This is why the Atlanta Fed GDP nowcast remains positive.

Think about it like this: The main reason for a bond bid is going to be inflation falling and less resilient growth. If inflation keeps falling without a recession into the end of the year then you don’t want to be neutral or short bonds. There can be multiple reasons for bonds to rally, not just a recession. For some reason this is still unfathomable for people since they don’t understand how interest rates work.

Do you know how often rates go down when there isn’t a recession? A LOT!

I laid out the logic for this here:

Interest Rates, Equities, Recession?

Hello everyone, There has been some confusion among people in the news media and social media regarding how the relationship between stocks and bonds functions in both the presence and absence of a recession. For example, I keep hearing that if rates are going to come down, a recession is likely to occur. This is a conflation of two separate variables.

I laid out all of these tensions as they impact rates and equities in the reports noted below:

Macro Report: Link

Equity Report: Link

Equities are going to Melt UP published in January 2024: Link

Interest Rate Strategy and Report: Link

Interest Rate Primer: Link

This brings us to the specific trades I am running in connection with these dynamics.

Trades:

Keep reading with a 7-day free trial

Subscribe to Capital Flows to keep reading this post and get 7 days of free access to the full post archives.