Trades: Global Macro and FX

Cyclical inflection point in FX flows

Intro

FX will always be a focal point for expressing trades in global macro. In truth, nations rise and fall because of changes with their currency and interest rates both of which are inherently connected.

I have already written a 5 part FX primer on how to analyze this market correctly:

FX Primer

Since FX and rates are intricately connected, reviewing the interest rate primer will be helpful here as well:

Interest Rates Primer

The Big Picture: I remember when I first started studying why interest rates were important. It was one of the most eye-opening experiences of my life. I originally thought interest rates were irrelevant yields that the boring parts of portfolios were made of. Stocks were always where the cool kids were making money. After conducting a historical study …

One of the things I touched on in the FX primer was this idea of the impossible trinity:

This idea is critical for framing our progression forward into the end of 2024. Policymakers at the Fed and Treasury are in a constant state of trying to influence markets for their purposes. At the end of the day, this MUST be expressed somewhere.

The Big Picture:

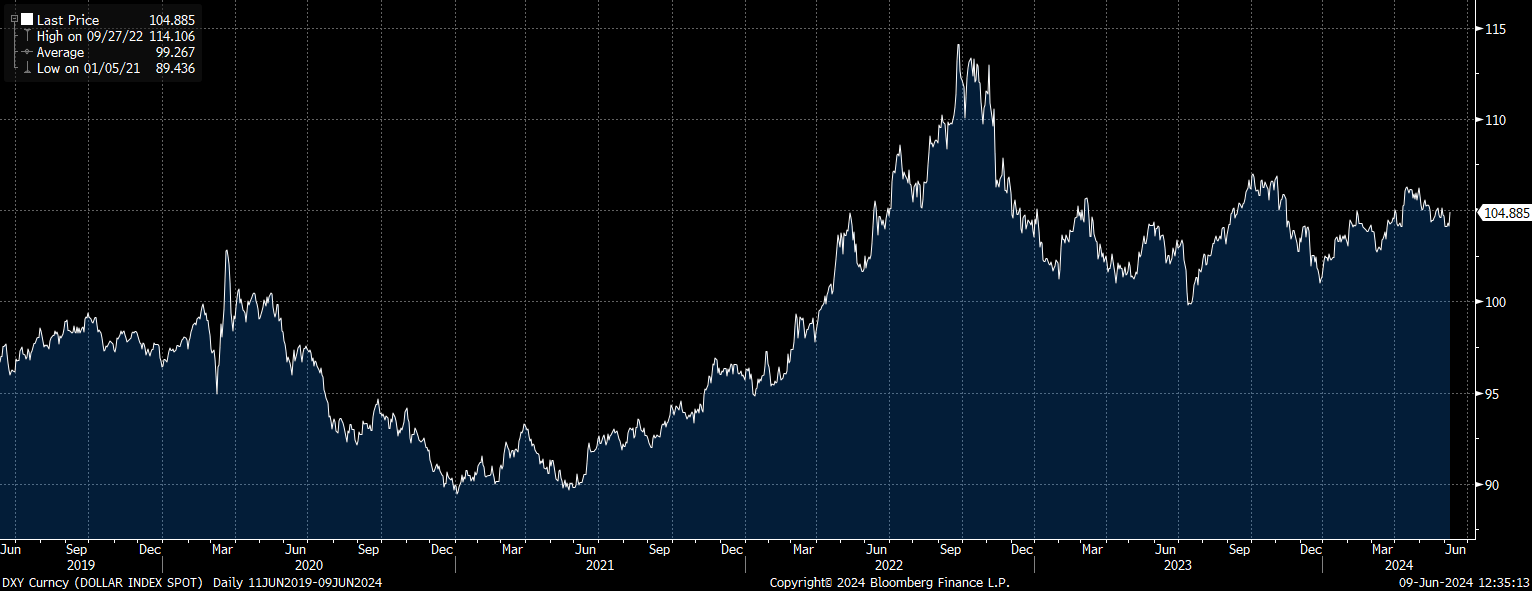

Something I have brought attention to in macro reports is how extremes have functioned since 2019. For example, during 2020 and 2021, the DXY index went to the 90 level as we had the collocation of extremely loose liquidity, negative real rates, and low expected returns across all major assets. As we entered 2022, we functionally had the exact opposite of the previous regime. The key thing to note during 2022 was that it was primarily the monetary policy function moving valuations as opposed to a deterioration in underlying growth.

Since the 2022 high, the dollar has been mean reverting in a range as policy differentials adjust to inflation and forward guidance differentials. This is critical to understand because this is a period of time where macro tensions frame the risk-reward for the DXY. During 2022 the DXY was clearly skewed to the upside based on the macro impulse and technical signals. This makes it much easier for momentum strategies to extract returns. For example, notice how the trend up during 2022 could have been traded simply using a rolling stop-loss via a moving average.

Notice that some of the highest returns for CTA strategies (represented by the green and red bars) overlapped with the bullish trend in the DXY during 2022. Why is this? This is because CTA strategies employ rolling stops very similar to the one I noted in the chart above.

This is why ETFs like DBMF 0.00%↑ and CTA 0.00%↑ moved in lockstep with the DXY.

It is this type of momentum factor that Paul Tudor Jones talks about when he says he will always have a “trend” part of his portfolio:

Similarly, it is just as important to press early profits into much more highly leveraged bets because that is the only possible way of having a home run year. I certainly do not want to gamble with my hard earned profits. I will always have a trend portfolio, no matter what.

-Paul Tudor Jones (see interview here: Link)

Where are we now?

Now let’s circle back to where we are now. We are no longer in a trend like 2020 or 2022. Rather, we are in a “mean reversion range” where the price oscillates between the compressing stdv range. This is reflected with something simple like Bollinger Bands (read this article for more on this topic: Link).

What I am going to do is explain WHY we are in this range, WHAT is likely to take as we move into 2024, and the specific trades to run based on the scenario analysis set by the macro regime. This is the framework that prepares you for adapting properly and actually benefiting from macro volatility.

Keep reading with a 7-day free trial

Subscribe to Capital Flows to keep reading this post and get 7 days of free access to the full post archives.